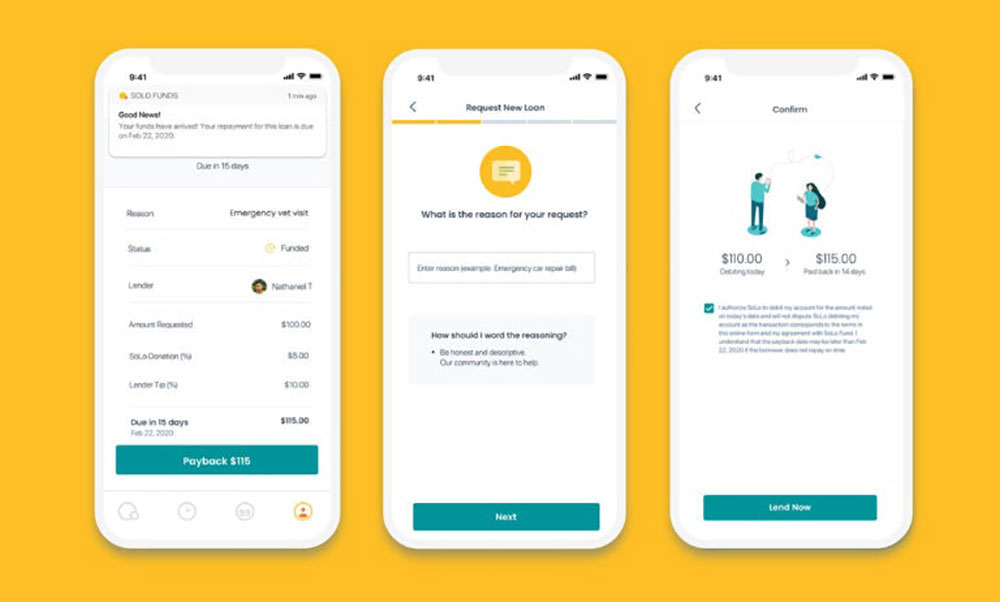

Running out of cash before payday is stressful enough without getting stuck waiting on a stranger to fund your loan request.

Solo Funds built something genuinely different with its peer-to-peer lending model, but the uncertainty of approval is a real problem when you need money now. That is why so many people go looking for apps like Solo Funds that offer faster, more predictable access to emergency cash.

This guide covers 10 alternatives, from earned wage access apps like EarnIn to direct cash advance platforms like Dave, Brigit, Possible Finance, and MoneyLion.

Each one skips the credit check, charges no interest, and gets money to your bank account faster than waiting on a peer-to-peer match.

By the end, you will know exactly which short-term loan app fits your income type, fee tolerance, and whether you want to build credit in the process.

Apps Like Solo Funds

Solo Funds runs on a peer-to-peer lending model, which is genuinely different from most cash advance apps. You post a loan request, and real people fund it. No guaranteed approval, no set timeline.

The 10 alternatives below use direct-advance models instead. Faster, more predictable, and in most cases, no credit check required.

| App | Max Advance | Monthly Fee | No Credit Check |

| EarnIn | $1,000 / pay period | None | Yes |

| Dave | $500 | Up to $5 | Yes |

| Brigit | $500 | $8.99 – $15.99 | Yes |

| MoneyLion | $1,000 | None (Turbo fees apply) | Yes |

| Albert | $1,000 | $19.99 – $39.99 | Yes |

| Cleo | $500 | $5.99 – $14.99 | Yes |

| Possible Finance | $300 (Advance) | $15 (Optional) | Yes |

| Precautionary | $500 | None (Flat fees apply) | Yes |

| Tilt (Empower) | $400 | $8 | Yes |

| Chime SpotMe | $200 | None | Yes |

According to Verified Market Research (2025), cash advance apps keep growing as more people look for fast, affordable alternatives to traditional overdraft fees and payday loans. About 33% of Americans have now used at least one of these platforms (DebtHammer).

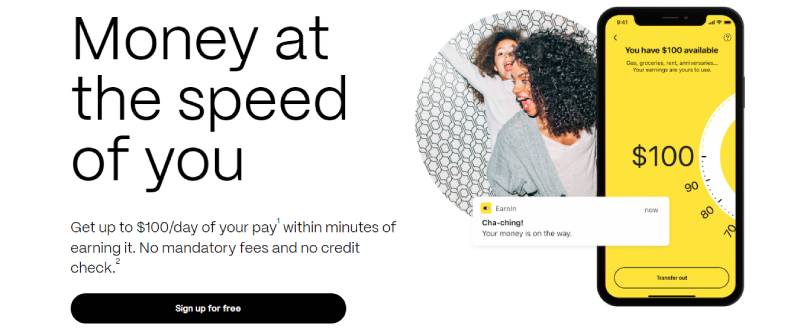

EarnIn

EarnIn is an earned wage access app that lets hourly and salaried employees pull money from their next paycheck before it arrives. It targets workers with regular direct deposits who need cash between pay periods. Unlike Solo Funds, it does not use a peer-to-peer model and does not require any credit check at all.

