Running short before payday is stressful enough without paying $20 per $100 just to bridge the gap.

Possible Finance helps, but its high fees, installment loan structure, and availability in only 21 states push a lot of people to look elsewhere. The good news: apps like Possible Finance have gotten much better, and several cost significantly less.

This guide covers the 10 best alternatives for 2025, whether you need a no-fee cash advance, a payday loan alternative that builds credit, or a small-dollar loan with flexible repayment.

You will find options suited for W-2 employees, gig workers, and underbanked users alike, including apps like Dave, EarnIn, Brigit, MoneyLion, and Cleo, with a clear breakdown of fees, advance limits, and what each app actually does well.

Apps Like Possible Finance

Possible Finance offers installment loans up to $500 with no credit check, but its APRs can reach 460% in some states and it’s only available in 21 states. That’s a pretty short list. Plenty of fintech apps cover the same ground with lower fees, higher limits, or broader availability.

According to Verified Market Research, cash advance apps keep growing as more consumers look for fair, fast alternatives to traditional payday loans and bank overdrafts. Below are the 10 best alternatives worth considering.

EarnIn

EarnIn is an earned wage access app that lets salaried and hourly workers pull from pay they’ve already earned before payday. It targets employed users who need quick, fee-free access to their own money rather than a short-term loan product.

What Does EarnIn Do?

EarnIn lets users access up to $1,000 per pay period based on hours already worked, with no mandatory fees and no interest.

How Is EarnIn Similar to Possible Finance?

- No credit check required

- Same-day funding available (for a fee)

- Targets users with limited access to traditional credit

How Is EarnIn Different from Possible Finance?

Advance limit: Up to $1,000 per pay period vs. $500 from Possible.

Cost model: Tip-based with optional express fees ($3.99-$5.99), not a fixed fee per $100 borrowed.

Loan structure: Earned wage access only. It’s not an installment loan and doesn’t build credit history.

Who Is EarnIn Best For?

EarnIn suits W-2 employees with regular direct deposits who need frequent, small-to-medium advances without paying interest or monthly fees.

Key Features of EarnIn

- Max advance: $1,000/pay period ($300/day limit)

- Balance Shield: Auto-advance when balance drops below a set threshold

- Early paycheck: Up to 2 days early for $2.99/transfer

- App Store rating: 4.8/5 from 385,000+ reviews (Jan 2026)

Pricing

- Free plan: Yes, tip-based model with no mandatory fees

- Express delivery: $3.99-$5.99 optional

- Free trial: N/A

Dave

Dave is a cash advance and banking app that combines overdraft protection with a full checking account product. It’s been around since 2017 and has over 10 million downloads. The app famously landed Mark Cuban investment after appearing on Shark Tank.

What Does Dave Do?

Dave offers cash advances up to $500 via its ExtraCash feature, plus an FDIC-insured checking account and side gig connections to over 1,000 opportunities.

How Is Dave Similar to Possible Finance?

| Feature | Dave | Possible Finance |

| Max advance | $500 | $500 |

| Credit check | No | No |

| Platforms | iOS, Android | iOS, Android |

| Target user | Low-income borrowers | Low-income borrowers |

How Is Dave Different from Possible Finance?

Dave charges a flat $1/month subscription vs. Possible’s per-advance fee structure of $15-$20 per $100.

Dave requires its own checking account for full access. Possible Finance works with your existing bank.

Who Is Dave Best For?

Dave suits users who want a full neobank experience with built-in overdraft protection and don’t mind opening a new checking account to unlock higher advance limits.

Key Features of Dave

- ExtraCash: Up to $500, typically approved in 5 minutes

- FDIC-insured checking: Through Coastal Community Bank

- Side gig finder with 1,000+ opportunities

- Overdraft alerts before your balance hits zero

Pricing

- Free plan: No (requires $1/month membership)

