Ever been stuck between paydays with bills staring you down? Or maybe you’ve got cash sitting idle and want to earn some good karma—and interest. Welcome to the world of peer-to-peer (P2P) lending apps like Solo Funds, where money needs and excess funds handshake. It’s financial solidarity in your pocket.

In this digital dive, you’ll unravel the ins and outs of microloan platforms that are reshaping personal finance. No suits, no branches, just taps on a screen.

You’re about to see how financial technology services empower folks to bypass traditional loan avenues.

By the end of our chat, you’ll be savvy to the alternative lending platforms scene. I’m talking risk assessments, the loan approval process, all peppered with user-generated stories.

And yeah, the realm of instant loan apps beckons with convenience, but it’s not all sunshine and low APRs.

We’ll get real about the nuts and bolts—think trust, safety policies, and staying in the clear with financial regulations. Ready for the scoop on how to either borrow smart or invest with impact?

Let’s get the financial wheel spinning!

Apps Like SoLo Funds To Check Out

| App Name | Type of Service | Key Features | Interest Rates | Loan/Advance Limits | Credit Check | Special Feature |

|---|---|---|---|---|---|---|

| Lenme | P2P Lending/Investing | Investment & loan opportunities, digital platform | Varies by lender | Up to lender | Depends on lender | User-friendly interface |

| Zirtue | Loan Agreements | Personal loans among friends, automated repayments | 0% – Agreement based | $50 – $10,000 | No | Loans with friends without awkwardness |

| Kiva | Microfinancing | Global impact loans, community funding, no-interest loans | 0% | $25 – No upper limit | No | Interest-free global lending |

| Possible Finance | Short-Term Loans | Small loans, quick funding, no-credit-check | High | Up to $500 | Soft check | No-credit-check loans |

| Prosper | P2P Lending | Personal loans, investment returns, wide range of uses | 7.95% – 35.99% | $2,000 – $40,000 | Yes | Diverse loan uses |

| LendingClub | P2P Lending | Personal and business loans, refinancing | 8.05% – 35.89% | $1,000 – $40,000 | Yes | Debt consolidation expertise |

| MoneyLion | Financial Advisory | Loans, cashback, investing, financial tracking | 0% with membership | Up to $250 advance | Soft check | All-in-one financial toolkit |

| Hundy | Microloans | P2P microloans, fast funding, low loan amounts | 0% – low interest | Up to $100 | No | Microloans within a friendly community |

| Brigit | Cash Advance | Overdraft protection, budgeting, cash advance | 0% | Up to $250 | No | Overdraft protection and budgeting |

| Chime | Online Banking | No fees, early direct deposit, automated savings | 0% | ATM withdrawal up to $500 | No | Fee-free banking and early paycheck access |

| Klover | Cash Advance | No-interest cash advance, financial tools | 0% | Up to $100 | No | Zero-interest cash advance |

| Vola Finance | Cash Advance | Loan advances, account monitoring, financial education | Varies | $100 – $300 | No | Financial insights and education |

| Albert | Financial Advisory | Cash advances, savings, investment advice | 0% with Albert Genius | Up to $250 | No | Financial advice and planning |

Lenme

Next up, Lenme. It’s an app that’s designed to give a seamless experience in peer-to-peer lending. Not just any other app like SoLo Funds, it stands out for its simplicity.

In a nutshell, Lenme works by allowing borrowers to request loans and investors to view the requests and pick which ones they want to fund.

What makes Lenme cool? Its intuitive interface, the simplicity, and transparency. It’s a breath of fresh air.

On the flip side, though, the interest rates can be steep, which can be a bit of a letdown.

Best Features:

- P2P investment opportunities

- Quick loan access

- User-friendly interface

What we like about it: Lenme makes it a breeze to lend or borrow dough without a mountain of paperwork. And the kicker? It all happens on your smartphone!