What Does EarnIn Do?

EarnIn lets users access up to $150 per day and $750 per pay period from wages already earned, using bank account verification and employment confirmation.

How Is EarnIn Similar to Solo Funds?

- No mandatory interest or fees on standard transfers

- No credit check required to qualify

- Available on both iOS and Android

How Is EarnIn Different from Solo Funds?

Solo Funds depends on individual lenders to fund your request. EarnIn advances your own earned wages directly. No waiting for someone to accept your loan post. Also, EarnIn requires verified employment and regular direct deposits. Solo Funds does not.

Who Is EarnIn Best For?

EarnIn suits employed workers with consistent direct deposit income who need fast, fee-free access to cash they have already earned.

Key Features of EarnIn

- Max advance: $750 per pay period ($150/day cap)

- Lightning Speed transfers: $3.99-$5.99 for instant delivery

- Balance Shield: Automatic advance if balance drops below a set threshold

- Tip-based model: Tips are optional, not required

Pricing

- Free plan: Yes, standard transfers free

- Paid plans: No subscription; optional instant transfer fees ($3.99-$5.99)

- Free trial: N/A

Dave

Dave is a mobile banking and cash advance app that offers up to $500 through its ExtraCash feature for users with active Dave accounts. It targets people who want a small emergency cash advance without going through a bank.

What Does Dave Do?

Dave offers cash advances up to $500 with no interest or credit check, alongside budgeting tools and a gig job marketplace with 1,000+ opportunities.

How Is Dave Similar to Solo Funds?

No credit check, no interest on advances. Both platforms target users who need small-dollar loans and serve people who may not qualify for traditional credit products.

How Is EarnIn Different from Solo Funds?

- Dave requires opening a Dave checking account; Solo Funds does not

- Advances are guaranteed once approved; Solo Funds loan funding is not

- Express transfer fee: $3-$25 depending on amount and destination

Who Is Dave Best For?

Dave suits users who want up to $500 instantly and do not mind opening a separate checking account to access the feature.

Key Features of Dave

- ExtraCash advances: Up to $500, no interest

- Express delivery: Minutes to Dave account, under 1 hour to external banks

- Side hustle finder: 1,000+ gig opportunities in-app

- Budgeting tools: Spending tracking and alerts included

Pricing

- Free plan: Yes (basic features)

- Paid plans: $1/month for ExtraCash access

- Free trial: No

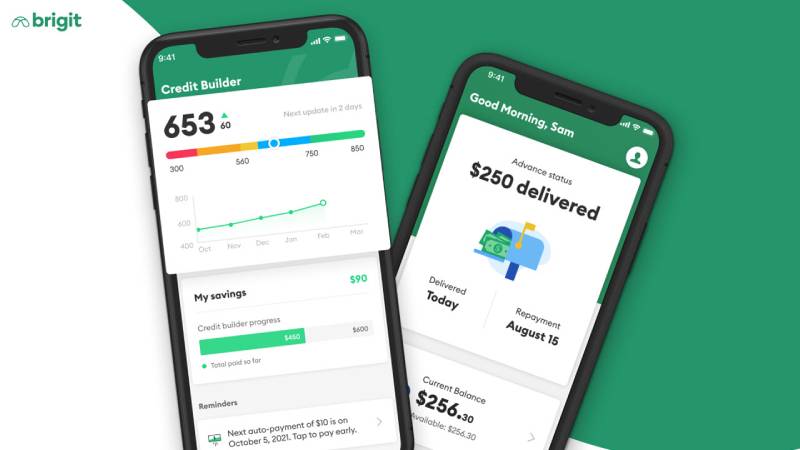

Brigit

Brigit’s standout feature is its proactive system. The app monitors your bank balance and can send you an advance before you even ask for one. It’s a good fit for people who keep getting hit with overdraft fees.

What Does Brigit Do?

Brigit offers cash advances up to $250, automatic overdraft protection, credit building, and spending insights through a monthly subscription model.

How Is Brigit Similar to Solo Funds?

- No credit check or interest on advances

- Small-dollar loan range ($50-$250) similar to Solo Funds entry-level amounts

- Supports credit building over time

How Is Brigit Different from Solo Funds?

Brigit requires a $9.99-$14.99/month subscription to access advances. Solo Funds has no membership fee. Brigit also does not report cash advance repayments to credit bureaus (only its separate credit builder product does).

Who Is Brigit Best For?

Brigit suits users who want automatic overdraft prevention and budgeting tools alongside occasional cash advances, and who will actually use all the app’s features to justify the subscription.