- Paid plan: $1/month

- Express fee: $3-$25 for instant delivery

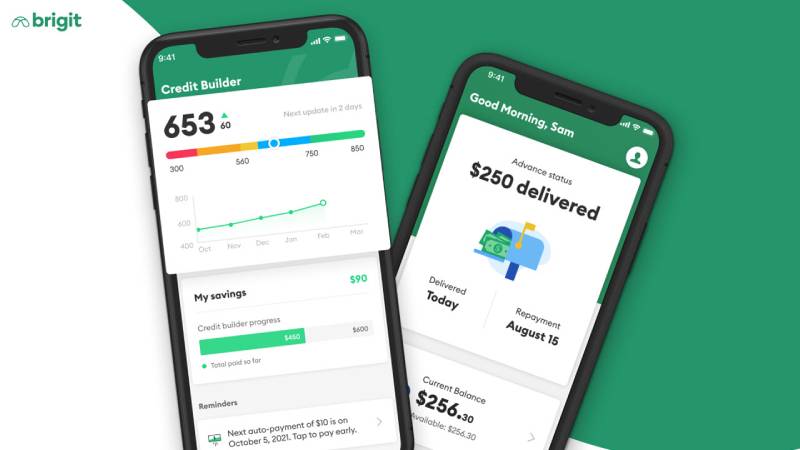

Brigit

Brigit is a credit-building cash advance app that focuses on long-term financial wellness, not just quick cash. It’s used by over 4 million members and claims to have helped save users more than $750 million in overdraft fees.

What Does Brigit Do?

Brigit offers cash advances up to $250 per pay period with no interest, no credit checks, and built-in budgeting tools and identity theft protection.

How Is Brigit Similar to Possible Finance?

- No credit check, no interest charges

- Reports to credit bureaus to help build credit history

- Targets users with unstable or low income

How Is Brigit Different from Possible Finance?

Advance cap: $250 vs. Possible’s $500 installment loan limit.

Repayment: Single repayment on next payday with extension option. Possible Finance spreads payments across 2-8 weeks.

Subscription required: $8.99-$14.99/month for Plus or Premium tiers.

Who Is Brigit Best For?

Brigit suits users who want a small emergency cash advance alongside credit-building tools, and are okay paying a monthly fee for the full feature set.

Key Features of Brigit

- Advance range: $50-$250, no interest

- Predictive overdraft alerts

- Credit builder program included in Premium

- Extension requests with no penalty

Pricing

- Free plan: Yes (limited features, no cash advance)

- Plus: $8.99/month

- Premium: $14.99/month

MoneyLion

MoneyLion is a broader personal finance platform that combines cash advances, investing, crypto, and credit-building into one app. New users can receive up to $500 through its Instacash feature, with no interest and no hard credit check.

What Does MoneyLion Do?

MoneyLion lets users access earned wage advances up to $500 (up to $1,000 with a RoarMoney account), while also offering investment accounts, loan marketplace access, and auto loan connections.

How Is MoneyLion Similar to Possible Finance?

Both apps target users who can’t access traditional credit. Both offer up to $500 with no interest on advances and no mandatory credit check.

How Is MoneyLion Different from Possible Finance?

MoneyLion disbursements are capped at $100 per transfer, so reaching $500 requires multiple transactions. Possible Finance delivers the full loan amount at once.

MoneyLion includes investing and crypto tools. Possible Finance is strictly a lending product.

Who Is MoneyLion Best For?

MoneyLion suits users who want a multi-tool financial app covering advances, investing, and credit-building, and don’t need the full amount in a single transfer.

Key Features of MoneyLion

- Instacash: Up to $500 (or $1,000 with RoarMoney)

- Managed investing and crypto auto-invest

- Credit Builder Plus: $19.99/month

- Turbo delivery: $0.49-$8.99 fee

Pricing

- Free plan: Yes (basic Instacash access)

- Credit Builder Plus: $19.99/month

- Turbo fee: $0.49-$8.99 per transfer

Chime

Chime is a neobank, not a standalone cash advance app. Its SpotMe feature gives eligible users fee-free overdraft coverage up to $200, and its MyPay feature offers early paycheck access. Over 13 million people use it as their primary bank account.

What Does Chime Do?

Chime provides mobile banking with no monthly fees, fee-free overdraft protection up to $200, and access to 60,000+ ATMs through its SpotMe and Credit Builder products.

How Is Chime Similar to Possible Finance?

- No credit check for SpotMe

- Targets underbanked and low-income users

- Available on iOS and Android

- Helps users avoid overdraft fees

How Is Chime Different from Possible Finance?

Chime requires you to use it as your primary bank with direct deposit. Possible Finance works with any bank account.

Product type: Overdraft protection, not an installment loan. Chime does not report payments to credit bureaus the same way Possible Finance does.

Who Is Chime Best For?