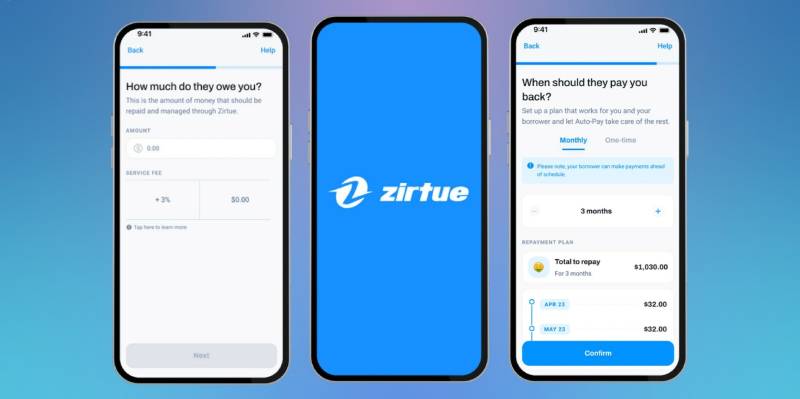

Zirtue

Let’s talk about Zirtue. You know those loans between friends and family that can get messy? Zirtue is trying to make that history.

Zirtue works in a pretty straightforward way. Lenders and borrowers know each other. It could be your buddy, your mom, or even your neighbor.

What’s unique about Zirtue? It has a relationship-based lending model. Making lending between friends and family easier and less awkward.

But just like everything else, it’s got its drawbacks. The lender and borrower have to both be on the app. And let’s face it, not everyone likes mixing finances with relationships.

Best Features:

- Simplified loan agreements with friends

- Automated repayment

- Trustworthy privacy features

What we like about it: Zirtue kicks to the curb any weird money vibes among friends with its straightforward and secured lending-borrowing sitch.

Kiva

Let’s switch gears a little bit and talk about Kiva. This app is focused on helping entrepreneurs who are financially excluded.

Kiva’s system is quite unique. It’s more of a crowdfunding platform where lenders can contribute a portion of the borrower’s request.

One thing that’s cool about Kiva is its mission. It’s not just about lending; it’s about empowering people.

But remember, Kiva is not ideal for emergency funds since it can take time for a loan request to get fully funded.

Best Features:

- Global impact

- Microfinancing services

- Community lending spirit

What we like about it: Slap a high five for Kiva’s rad way of uplifting communities by funneling your spare cash into someone’s life-changing project.

Possible Finance

Taking a closer look at Possible Finance, we find an app that brings a whole different vibe to the table. This digital platform is about providing small loans that can be paid back in installments. Think of it as a friendly hand when you’re a bit strapped for cash.

Just like its name suggests, Possible Finance is all about making it possible for people to access small loans. You apply, get approved, and voila, the money is sent straight to your bank account. It’s as simple as that.

The standout feature here is that Possible Finance reports your payments to credit bureaus. If you’re looking to build credit, this is a sweet deal.

However, the downside is that these loans can be quite costly in terms of interest, especially when compared to traditional personal loans. So it’s something to consider.

Best Features:

- Swift short-term borrowing

- Gentle on credit checks

- Nifty mobile lending platform

What we like about it: We’re all over Possible Finance’s vibe of lending cash with tons of heart and zero stress on your credit score.

Prosper

Let’s kick off with Prosper. Just another app in the sea of apps like SoLo Funds? Not really. Prosper’s been around since 2005, carving out a name as one of the pioneers of the peer-to-peer lending scene.

Now, here’s how it works. Borrowers set the amount they want, the purpose, and investors bid to fund it. It’s a bit like a marketplace for loans.

What sets Prosper apart, though? One thing – they give you a rating. A higher rating could potentially lead to lower interest rates.

But let’s not get carried away. It’s not all sunshine and rainbows. While you might get a potentially lower interest rate, Prosper also has stringent requirements for borrowers.

Best Features:

- Peer-to-peer finance paradise

- Diverse loan purposes

- Snazzy investor returns

What we like about it: What gets us buzzing? The way Prosper flips the script on borrowing, making it a total win-win situation for everyone involved.

LendingClub

Moving onto LendingClub. It’s been in the game since 2007, making it a veteran among peer-to-peer lending apps. Like Solo Funds, LendingClub is an app that matches borrowers with investors, but it’s got a more traditional, bank-like feel to it.

After applying and getting approved, LendingClub pitches your loan to investors who will fund it. Once the loan is fully funded, you receive the money.