Key Features of Brigit

- Advance amount: $50-$250 per pay period

- Proactive alerts: Sends advance before balance hits zero

- Credit builder: Separate product, reports to bureaus

- Identity protection: Up to $1 million included

Pricing

- Free plan: Yes (budgeting and monitoring only)

- Paid plans: $9.99-$14.99/month for cash advance access

- Free trial: No

MoneyLion

MoneyLion is more than a cash advance app. It bundles Instacash advances, credit building, investing, and a checking account into one platform. It’s one of the more complete personal finance apps in this space.

What Does MoneyLion Do?

MoneyLion offers fee-free cash advances up to $500 (up to $1,000 with a RoarMoney account), plus access to credit builder loans, investment accounts, and cryptocurrency trading.

How Is MoneyLion Similar to Solo Funds?

Both platforms operate with no mandatory fees and no credit check for cash advances. Both also support credit building over time, and both are available on iOS and Android.

How Is MoneyLion Different from Solo Funds?

- Individual disbursements capped at $100 per transfer (requires multiple transfers for larger amounts)

- Instant delivery costs $0.49-$8.99 per transaction

- Requires a RoarMoney checking account to access $1,000 max

Who Is MoneyLion Best For?

MoneyLion suits users who want a full financial platform covering advances, credit building, and investing in one app.

Key Features of MoneyLion

- Instacash: Up to $500 free, up to $1,000 with RoarMoney

- Credit Builder Plus: Helps build credit history

- Investment accounts: Auto-invest and crypto options

- Turbo delivery: $0.49-$8.99 for instant transfers

Pricing

- Free plan: Yes (Instacash up to $500)

- Paid plans: Optional RoarMoney account; Credit Builder Plus at $19.99/month

- Free trial: No

Albert

Albert bundles cash advances, banking, and automated savings into a single app. It’s one of the higher-limit options here, with advances up to $1,000 for qualifying users.

What Does Albert Do?

Albert offers cash advances via its Instant feature ($25-$1,000), early paycheck access up to 2 days early, plus automated savings and investment tools through a Genius subscription.

How Is Albert Similar to Solo Funds?

| Feature | Albert | Solo Funds |

| Credit check | No | No |

| Interest on advance | No | No (tips optional) |

| iOS + Android | Yes | Yes |

| Small-dollar access | Yes | Yes |

How Is Albert Different from Solo Funds?

Albert requires a $14.99/month Genius subscription to access advances. Solo Funds has zero membership fees. Albert also charges $5.99-$19.99 to transfer to external bank accounts.

Who Is Albert Best For?

Albert suits users who want high advance limits alongside savings automation and investment tools and will use the full Genius membership features.

Key Features of Albert

- Advance range: $25-$1,000

- Early paycheck: Up to 2 days early via direct deposit

- Genius subscription: Financial coaching, investing, budgeting

- External transfer fee: $5.99-$19.99 per advance

Pricing

- Free plan: Yes (basic banking and savings)

- Paid plans: $14.99/month for cash advance access

- Free trial: No

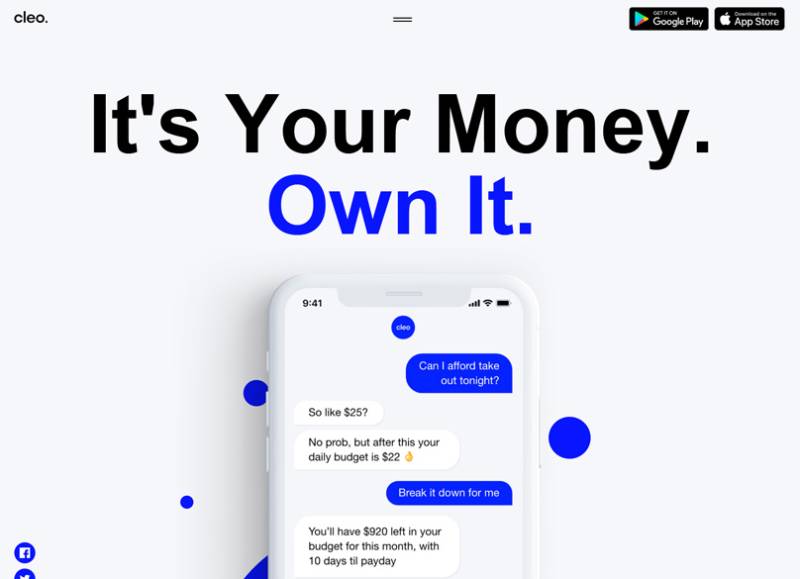

Cleo

Cleo takes a different approach than most fintech apps. Its AI assistant uses humor to coach you on spending habits, complete with a “roast mode” that calls out bad financial decisions. It is genuinely fun to use, which is not something you can say about most cash advance apps.

What Does Cleo Do?

Cleo offers AI-powered budgeting, cash advances up to $250, a credit builder card, and a high-yield savings account (3.33% APY as of 2025).

How Is Cleo Similar to Solo Funds?

No credit check, no interest on advances, and available to gig workers and freelancers. Both platforms work for users without a traditional employer-linked income.