Chime suits users who want a full banking replacement with built-in overdraft protection and are willing to switch their direct deposit.

Key Features of Chime

- SpotMe: Fee-free overdraft up to $200

- 60,000+ fee-free ATMs

- Get paid up to 2 days early

- Instant transfer fee: $2-$5

Pricing

- Free plan: Yes, no monthly fees

- Paid plans: None (fee-free banking model)

- Instant transfer: $2-$5 optional

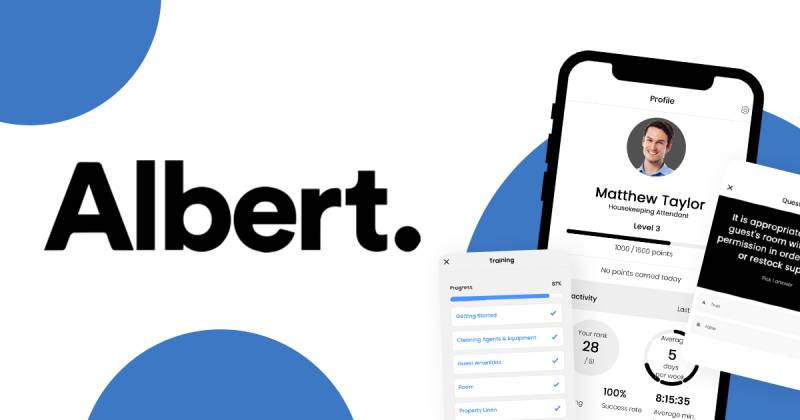

Albert

Albert is a budgeting and cash advance app with a Genius subscription that adds financial coaching and investment tools. It offers cash advances up to $250 with no interest and no credit check, available on iOS and Android.

What Does Albert Do?

Albert lets users access early paycheck deposits up to 2 days early, request cash advances, and get AI-driven savings and investment recommendations through the Genius tier.

How Is Albert Similar to Possible Finance?

Both offer small-dollar advances to users with limited credit access. Neither charges interest on the advance itself. Both are available without a hard credit check.

How Is Albert Different from Possible Finance?

| Feature | Albert | Possible Finance |

| Advance limit | $250 | $500 |

| Subscription | $14.99/month (Genius) | Per-advance fee |

| Credit building | No direct reporting | Reports to 2 bureaus |

| Extra tools | Investing, coaching | Loan product only |

Who Is Albert Best For?

Albert suits users who want cash advances alongside financial coaching and automated savings, and are comfortable with a $14.99/month subscription.

Key Features of Albert

- Advance limit: Up to $250, no interest

- Early paycheck access up to 2 days

- AI savings automation

- Financial coaching via Genius subscription

Pricing

- Free plan: Yes (limited features)

- Genius: $14.99/month

- Free trial: No

Empower

Empower (now rebranding as Tilt) is a cash advance and credit card app offering advances between $10 and $400. It charges a flat $8/month subscription and connects directly to your existing bank account via Plaid. No credit check, no interest.

What Does Empower Do?

Empower provides instant cash advances up to $400, a debit card with up to 10% cashback, and overdraft protection. Advance amounts are based on income and spending patterns.

How Is Empower Similar to Possible Finance?

- No credit check, no interest on advances

- Same-day funding available for a fee

- Works with your existing bank account

How Is Empower Different from Possible Finance?

Empower’s flat $8/month is more predictable than Possible’s per-advance fees. First-time users typically receive an average of $101, with returning users averaging $178.

Empower also includes a debit card with cashback, which Possible Finance doesn’t offer.

Who Is Empower Best For?

Empower suits users who want moderate cash advances with transparent pricing and don’t want to switch banks or deal with tip-based models.

Key Features of Empower

- Advance range: $10-$400 based on income

- 75% eligibility rate (above industry average)