What’s awesome about LendingClub is the ability to get a larger loan compared to many other apps like SoLo Funds. Plus, the repayment period is longer, which can ease the pressure of payback time.

However, LendingClub isn’t for everyone. It has pretty high credit score requirements, which might make it a no-go for some folks.

Best Features:

- Debt consolidation wizards

- A wide array of loan options

- Spiffy online application

What we like about it: LendingClub nails it with their chill approach to loans, and that sweet online application is the cherry on top.

MoneyLion

Let’s take a walk on the wild side with MoneyLion. This isn’t just another lending app. It’s a whole financial hub, with a ton of features designed to help you take control of your money.

Borrowing with MoneyLion involves joining their membership program, where you have access to small loans with zero interest. Yes, you heard that right, zero interest.

MoneyLion’s whole vibe of being more than just a lending app sets it apart. Plus, that zero interest feature is pretty hard to beat.

The downside? Well, you’ll need to pay for the membership, which might not be up everyone’s alley.

Best Features:

- Financial toolkit in one app

- Cashback rewards

- Investment features

What we like about it: MoneyLion has us jazzed with their all-in-one approach. Loans, budgeting, investing – they’ve rolled it all into one slick package.

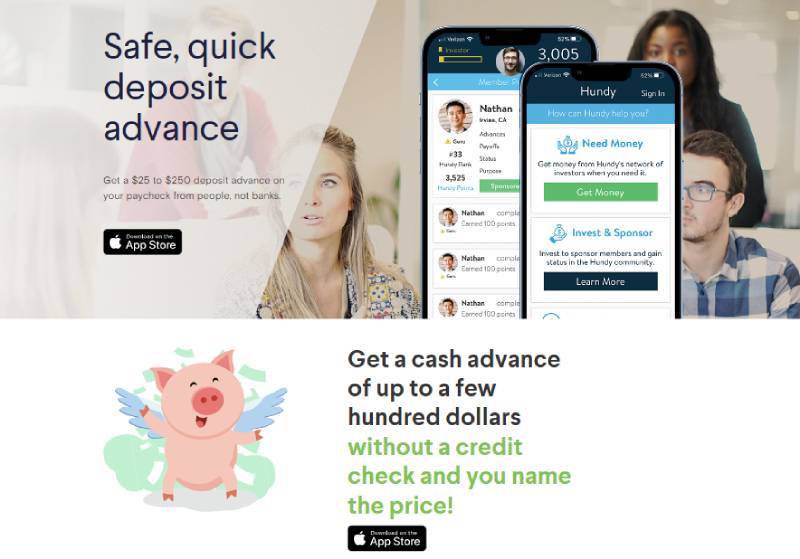

Hundy

Alright, let’s shift our focus to Hundy. It’s a community-based lending app where people can lend and borrow small amounts of money.

Just like the others, you apply, get approved, and receive your funds. It’s as easy as pie.

What sets Hundy apart is the community aspect. It feels more friendly and less transactional. Plus, you get rewards for paying back on time, which is a nice touch.

However, the loans offered are pretty small, so it’s not the best option if you need a significant amount of cash.

Best Features:

- Instant loan access

- Peer-to-peer microloans

- Straightforward experience

What we like about it: Hundy’s the real MVP for those ‘need cash yesterday’ moments, dishing out funds faster than you can spell H-U-N-D-Y!

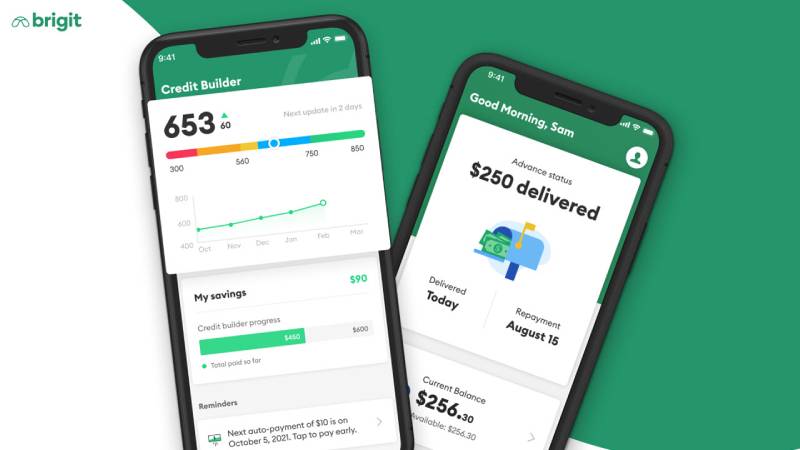

Brigit

Let’s head over to Brigit. This app is all about preventing overdraft fees by offering small advances. Picture it as your mini financial safety net.