How Is Cleo Different from Solo Funds?

- First-time users limited to $20-$100; only increases to $250 with repayment history

- Requires Cleo Plus ($5.99/month) to access cash advances

- Express transfer fee: $3.99-$14.99 for same-day delivery

Who Is Cleo Best For?

Cleo suits younger users and gig workers who want a cash advance alongside budgeting tools and do not mind a conversational AI approach to money management.

Key Features of Cleo

- Advance range: $20-$250 (max $100 per 24 hours)

- AI roast mode: Humor-based spending feedback

- Credit builder card: Secured Visa, no credit check

- Savings APY: 3.33% on Cleo savings wallet

Pricing

- Free plan: Yes (spending tracking and budgeting)

- Paid plans: Cleo Plus at $5.99/month; Cleo Builder at $14.99/month

- Free trial: No

Possible Finance

Most cash advance apps skip credit bureaus entirely. Possible Finance is different – it actually reports payments to help you build a credit history. That makes it more useful long-term for people rebuilding their credit from scratch.

What Does Possible Finance Do?

Possible offers small-dollar installment loans up to $500 and a subscription-based cash advance up to $300, both with no interest, no late fees, and no credit check. On-time payments report to credit bureaus.

How Is Possible Finance Similar to Solo Funds?

Both platforms offer no credit check, no interest borrowing for small amounts. Both also target users who struggle to access traditional credit and use mobile-first interfaces on iOS and Android.

How Is Possible Finance Different from Solo Funds?

- Possible reports payments to credit bureaus; Solo Funds also reports, but Possible’s installment loan structure has a stronger credit-building track record

- Possible Loan repaid over 4 installments (not lump sum)

- Possible Advance requires $15/month membership for full benefits

Who Is Possible Finance Best For?

Possible Finance suits users with no or bad credit who want emergency cash and a structured way to build credit history through installment repayments.

Key Features of Possible Finance

- Possible Loan: Up to $500, repaid in 4 installments

- Possible Advance: Up to $300 instantly, $15/month membership

- Credit reporting: On-time payments reported to bureaus

- Reschedule payments: Up to 29 days, no fee, no credit impact

Pricing

- Free plan: Yes (basic loan access, up to $150 non-member)

- Paid plans: $15/month for Possible Membership (unlocks up to $300 advance + free instant transfers)

- Free trial: No

Varo

Varo is an FDIC-insured online bank, not just a cash advance app. That distinction matters. You get a real bank account, a debit card, and a high-yield savings account alongside the advance feature.

What Does Varo Do?

Varo offers cash advances of $20-$500 with no interest, same-day delivery at no extra cost, and a full mobile banking suite including high-yield savings at 5.00% APY for qualifying accounts.

How Is Varo Similar to Solo Funds?

Both offer no credit check, no interest cash access. Both serve users who need small-dollar funds quickly without traditional bank approval processes.

How Is Varo Different from Solo Funds?

- Varo charges flat fees per advance: up to $40 for a $500 advance

- Requires $800+ in direct deposits in current or prior month

- Requires an active Varo Bank account (cannot use with just an external bank)

Who Is Varo Best For?

Varo suits users who already use or plan to open a Varo bank account and want same-day advance access without instant transfer fees.

Key Features of Varo

- Advance range: $20-$500 (new users capped at $250)

- Same-day delivery: Free to Varo account, no extra charge

- High-yield savings: Up to 5.00% APY

- Cash back: Up to 6% at select retailers with Varo debit card

Pricing

- Free plan: Yes (banking is free; advances have flat fees)

- Paid plans: Per-advance fee, 8% of advance amount (e.g., $40 max for $500)

- Free trial: No

Tilt (formerly Empower)

Tilt rebranded from Empower in August 2025. Same app, cleaner name. It has one of the highest eligibility rates in the industry at 75%, meaning most applicants actually qualify on the first try.

What Does Tilt Do?

Tilt offers interest-free cash advances of $10-$400, works with your existing bank account through Plaid, and includes budgeting tools, overdraft reimbursement, and cashback on purchases.

How Is Tilt Similar to Solo Funds?

No interest on advances, no credit check, and works alongside your existing bank account. Both platforms support gig workers and freelancers who may not have traditional payroll income.

How Is Tilt Different from Solo Funds?

| Feature | Tilt | Solo Funds |

| Advance model | Direct advance | Peer-to-peer lending |

| Approval speed | Instant (if eligible) | Depends on lender activity |

| Monthly fee | $8/month | None |

| Overdraft reimbursement | Yes | No |

Who Is Tilt Best For?

Tilt suits users who want predictable flat-rate pricing and high approval odds without switching banks or opening a new account.