- Empower Card with up to 10% cashback

- Instant delivery included in subscription

Pricing

- Free plan: No

- Subscription: $8/month flat

- Free trial: No

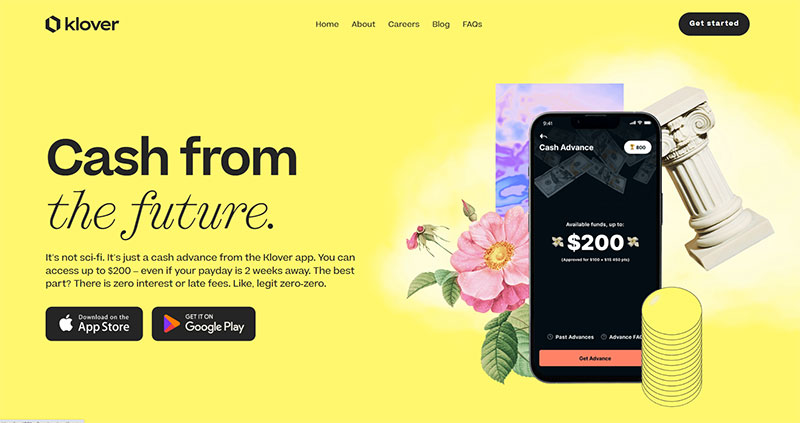

Klover

Klover is a no-fee cash advance app that gives users access to up to $200 up to two weeks before payday. Instead of charging interest or a subscription, it uses a points system where users earn higher advance limits by completing surveys, watching ads, or referring friends.

What Does Klover Do?

Klover provides small cash advances up to $200 with no credit check and no mandatory fees, funded by user data-sharing and in-app activity completion.

How Is Klover Similar to Possible Finance?

Both apps target bad credit borrowers and don’t run hard credit checks. Both are available on iOS and Android with instant or near-instant funding options.

How Is Klover Different from Possible Finance?

Klover’s $200 cap is well below Possible’s $500 limit. Also worth noting: Klover’s model depends on you sharing financial data and completing tasks to unlock better limits.

Possible Finance reports on-time payments to credit bureaus. Klover does not.

Who Is Klover Best For?

Klover suits users who need a small, fee-free advance and don’t mind engaging with in-app surveys and offers to access higher limits over time.

Key Features of Klover

- Max advance: $200 (limit grows with points activity)

- No mandatory fees or subscription

- Points system: earn higher limits via tasks

- Delivery fee: $1.49-$21.99 for instant transfers

Pricing

- Free plan: Yes, no mandatory fees

- Instant transfer: $1.49-$21.99 (optional)

- Free trial: N/A

FloatMe

FloatMe is a small-dollar cash advance app designed for one specific problem: stopping overdraft fees before payday. Advances start at $10-$50 for new users, with existing members eligible for up to $100. It’s a focused, low-frills tool.

Worth noting: FloatMe settled with the FTC in January 2024 for $3 million over misleading claims about advance limits and fees. The app has since updated its disclosures significantly.

What Does FloatMe Do?

FloatMe provides interest-free cash advances up to $100, overdraft alerts, and a Financial Forecast tool that estimates your available balance before payday.

How Is FloatMe Similar to Possible Finance?

- No credit check, 0% interest

- Targets users at risk of bank overdrafts

- Available on iOS and Android

How Is FloatMe Different from Possible Finance?

FloatMe’s $100 max is far below Possible’s $500 limit. It’s also subscription-based at $4.99/month regardless of whether you borrow.

FloatMe does not report payments to credit bureaus. No credit-building benefit.

Who Is FloatMe Best For?

FloatMe suits budget-conscious users who only need a small weekly buffer against overdraft fees and already have a steady direct deposit from an employer.

Key Features of FloatMe

- Advance range: $10-$50 (new), up to $100 (existing members)