So, how does it work? Brigit syncs up with your bank account, keeps an eye on your balance, and if it’s looking like you might overdraft, Brigit sends you a cash advance.

Cool, right? Brigit’s overdraft protection is a real game-changer. And what’s more, they also provide budgeting tools to help you keep track of your spending.

The downside? Well, you’ve got to pay a monthly fee to use Brigit, and that might be a turn-off for some.

Best Features:

- Overdraft protection

- Quick cash advance

- Smart budgeting tools

What we like about it: Brigit gets a high-five for keeping our bank accounts out of the red zone with that speedy cash boost just when you need it.

Chime

Next up, we have Chime. It’s not just another lending app, it’s a full-blown online bank with a killer feature: SpotMe.

SpotMe works like this: if you’re about to overdraft, Chime covers you up to a certain limit. Once you deposit again, Chime takes back what it covered, no fees or interest. It’s a pretty neat way to dodge overdraft fees.

What makes Chime awesome? It’s an all-in-one banking solution. It’s not just about lending, but also spending, saving, and managing your money.

On the downside, Chime’s customer service is primarily online, which might be a drawback if you prefer in-person assistance.

Best Features:

- No overdraft fees

- Automated saving

- Get paid early

What we like about it: Chime’s cool beans with making paydays come early, and who doesn’t love getting their hands on the moolah ahead of schedule?

Klover

Let’s move onto Klover. This app is here to help you with small advances on your paycheck. No interest, no credit check, just a safety net when you need it.

Klover works by giving you access to your earned wages ahead of payday. It’s your money; Klover just helps you access it when you need it.

Klover’s feature that stands out? Definitely the ability to access your paycheck early. Also, they provide financial wellness tools to help you manage your money better.

However, you have to pay a subscription fee, which could be a negative for some.

Best Features:

- Payday advances with no interest

- Financial insights

- Simple borrowing process

What we like about it: Klover sets our hearts racing with those zippy cash advances, and guess what? No interest got us over the moon!

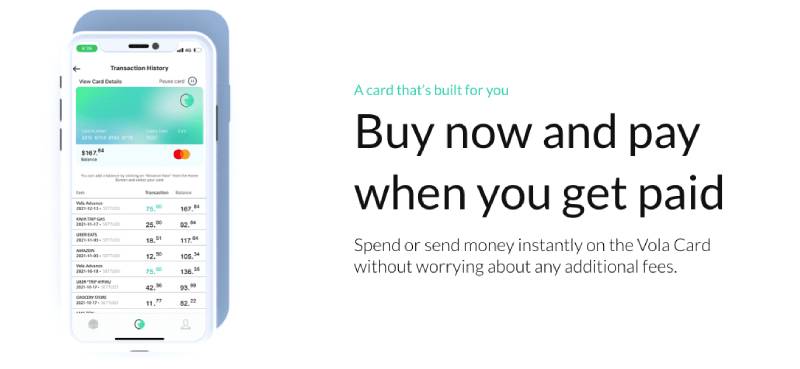

Vola Finance

Alright, onto Vola Finance. It’s a lending app specifically designed for college students. It’s all about helping you out with small loans when you’re in a pinch.

You apply, get approved, and get your loan. Vola Finance also provides a bunch of educational content to help you become more financially savvy.

What’s unique about Vola? It’s focus on college students and its educational resources.

Downside? The loan amounts are relatively small, and there’s a membership fee, which might not be ideal for everyone.

Best Features:

- Advance loans on demand

- Financial education

- Account monitoring

What we like about it: Vola gets a hat tip for dropping knowledge bombs while padding your wallet – it’s like your smart money whisperer.