Key Features of Tilt

- Advance range: $10-$400

- Eligibility rate: 75% (one of the highest available)

- Instant delivery: Under 15 minutes, $1-$8 fee to external accounts

- Overdraft reimbursement: Refunds overdraft fees caused by auto-repayment

Pricing

- Free plan: No

- Paid plans: $8/month flat subscription

- Free trial: No

Chime SpotMe

Chime SpotMe is the simplest option on this list. It is not really a cash advance app. It is overdraft protection built into a free mobile banking account. But for small amounts, it covers the same need.

What Does Chime SpotMe Do?

Chime lets eligible members overdraft their debit card by up to $200 at no charge. No fees, no interest, no subscription required. Repayment happens automatically from your next direct deposit.

How Is Chime Similar to Solo Funds?

No credit check, no interest, no mandatory fees. Both platforms target users who need small-dollar, short-term financial relief without traditional loan applications.

How Is Chime Different from Solo Funds?

- SpotMe limit starts at just $20 and increases up to $200 based on account activity

- Requires a Chime checking account with direct deposit of $200+ per 34 days

- Not available in 17 states (check eligibility before signing up)

Who Is Chime SpotMe Best For?

Chime suits users who already use or want free mobile banking and need occasional small overdraft coverage without a subscription or per-use fee. If you need more than $200, look elsewhere.

Key Features of Chime SpotMe

- Overdraft limit: Up to $200

- No fees: No monthly fee, no overdraft fee, no instant transfer fee

- Early paycheck: Up to 2 days early via direct deposit

- Compatibility: Works with many cash advance apps that work with Chime

Pricing

- Free plan: Yes, fully free

- Paid plans: None

- Free trial: N/A

Apps Like Solo Funds

Solo Funds runs on a peer-to-peer lending model, which is genuinely different from most cash advance apps. You post a loan request, and real people fund it. No guaranteed approval, no set timeline.

The 10 alternatives below use direct-advance models instead. Faster, more predictable, and in most cases, no credit check required.

| App | Max Advance | Monthly Fee | No Credit Check |

| EarnIn | $750/pay period | None | Yes |

| Dave | $500 | $1 | Yes |

| Brigit | $250 | $9.99-$14.99 | Yes |

| MoneyLion | $500-$1,000 | None (fees vary) | Yes |

| Albert | $1,000 | $14.99 | Yes |

| Cleo | $250 | $5.99-$14.99 | Yes |

| Possible Finance | $500 (loan) / $300 (advance) | $15 (optional) | Yes |

| Varo | $500 | None | Yes |

| Tilt (Empower) | $400 | $8 | Yes |

| Chime SpotMe | $200 | None | Yes |

According to Verified Market Research (2025), cash advance apps keep growing as more people look for fast, affordable alternatives to traditional overdraft fees and payday loans. About 33% of Americans have now used at least one of these platforms (DebtHammer).

EarnIn

EarnIn is an earned wage access app that lets hourly and salaried employees pull money from their next paycheck before it arrives. It targets workers with regular direct deposits who need cash between pay periods. Unlike Solo Funds, it does not use a peer-to-peer model and does not require any credit check at all.

What Does EarnIn Do?

EarnIn lets users access up to $150 per day and $750 per pay period from wages already earned, using bank account verification and employment confirmation.

How Is EarnIn Similar to Solo Funds?

- No mandatory interest or fees on standard transfers

- No credit check required to qualify

- Available on both iOS and Android

How Is EarnIn Different from Solo Funds?

Solo Funds depends on individual lenders to fund your request. EarnIn advances your own earned wages directly. No waiting for someone to accept your loan post. Also, EarnIn requires verified employment and regular direct deposits. Solo Funds does not.

Who Is EarnIn Best For?

EarnIn suits employed workers with consistent direct deposit income who need fast, fee-free access to cash they have already earned.

Key Features of EarnIn

- Max advance: $750 per pay period ($150/day cap)

- Lightning Speed transfers: $3.99-$5.99 for instant delivery

- Balance Shield: Automatic advance if balance drops below a set threshold

- Tip-based model: Tips are optional, not required

Pricing

- Free plan: Yes, standard transfers free

- Paid plans: No subscription; optional instant transfer fees ($3.99-$5.99)

- Free trial: N/A

Dave

Dave is a mobile banking and cash advance app that offers up to $500 through its ExtraCash feature for users with active Dave accounts. It targets people who want a small emergency cash advance without going through a bank.

What Does Dave Do?

Dave offers cash advances up to $500 with no interest or credit check, alongside budgeting tools and a gig job marketplace with 1,000+ opportunities.

How Is Dave Similar to Solo Funds?

No credit check, no interest on advances. Both platforms target users who need small-dollar loans and serve people who may not qualify for traditional credit products.

How Is EarnIn Different from Solo Funds?

- Dave requires opening a Dave checking account; Solo Funds does not

- Advances are guaranteed once approved; Solo Funds loan funding is not

- Express transfer fee: $3-$25 depending on amount and destination

Who Is Dave Best For?

Dave suits users who want up to $500 instantly and do not mind opening a separate checking account to access the feature.