- Financial Forecast balance estimator

- Overdraft risk alerts

- Instant transfer fee: $1-$7

Pricing

- Free plan: No

- Subscription: $4.99/month

- Free trial: 7-day trial period

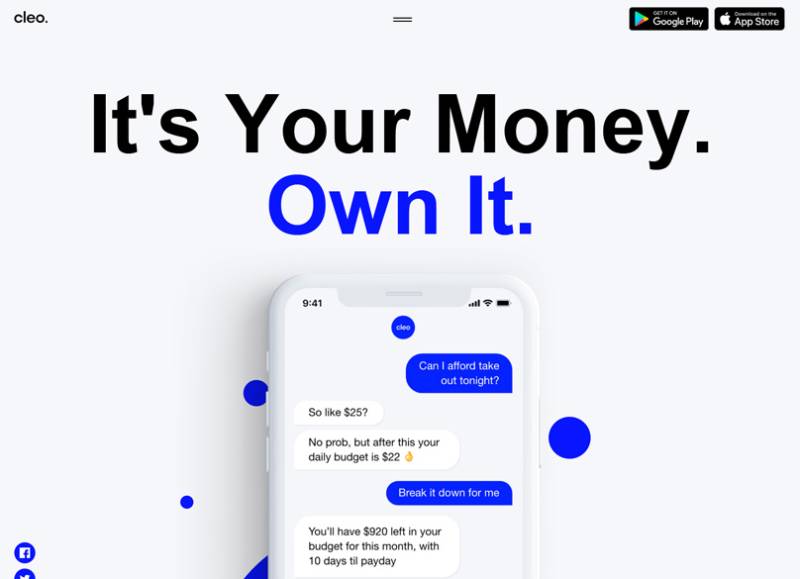

Cleo

Cleo is an AI-powered budgeting app with a cash advance feature and a famously sarcastic chatbot. It targets younger users who want money management to feel less like a chore. As of March 2025, Cleo agreed to a $17 million FTC settlement over misleading cash advance disclosures, and has since improved its transparency.

What Does Cleo Do?

Cleo lets users access cash advances between $20-$250 (first-timers capped at $100), track spending via AI, build credit with a secured card, and save in a high-yield account with 3.33% APY.

How Is Cleo Similar to Possible Finance?

Both apps serve users with limited credit access and offer cash advances with no hard credit check. Both are available on iOS and Android with same-day funding options for a fee.

How Is Cleo Different from Possible Finance?

| Feature | Cleo | Possible Finance |

| Advance limit | Up to $250 | Up to $500 |

| Subscription | $5.99/month (Plus) | Per-advance fee |

| Credit building | Secured card (Builder tier) | Reports to 2 bureaus |

| Unique feature | AI chatbot, budgeting | Installment loan structure |

Who Is Cleo Best For?

Cleo suits gig workers, freelancers, and younger users who want AI-driven budgeting alongside small cash advances and prefer a conversational app experience.

Key Features of Cleo

- Advance range: $20-$250 (no credit check)

- AI chatbot with spending “roasts” and coaching

- High-yield savings at 3.33% APY

- Cleo Card (secured credit builder) via Builder tier

- Express fee: $3.99-$14.99 for same-day transfer

Pricing

- Free plan: Yes (budgeting tools only)

- Plus: $5.99/month (includes cash advances)

- Builder: $14.99/month (adds credit card)

What Makes an App a True Alternative to Possible Finance?

Possible Finance offers installment loans between $50 and $500 with no credit check, a 2-8 week repayment window, and reports payments to TransUnion and Equifax. It’s a specific product, and not every cash advance app replaces it on every dimension.

The cash advance app market was valued at $7.69 billion in 2024 and is projected to grow at an 11.3% CAGR through 2035, according to Wise Guy Reports. That means a lot of alternatives, but not all of them solve the same problem.

Four attributes define a genuine Possible Finance alternative:

- Small-dollar access ($50-$500 range)

- No hard credit check

- Low or no interest on the advance itself

- Mobile-first delivery to an existing bank account

Possible Finance’s APR can reach 460% in some states despite the no-interest framing, because it charges $15-$20 per $100 borrowed as a flat fee. Most alternatives cost less on a per-dollar basis, though some add monthly subscription fees that change the math for infrequent borrowers.

One other factor matters: credit building. Possible Finance reports on-time payments to two credit bureaus. That’s not common in this space. If credit-building is the reason you’re using it, the shortlist of true alternatives shrinks fast.

| Attribute | Possible Finance | Most Cash Advance Apps |

| Advance limit | Up to $500 | $50–$1,000 |

| Repayment structure | Installment (2–8 weeks) | Lump sum on next payday |

| Credit reporting | Yes (TransUnion, Equifax) | Rarely |

| State availability | 21 states only | Usually broader |

| Fee model | Per-advance ($15–$20/$100) | Subscription or tip-based |

Best Cash Advance Apps Like Possible Finance for No-Fee Access

37% of Americans can’t afford an unexpected expense over $400, and 21% have no emergency savings at all, according to Empower’s 2024 research. That’s the market these apps exist to serve.

The apps below charge no mandatory fees, or charge well under what Possible Finance’s per-advance model costs. The comparison is direct: borrowing $200 from Possible Finance costs $30-$40 in fees. Each of these alternatives can deliver the same amount for less.