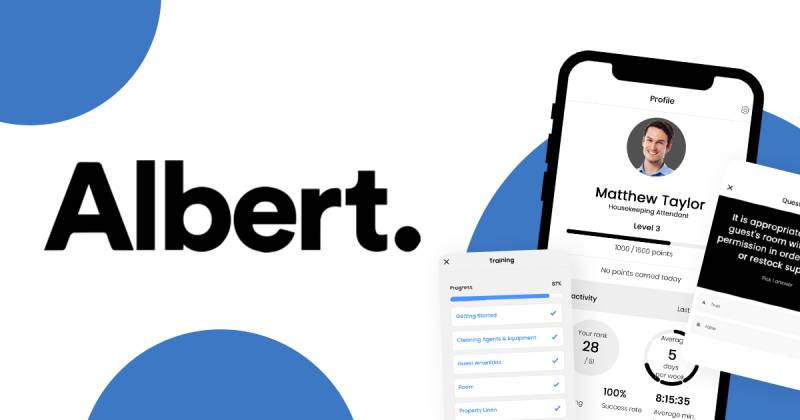

Albert

Last but definitely not least, we have Albert. This app is like your personal financial assistant. It’s got budgeting tools, automatic savings, and even a feature to advance some cash when you need it.

Albert’s genius feature is their smart savings. Albert studies your spending and then automatically sets aside money you can afford to save.

Albert’s cool, but keep in mind that you’ll need to subscribe to Albert Genius to access the cash advance feature.

Best Features:

- Cash advances

- Automated savings

- Personal finance advice

What we like about it: Albert is the talk of the town ’cause it’s a jack-of-all-trades: loans, savings, investing advice—all rolled into one snazzy app.

Comparison of SoLo Funds Alternatives

So, we’ve got all these apps like SoLo Funds lined up, right? Time to see how they stack up against each other. Let’s get into the nitty-gritty details.

Comparison of Key Features

First, let’s look at key features. Each one has its own selling points.

Prosper stands out with its person-to-person lending platform, giving you a chance to invest in and borrow from real people.

Lenme? It’s all about providing a marketplace for lenders and borrowers to meet. Pretty neat, huh?

Zirtue offers something unique with its relationship-based lending. Need a loan? Ask a friend on Zirtue. Simple as that.

Kiva, on the other hand, focuses on socially impactful loans. It’s all about helping out people in need.

Possible Finance is about affordable short-term loans. They’re here to help you out when you need it, without the killer interest rates.

LendingClub? It’s another peer-to-peer lending platform, but they also offer a suite of financial products.

MoneyLion, Hundy, Brigit, Klover, and Albert all provide cash advances. Overdraft protection and early access to your paycheck are their go-to features.

Chime is the full package. It’s a whole bank in an app, complete with overdraft protection and no hidden fees.

And Vola Finance? They’re all about helping college students out with loans and financial education.

Comparison of Pros and Cons

Now, the pros and cons. All of these apps have their upsides and downsides.

Prosper, Lenme, and LendingClub provide a unique platform for borrowing and lending, but the loan process can be a bit lengthy.

Zirtue lets you borrow from people you know, but you have to convince them to join and lend to you.

Kiva is all about making a difference, but the loans aren’t for personal use.

Possible Finance, MoneyLion, Hundy, Brigit, Klover, and Albert all provide short-term financial help, but they require a subscription or membership fee.

Chime offers a bunch of banking services, but if you’re a fan of in-person customer service, they might not be for you.

Vola Finance focuses on college students, which is great if you are one, but not so much if you’re not.

Choosing the Right Alternative for Your Needs

So, which of these apps like SoLo Funds is the right fit for you? Well, it depends.

Looking for a full banking service? Chime might be your pick. Just need a little advance on your paycheck? Maybe give Brigit or Klover a shot. Want to borrow from or lend to people you know? Zirtue‘s got you covered. Looking to make a difference with your loan? Check out Kiva.

The bottom line? It’s all about finding the app that fits your needs and lifestyle. Remember, the best app for you is the one that helps you achieve your financial goals, without causing you any headaches.

So, go ahead. Check these apps out. Your ideal Solo Funds alternative is out there waiting for you.

Understanding Peer-to-Peer Lending

You’ve probably heard the term peer-to-peer lending getting thrown around a lot. Let’s break it down, shall we?