Key Features of Dave

- ExtraCash advances: Up to $500, no interest

- Express delivery: Minutes to Dave account, under 1 hour to external banks

- Side hustle finder: 1,000+ gig opportunities in-app

- Budgeting tools: Spending tracking and alerts included

Pricing

- Free plan: Yes (basic features)

- Paid plans: $1/month for ExtraCash access

- Free trial: No

Brigit

Brigit’s standout feature is its proactive system. The app monitors your bank balance and can send you an advance before you even ask for one. It’s a good fit for people who keep getting hit with overdraft fees.

What Does Brigit Do?

Brigit offers cash advances up to $250, automatic overdraft protection, credit building, and spending insights through a monthly subscription model.

How Is Brigit Similar to Solo Funds?

- No credit check or interest on advances

- Small-dollar loan range ($50-$250) similar to Solo Funds entry-level amounts

- Supports credit building over time

How Is Brigit Different from Solo Funds?

Brigit requires a $9.99-$14.99/month subscription to access advances. Solo Funds has no membership fee. Brigit also does not report cash advance repayments to credit bureaus (only its separate credit builder product does).

Who Is Brigit Best For?

Brigit suits users who want automatic overdraft prevention and budgeting tools alongside occasional cash advances, and who will actually use all the app’s features to justify the subscription.

Key Features of Brigit

- Advance amount: $50-$250 per pay period

- Proactive alerts: Sends advance before balance hits zero

- Credit builder: Separate product, reports to bureaus

- Identity protection: Up to $1 million included

Pricing

- Free plan: Yes (budgeting and monitoring only)

- Paid plans: $9.99-$14.99/month for cash advance access

- Free trial: No

MoneyLion

MoneyLion is more than a cash advance app. It bundles Instacash advances, credit building, investing, and a checking account into one platform. It’s one of the more complete personal finance apps in this space.

What Does MoneyLion Do?

MoneyLion offers fee-free cash advances up to $500 (up to $1,000 with a RoarMoney account), plus access to credit builder loans, investment accounts, and cryptocurrency trading.

How Is MoneyLion Similar to Solo Funds?

Both platforms operate with no mandatory fees and no credit check for cash advances. Both also support credit building over time, and both are available on iOS and Android.

How Is MoneyLion Different from Solo Funds?

- Individual disbursements capped at $100 per transfer (requires multiple transfers for larger amounts)

- Instant delivery costs $0.49-$8.99 per transaction

- Requires a RoarMoney checking account to access $1,000 max

Who Is MoneyLion Best For?

MoneyLion suits users who want a full financial platform covering advances, credit building, and investing in one app.

Key Features of MoneyLion

- Instacash: Up to $500 free, up to $1,000 with RoarMoney

- Credit Builder Plus: Helps build credit history

- Investment accounts: Auto-invest and crypto options

- Turbo delivery: $0.49-$8.99 for instant transfers

Pricing

- Free plan: Yes (Instacash up to $500)

- Paid plans: Optional RoarMoney account; Credit Builder Plus at $19.99/month

- Free trial: No

Albert

Albert bundles cash advances, banking, and automated savings into a single app. It’s one of the higher-limit options here, with advances up to $1,000 for qualifying users.

What Does Albert Do?

Albert offers cash advances via its Instant feature ($25-$1,000), early paycheck access up to 2 days early, plus automated savings and investment tools through a Genius subscription.

How Is Albert Similar to Solo Funds?

| Feature | Albert | Solo Funds |

| Credit check | No | No |

| Interest on advance | No | No (tips optional) |

| iOS + Android | Yes | Yes |

| Small-dollar access | Yes | Yes |

How Is Albert Different from Solo Funds?

Albert requires a $14.99/month Genius subscription to access advances. Solo Funds has zero membership fees. Albert also charges $5.99-$19.99 to transfer to external bank accounts.

Who Is Albert Best For?

Albert suits users who want high advance limits alongside savings automation and investment tools and will use the full Genius membership features.

Key Features of Albert

- Advance range: $25-$1,000

- Early paycheck: Up to 2 days early via direct deposit

- Genius subscription: Financial coaching, investing, budgeting

- External transfer fee: $5.99-$19.99 per advance

Pricing

- Free plan: Yes (basic banking and savings)

- Paid plans: $14.99/month for cash advance access

- Free trial: No

Cleo

Cleo takes a different approach than most fintech apps. Its AI assistant uses humor to coach you on spending habits, complete with a “roast mode” that calls out bad financial decisions. It is genuinely fun to use, which is not something you can say about most cash advance apps.

What Does Cleo Do?

Cleo offers AI-powered budgeting, cash advances up to $250, a credit builder card, and a high-yield savings account (3.33% APY as of 2025).

How Is Cleo Similar to Solo Funds?

No credit check, no interest on advances, and available to gig workers and freelancers. Both platforms work for users without a traditional employer-linked income.