EarnIn

EarnIn uses a tip-based model with no mandatory fees. Users access up to $1,000 per pay period based on hours already worked, making it technically earned wage access rather than a loan.

The app requires W-2 employment, location or timesheet verification, and a regular direct deposit. Gig workers don’t qualify. EarnIn held a 4.8/5 rating from over 385,000 App Store reviews as of January 2026.

Key tradeoff: No credit reporting. Using EarnIn doesn’t build your credit history the way Possible Finance does.

- Max advance: $1,000/pay period, $300/day limit

- Express fee: $3.99-$5.99 (optional)

- Balance Shield: auto-advance when balance drops below a threshold

Dave

Dave became famous after appearing on Shark Tank with Mark Cuban backing. It’s evolved well beyond that into a full neobank product.

ExtraCash limit: Up to $500, typically approved in 5 minutes.

Key requirement: Dave requires its own FDIC-insured checking account for full access. Unlike EarnIn, this means switching (or adding) a bank account. Possible Finance works with any existing bank.

Dave costs $1/month flat, which is significantly cheaper than Possible Finance’s per-advance fee structure for regular borrowers.

Klover

Zero mandatory fees. Klover funds its model through user data-sharing and in-app task completion (surveys, ads), which is the tradeoff.

Advance limit caps at $200, well below Possible Finance’s $500. Limit grows over time as you earn points by completing in-app activities. Klover does not report to credit bureaus.

Instant delivery runs $1.49-$21.99 depending on the amount. Slow delivery is free.

Best for: Users who need a small, occasional advance and won’t miss the credit-building feature.

| App | Max Advance | Mandatory Fee | Credit Reporting |

| EarnIn | $1,000/period | None (tip-based) | No |

| Dave | $500 | $1/month | No |

| Klover | $200 | None | No |

| Possible Finance | $500 | $15–$20 per $100 | Yes |

Cash Advance Apps That Also Build Credit Like Possible Finance

About 15.7% of U.S. households lack any mainstream credit products that show up on a credit report, according to the 2023 FDIC National Survey of Unbanked and Underbanked Households. For these users, credit reporting is the entire point of using Possible Finance over a cheaper alternative.

Most cash advance apps, including Cleo, FloatMe, and Klover, do not report to any credit bureau. The short list below actually does.

Which cash advance apps report payments to credit bureaus?

Possible Finance reports to TransUnion and Equifax on on-time installment payments.

Brigit includes a credit builder program within its Plus and Premium tiers. It reports to credit bureaus through a credit builder loan structure, separate from the cash advance feature itself.

MoneyLion Credit Builder Plus combines a cash advance with a credit builder loan, reporting to all three bureaus (Equifax, Experian, TransUnion) for $19.99/month.

Self Financial is not a cash advance app, but it’s worth mentioning as an adjacent tool. It offers credit-builder loans that report to all three bureaus with no cash advance component.

How does Possible Finance’s credit reporting compare to Brigit and MoneyLion?

Possible Finance reports installment loan payments, which carry more weight in FICO scoring than a simple credit builder product. Each on-time payment actively builds repayment history across two bureaus.

Brigit’s credit builder is an add-on, not a feature of the cash advance itself. The advance you take doesn’t directly build credit. It’s the separate credit builder loan that reports.

MoneyLion’s Credit Builder Plus reports to all three bureaus, which is broader than Possible Finance’s two. The $19.99/month cost is steep for users who only need the credit-building piece.

| App | Bureaus Reported | Credit Mechanism | Monthly Cost |

| Possible Finance | TransUnion, Experian | Installment loan payments | $0 (fee per advance) |

| Brigit (Premium) | All three major bureaus | Separate credit builder loan | $14.99 |

| MoneyLion (CBP) | All three major bureaus | Combined advance + loan | $19.99 |

| Self Financial | All three major bureaus | Standalone credit builder | From $25 |

Apps Like Possible Finance for Bad Credit and Underbanked Users

The FDIC found that 14.2% of U.S. households (about 19 million) were underbanked in 2023, meaning they have a bank account but still rely on nonbank financial services. This is Possible Finance’s core user base.

Racial disparities are significant: about one in five Black and Hispanic households were underbanked, compared to one in ten white households (FDIC, 2023). The apps below all work without a hard credit check and are designed for users in this segment.

Empower (Tilt)

Empower, now rebranding as Tilt, publishes more transparency data than most competitors. Average advance for first-time users is $101; returning users average $178. Eligibility rate is 75%, which is above the industry norm.