Definition of Peer-to-Peer Lending

Imagine you’re chilling at a cafe. Your mate, who’s sitting across from you, needs some cash for this cool gig happening over the weekend. You lend them some, they give it back after the weekend. Easy, right? That’s the essence of peer-to-peer lending. Just replace the cafe with an app and your mate with someone you might not know, and voilà!

How Peer-to-Peer Lending Works

So, let’s say you’re on one of these apps like SoLo Funds. You set up your profile, pop in how much you need, and why. On the flip side, there are people ready to lend. They see your story, decide to help out, and bam! Transaction complete. Repayments? Usually done through the app with some added interest.

Benefits and Drawbacks of Peer-to-Peer Lending

The cool thing about these apps? It’s super flexible. You aren’t bound by heaps of paperwork or waiting ages for approval.

Pros:

- Quicker approvals

- Flexible amounts to borrow

- Potentially lower interest rates

But… (yeah, there’s always a but)

Cons:

- Risk of default (for lenders)

- Interest rates can sometimes be higher (for borrowers)

- Not as regulated as traditional banks

FAQ about apps like SoLo Funds

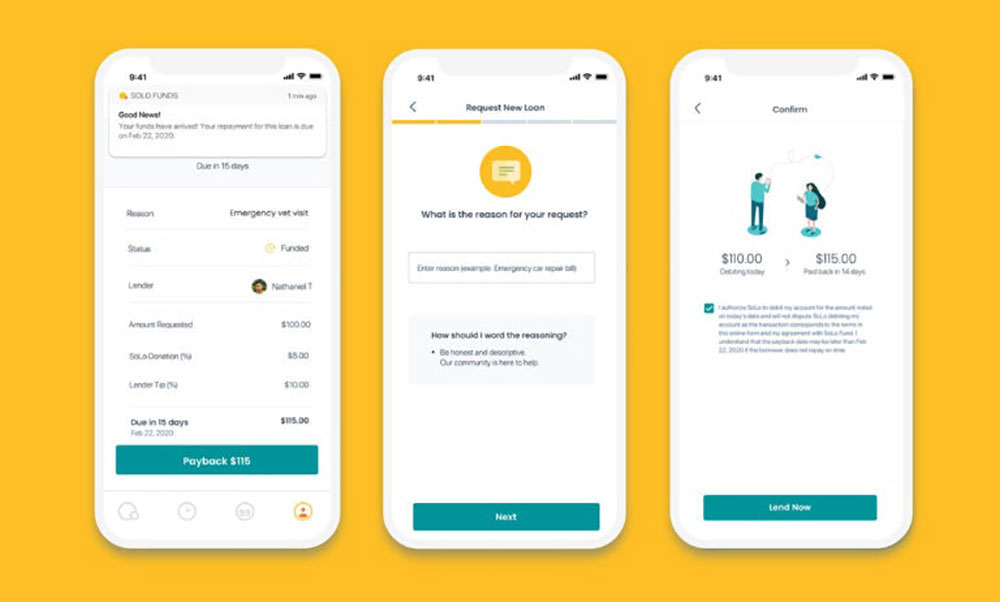

How does SoLo Funds work?

SoLo Funds, huh? Well, it’s essentially a platform that connects borrowers to lenders. Kind of like a community for peer-to-peer lending. What you do is set up an account, throw in your personal info, and post a loan request.

If you’re on the other side, looking to lend, you just review requests and decide who to help out. Interest rates are determined by the borrower, but there are guidelines to prevent anything too outrageous.

What’s the deal with the security on SoLo Funds?

So you’re worried about your info on SoLo Funds? Totally get it. They actually use bank-level encryption to protect your data, and your account is verified through your mobile device.

So yeah, they take your privacy pretty seriously. Also, keep in mind that transactions go through bank accounts or cards, not directly through the app, which is an added layer of security.

Is SoLo Funds legit?

Alright, you’re skeptical. I feel you. But yes, SoLo Funds is legit. It’s got its share of positive reviews and it follows the regulations for peer-to-peer lending. Now, does that mean every experience will be positive?

No, not necessarily. Like any platform, it’s got its flaws. But it’s not a scam or anything like that. Just remember to do your own research and make wise decisions.

How long does it take to get a loan on SoLo Funds?