How Is Cleo Different from Solo Funds?

- First-time users limited to $20-$100; only increases to $250 with repayment history

- Requires Cleo Plus ($5.99/month) to access cash advances

- Express transfer fee: $3.99-$14.99 for same-day delivery

Who Is Cleo Best For?

Cleo suits younger users and gig workers who want a cash advance alongside budgeting tools and do not mind a conversational AI approach to money management.

Key Features of Cleo

- Advance range: $20-$250 (max $100 per 24 hours)

- AI roast mode: Humor-based spending feedback

- Credit builder card: Secured Visa, no credit check

- Savings APY: 3.33% on Cleo savings wallet

Pricing

- Free plan: Yes (spending tracking and budgeting)

- Paid plans: Cleo Plus at $5.99/month; Cleo Builder at $14.99/month

- Free trial: No

Possible Finance

Most cash advance apps skip credit bureaus entirely. Possible Finance is different – it actually reports payments to help you build a credit history. That makes it more useful long-term for people rebuilding their credit from scratch.

What Does Possible Finance Do?

Possible offers small-dollar installment loans up to $500 and a subscription-based cash advance up to $300, both with no interest, no late fees, and no credit check. On-time payments report to credit bureaus.

How Is Possible Finance Similar to Solo Funds?

Both platforms offer no credit check, no interest borrowing for small amounts. Both also target users who struggle to access traditional credit and use mobile-first interfaces on iOS and Android.

How Is Possible Finance Different from Solo Funds?

- Possible reports payments to credit bureaus; Solo Funds also reports, but Possible’s installment loan structure has a stronger credit-building track record

- Possible Loan repaid over 4 installments (not lump sum)

- Possible Advance requires $15/month membership for full benefits

Who Is Possible Finance Best For?

Possible Finance suits users with no or bad credit who want emergency cash and a structured way to build credit history through installment repayments.

Key Features of Possible Finance

- Possible Loan: Up to $500, repaid in 4 installments

- Possible Advance: Up to $300 instantly, $15/month membership

- Credit reporting: On-time payments reported to bureaus

- Reschedule payments: Up to 29 days, no fee, no credit impact

Pricing

- Free plan: Yes (basic loan access, up to $150 non-member)

- Paid plans: $15/month for Possible Membership (unlocks up to $300 advance + free instant transfers)

- Free trial: No

Varo

Varo is an FDIC-insured online bank, not just a cash advance app. That distinction matters. You get a real bank account, a debit card, and a high-yield savings account alongside the advance feature.

What Does Varo Do?

Varo offers cash advances of $20-$500 with no interest, same-day delivery at no extra cost, and a full mobile banking suite including high-yield savings at 5.00% APY for qualifying accounts.

How Is Varo Similar to Solo Funds?

Both offer no credit check, no interest cash access. Both serve users who need small-dollar funds quickly without traditional bank approval processes.

How Is Varo Different from Solo Funds?

- Varo charges flat fees per advance: up to $40 for a $500 advance

- Requires $800+ in direct deposits in current or prior month

- Requires an active Varo Bank account (cannot use with just an external bank)

Who Is Varo Best For?

Varo suits users who already use or plan to open a Varo bank account and want same-day advance access without instant transfer fees.

Key Features of Varo

- Advance range: $20-$500 (new users capped at $250)

- Same-day delivery: Free to Varo account, no extra charge

- High-yield savings: Up to 5.00% APY

- Cash back: Up to 6% at select retailers with Varo debit card

Pricing

- Free plan: Yes (banking is free; advances have flat fees)

- Paid plans: Per-advance fee, 8% of advance amount (e.g., $40 max for $500)

- Free trial: No

Tilt (formerly Empower)

Tilt rebranded from Empower in August 2025. Same app, cleaner name. It has one of the highest eligibility rates in the industry at 75%, meaning most applicants actually qualify on the first try.

What Does Tilt Do?

Tilt offers interest-free cash advances of $10-$400, works with your existing bank account through Plaid, and includes budgeting tools, overdraft reimbursement, and cashback on purchases.

How Is Tilt Similar to Solo Funds?

No interest on advances, no credit check, and works alongside your existing bank account. Both platforms support gig workers and freelancers who may not have traditional payroll income.

How Is Tilt Different from Solo Funds?

| Feature | Tilt | SoLo Funds |

| Advance model | Direct advance | Peer-to-peer lending |

| Approval speed | Instant (if eligible) | Depends on lender activity |

| Monthly fee | $8/month | None |

| Overdraft reimbursement | Yes | No |

Who Is Tilt Best For?

Tilt suits users who want predictable flat-rate pricing and high approval odds without switching banks or opening a new account.