Flat $8/month subscription. Works with your existing bank account through Plaid. No need to open a new account, which matters for users wary of adding another banking relationship.

- Advance range: $10-$400

- Empower Card: up to 10% cashback, no overdraft fees

- Instant delivery included in subscription

Cleo

Cleo uses AI to combine budgeting, cash advances, and a secured credit card. It’s one of the few apps in this space that works for gig workers, Uber drivers, and DoorDash contractors who can’t use EarnIn due to employment verification requirements.

As of March 2025, Cleo settled with the FTC for $17 million over misleading cash advance disclosures. The app has since updated its disclosures and fee structures significantly.

Advance range: $20-$250. First-time users are capped at $100. Plus subscription costs $5.99/month.

Albert and apps like Albert

Albert targets users who want AI-assisted budgeting alongside cash advances, not just emergency cash. Its Genius subscription at $14.99/month includes automated savings, investment options, and financial coaching.

Advance limit is $250 with no interest and no credit check. Albert also offers early paycheck access up to 2 days early. For users who want more than just a loan product, similar apps to Albert exist that replicate this approach with slightly different pricing or advance limits.

Klover for zero-fee access

For users who want the fewest strings attached, alternatives to Klover and Klover itself offer a rare no-mandatory-fee model. The tradeoff is data sharing and a lower advance ceiling of $200.

State availability gaps to know: FloatMe is unavailable in CT, DC, and NV. Possible Finance itself is limited to 21 states. Empower and Dave have broader footprints.

How Do Apps Like Possible Finance Handle Repayment and Loan Structure?

This is where most comparisons miss something important. Possible Finance is an installment loan, not a single-repayment cash advance. That structural difference affects who each product actually helps.

Pew Charitable Trusts research found that 80% of payday loan borrowers can’t repay in the standard two-week window and roll over into a new loan. Installment structures like Possible Finance’s exist precisely to prevent that cycle.

Do any apps offer installment repayment like Possible Finance?

Most don’t. Dave, EarnIn, Cleo, Brigit, and Klover all use single lump-sum repayment on the user’s next payday.

Brigit offers an extension option with no penalty, which softens the single-repayment model somewhat. Cleo allows up to 14 additional days with no interest or fees. FloatMe lets users set their own repayment date within reason.

SoLo Funds takes a different approach entirely. It’s a peer-to-peer lending platform where loan terms, including repayment schedules, are negotiated between borrower and lender. For users who need more flexibility than a fixed payday repayment, peer-to-peer lending apps similar to SoLo Funds represent a genuinely different model.

Failed repayment handling varies significantly:

- FloatMe and Cleo: no debt collectors, no credit bureau reporting for missed payments

- Dave: auto-retries the ACH debit after a few days

- EarnIn: retries automatically, may limit future access until repaid

- Possible Finance: may affect credit score since it reports to bureaus

The credit-reporting feature cuts both ways. On-time payments help your score. A missed payment on Possible Finance does more damage than missing a payment on most competitors.

What Are the Fees and Costs Across Apps Like Possible Finance?

Payday lenders drained more than $2.4 billion in fees from low-income borrowers in a single year through 30 states that allow payday lending, according to the Center for Responsible Lending. Cash advance apps are cheaper, but “cheaper” depends entirely on how often you borrow.

Banks still collected $5.8 billion in overdraft fees in 2023 (Motley Fool), averaging $35 per incident. That context matters: a $4.99/month FloatMe subscription becomes cost-effective if it prevents even one overdraft per month.

Which app is cheapest for borrowing $100 once a month?

Run the numbers for a single $100 advance monthly:

- EarnIn: $0 mandatory + optional $3.99-$5.99 express fee

- Klover: $0 mandatory + $1.49-$21.99 instant transfer

- Dave: $1/month + $3-$10 express fee if needed

- Cleo: $5.99/month + $3.99-$9.99 express (or slow transfer free)

- FloatMe: $4.99/month + $1-$7 instant fee

- Empower: $8/month flat (instant delivery included)

- Possible Finance: $15-$20 flat per $100 borrowed

For a single $100 advance per month, EarnIn or Klover with standard delivery cost nearly nothing. Possible Finance costs $15-$20. Over 12 months that’s $180-$240 in fees vs. near zero.