Oh, you’re in a rush? Well, the speed at which you get a loan on SoLo Funds depends on a few things. Mainly, how quickly a lender decides to fund your request.

Once a lender commits, the funds should be transferred in 1-2 business days. So, not instant, but not too bad either. But hey, just a heads up, weekends and holidays can slow things down a bit.

Can I trust the lenders on SoLo Funds?

Well, trust is a big word, right? SoLo Funds doesn’t exactly vet lenders, so there’s no guarantee. What they do, however, is facilitate communication between lenders and borrowers.

You get to chat, ask questions, and hopefully get a feel for each other. The decision to trust or not, well, that’s up to you. Just remember, use your judgement and don’t rush into anything.

What are the interest rates like on SoLo Funds?

Interest rates, yeah, they can be a deal breaker. On SoLo Funds, it’s the borrower who sets the rate. However, it can’t exceed 36%. So you won’t be seeing any crazy high numbers.

The average, from what I’ve seen, tends to hover around 10-15%. Not too shabby, but always compare with other options, you know?

How do I repay a loan on SoLo Funds?

Repaying a loan on SoLo Funds is pretty straightforward. Once the loan is due, the amount is automatically debited from your linked account. Easy peasy.

If there’s an issue, like insufficient funds, they’ll try again in a few days. Now, if you’re really in a bind, there’s a chance to negotiate an extension with your lender. Communication is key here, just be honest and upfront.

What happens if I can’t repay the loan on SoLo Funds?

So, you’re worried about not being able to pay back? Look, things happen, and SoLo Funds gets that. If you can’t repay the loan, you should reach out to your lender ASAP and explain the situation.

Maybe you can work out an extension. If you don’t pay and don’t communicate, it’s reported to the credit bureaus. So it’s super important to not just ignore the situation, okay?

Are there any fees associated with using SoLo Funds?

Fees, the necessary evil. On SoLo Funds, borrowers pay a small fee, which is usually a percentage of the loan. It’s added to the loan amount and paid back with the rest.

Lenders, on the other hand, get charged a transaction fee, but that’s about it. No hidden fees or anything shady. They lay it all out there for you to see.

What happens if a lender doesn’t fund my loan on Solo Funds?

Oh, you’re worried about not getting funded? Yeah, that can happen. If a lender doesn’t fund your loan, it stays on the platform for a period of time. Other lenders can see it and decide to fund it.

If no one steps up, the request eventually expires. It’s not a surefire thing, but don’t lose hope. You can always create a new request or try to improve your profile to attract lenders.

Conclusion on apps like SoLo Funds

Well, we’ve been on quite a journey together, haven’t we? Diving into the world of apps like SoLo Funds and all. Let’s hit the brakes and recap what we’ve learned.

SoLo Funds started us off, a beacon in the world of peer-to-peer lending, connecting lenders and borrowers like never before. But it’s not the only fish in the sea, far from it. From lending platforms like Prosper and Lenme to full-blown banks like Chime, we’ve seen a whole rainbow of alternatives.

Each app had something to bring to the table. Whether it’s the relationship-based lending from Zirtue, the socially impactful loans from Kiva, or the short-term help from Possible Finance, MoneyLion, Hundy, Brigit, Klover, and Albert, there’s no shortage of options.

Sure, every app has its pros and cons. Maybe the lending process is a bit lengthy, or maybe you need a subscription. Maybe you’re a college student looking for a loan. Or maybe you’re not.

But at the end of the day, each one of these apps like SoLo Funds can give you something unique.

Alright, let’s wrap this up. You’re here because you’re looking for an alternative to SoLo Funds, right? And now, you’ve got a whole list to choose from.

Remember, it’s not about which app is the best. It’s about which app is the best for you. Do you need a quick cash advance? Or maybe you’re after the full banking package? Each app offers something different, and what matters is that it matches what you need.

If you liked this article about apps like Solo Funds, you should check out this article about apps that pay you to walk.

There are also similar articles discussing apps like MoneyLion, cash advance apps that work with Chime, cash advance apps that don’t use Plaid, and apps that pay instantly to Cash App.

And let’s not forget about articles on apps like Cash App, apps that make you money, apps like Brigit, and money apps like Dave.