Key Features of Tilt

- Advance range: $10-$400

- Eligibility rate: 75% (one of the highest available)

- Instant delivery: Under 15 minutes, $1-$8 fee to external accounts

- Overdraft reimbursement: Refunds overdraft fees caused by auto-repayment

Pricing

- Free plan: No

- Paid plans: $8/month flat subscription

- Free trial: No

Chime SpotMe

Chime SpotMe is the simplest option on this list. It is not really a cash advance app. It is overdraft protection built into a free mobile banking account. But for small amounts, it covers the same need.

What Does Chime SpotMe Do?

Chime lets eligible members overdraft their debit card by up to $200 at no charge. No fees, no interest, no subscription required. Repayment happens automatically from your next direct deposit.

How Is Chime Similar to Solo Funds?

No credit check, no interest, no mandatory fees. Both platforms target users who need small-dollar, short-term financial relief without traditional loan applications.

How Is Chime Different from Solo Funds?

- SpotMe limit starts at just $20 and increases up to $200 based on account activity

- Requires a Chime checking account with direct deposit of $200+ per 34 days

- Not available in 17 states (check eligibility before signing up)

Who Is Chime SpotMe Best For?

Chime suits users who already use or want free mobile banking and need occasional small overdraft coverage without a subscription or per-use fee. If you need more than $200, look elsewhere.

Key Features of Chime SpotMe

- Overdraft limit: Up to $200

- No fees: No monthly fee, no overdraft fee, no instant transfer fee

- Early paycheck: Up to 2 days early via direct deposit

- Compatibility: Works with many cash advance apps that work with Chime

Pricing

- Free plan: Yes, fully free

- Paid plans: None

- Free trial: N/A

FAQ on Apps Like Solo Funds

What is the best app like Solo Funds for instant cash?

EarnIn and Dave are the fastest options. EarnIn delivers up to $750 per pay period with no mandatory fees. Dave offers up to $500 with express delivery in minutes. Both skip credit checks entirely.

Do apps like Solo Funds require a credit check?

No. Every major alternative, including Brigit, MoneyLion, Cleo, and Possible Finance, approves users based on bank account activity and income patterns. No hard pull, no FICO score required.

What is the difference between Solo Funds and a cash advance app?

Solo Funds is a peer-to-peer lending platform. Real people fund your loan request, so approval is never guaranteed. Cash advance apps like Dave and EarnIn approve you instantly through automated systems.

Which apps like Solo Funds work for gig workers?

Cleo and Tilt are the top picks. Cleo accepts non-W2 income including DoorDash and Uber earnings. No pay stubs or direct deposit required. Possible Finance also uses bank transaction analysis instead of payroll verification.

Are there apps like Solo Funds with no monthly fee?

Yes. EarnIn, Varo, and Chime SpotMe charge no monthly subscription. Dave costs just $1/month. MoneyLion’s basic Instacash feature is also free, though instant transfers carry a per-use fee.

Which app like Solo Funds helps build credit?

Possible Finance is the strongest option. Its installment loans report on-time payments to all three credit bureaus. MoneyLion’s Credit Builder Plus also reports, but requires a separate $19.99/month subscription.

Can I use apps like Solo Funds without a direct deposit?

Yes. Cleo, Brigit, Dave, and Tilt all work without employer-linked direct deposit. They evaluate your bank account history and spending patterns instead. EarnIn and Chime SpotMe do require regular direct deposits.

How much can you borrow from apps like Solo Funds?

Most apps offer $20 to $500. Albert goes up to $1,000 for qualifying users. First-time limits are usually much lower. Cleo starts at $20-$100, and Possible Finance averages $85 on the first advance.

Are apps like Solo Funds safe to use?

The major platforms, including EarnIn, MoneyLion, and Brigit, are legitimate fintech apps used by millions. Read fee disclosures carefully. The Center for Responsible Lending found overdrafts increase 56% on average after users start borrowing from these platforms.

What happens if you don’t repay a cash advance app?

Most apps auto-debit your account on the repayment date. Missing it can trigger bank overdraft fees. Possible Finance lets you reschedule payments up to 29 days at no cost. Late repayment rarely affects your credit score directly.

Conclusion

This conclusion is for an article presenting apps like Solo Funds as real alternatives to the peer-to-peer lending model, covering everything from no credit check cash advances to installment loans that actually build your credit history.

If you need guaranteed approval and same-day funding, direct advance platforms like Brigit, MoneyLion, and Tilt beat waiting on a lender match every time.

Gig workers and freelancers without traditional payroll should look at Cleo or Possible Finance first. Both evaluate bank transaction history instead of employer-linked direct deposit.

For long-term financial wellness, Possible Finance remains the strongest pick, combining small-dollar borrowing with credit bureau reporting.

Whatever your situation, the right short-term loan app exists. Compare fees, check first-advance limits, and borrow only what you can repay on the next payday.

- Angular Cheat Sheet - August 4, 2026

- How to Install Plugins in Notepad++ - August 3, 2026

- Best 5 AI Penetration Testing Tools for Web and Mobile Applications - August 2, 2026