Which apps have no mandatory fees at all?

Two apps charge nothing mandatory: EarnIn (tip-based) and Klover (data-sharing funded).

EarnIn works for W-2 employees with regular direct deposits. Klover works for a broader range but caps advances at $200.

For users whose bank isn’t compatible with Plaid (which powers most of these apps), cash advance apps that bypass Plaid are a narrow but real category worth knowing. And for users already banking with Chime, cash advance apps compatible with Chime avoid the cross-platform transfer delays that add hours or days to funding time.

The real cost question isn’t the fee in isolation. It’s whether the app’s repayment structure, state availability, and credit-building feature match what you actually need. Possible Finance wins on installment structure and credit reporting. It loses on cost and geographic reach.

FAQ on Apps Like Possible Finance

What are the best apps like Possible Finance?

The top alternatives are EarnIn, Dave, Brigit, MoneyLion, Chime, Albert, Empower, Klover, FloatMe, and Cleo. Each offers small-dollar cash advances with no hard credit check. The best pick depends on your income type, borrowing frequency, and whether credit building matters to you.

Do apps like Possible Finance check your credit?

Most don’t run a hard credit check. Apps like Dave, EarnIn, Brigit, and Cleo use bank account activity and income history instead. Soft checks or no checks at all are standard across this category.

Which cash advance apps build credit like Possible Finance?

Possible Finance reports payments to TransUnion and Equifax. Brigit and MoneyLion Credit Builder Plus also report to credit bureaus. Most other cash advance apps, including EarnIn, Klover, and FloatMe, do not report to any bureau.

What is the highest cash advance available without a credit check?

EarnIn offers up to $1,000 per pay period with no mandatory fees and no credit check, the highest limit in this category. MoneyLion reaches $1,000 too, but only with a RoarMoney account and active direct deposits.

Are apps like Possible Finance safe?

Yes, established apps like Dave, Brigit, EarnIn, and MoneyLion use bank-level 256-bit encryption and connect via Plaid. They’re legitimate fintech platforms, not payday lenders. Still, always review fee disclosures carefully before linking your bank account.

What apps work like Possible Finance but with lower fees?

EarnIn and Klover charge no mandatory fees. Dave costs $1/month flat. All three are cheaper than Possible Finance’s $15-$20 per $100 borrowed. Empower’s $8/month flat rate is also more predictable for regular borrowers.

Can gig workers use apps like Possible Finance?

Some can. Cleo and Klover work for gig workers and DoorDash or Uber drivers. EarnIn and Dave require a regular employer direct deposit, which excludes most freelancers. Possible Finance itself accepts non-traditional income in qualifying states.

How fast do apps like Possible Finance send money?

Standard ACH transfers take 1-3 business days across most apps. Instant transfers are available on Dave, EarnIn, Brigit, Cleo, and Empower for an optional fee ranging from $1 to $25 depending on the amount and platform.

Do cash advance apps work with Chime?

Several do. Cleo, MoneyLion, and Dave are commonly used alongside Chime accounts. Compatibility varies, and some users report connection issues. Apps specifically designed to work with Chime avoid cross-platform transfer delays that can slow funding by hours.

What is the difference between a cash advance app and a payday loan?

Cash advance apps like Possible Finance charge flat fees or subscriptions with no interest. Payday loans average 391% APR according to the CFPB. Cash advance apps also rarely use debt collectors and typically offer more flexible repayment terms.

Conclusion

This conclusion is for an article presenting apps like Possible Finance as real, lower-cost alternatives to short-term installment loans and payday lending.

EarnIn, Brigit, MoneyLion, and Empower each solve a different piece of the puzzle. Some prioritize fee-free earned wage access. Others focus on credit building, overdraft protection, or broader financial wellness tools for underbanked users.

No single app beats Possible Finance on every dimension. But if high per-advance fees or limited state availability are the problem, there are better fits.

Match the app to your situation. A gig worker needs Cleo or Klover. A W-2 employee who rarely borrows needs EarnIn. Someone rebuilding credit needs Brigit or MoneyLion Credit Builder Plus.

The right cash advance app costs less and fits how you actually get paid.

- Android App Bundle vs APK - August 1, 2026

- PHP Cheat Sheet - July 31, 2026

- How Computer Vision, built on existing systems, increases inventory accuracy by 20%+ and protects profit margins - July 31, 2026