Rent is due on the 1st, but your paycheck doesn’t always agree.

For millions of renters, that timing gap is where the stress lives. Harvard’s Joint Center for Housing Studies found a record 22.6 million renter households spent more than 30% of their income on rent in 2023 alone.

Flex Rent helped fix that by splitting your monthly payment into two installments. But it requires a minimum credit score, and landlord participation can be a barrier. Not everyone qualifies.

That’s exactly why apps like Flex Rent keep growing. From cash flow-based platforms like Livble to no-credit-check tools like Kasheesh, there are now real alternatives built for renters at every financial stage.

This guide covers the 10 best flexible rent payment options available right now, including how each one works, what it costs, and who it actually fits.

Apps Like Flex Rent

Flex Rent splits your monthly rent into two payments and pays your landlord upfront. It costs $14.99/month plus 1% of your rent, requires a credit score of at least 500-580, and needs landlord participation in some cases. That combination rules out a lot of renters.

According to Till’s 2021 data, 41% of workforce housing residents had been late on rent at least once in the previous six months. Demand for flexible rent payment options has only grown since then. The apps below cover the full range: installment plans, card-splitting tools, credit-building programs, and deferred payment services.

| App | Payment Style | Credit Check | Landlord Required |

| Livble | Up to 4 installments | Cash flow-based | Sometimes |

| Rent App | 2 payments (split) | Eligibility review | No |

| Zenbase | 2 payments | Yes | Yes |

| Deferit | 4 installments | Soft check | No |

| Kasheesh | Multi-card split | No | No |

| Bilt Rewards | Rewards + reporting | Hard check | Sometimes |

| Best Egg | Custom schedule | 640+ recommended | Yes |

| Splitit | Credit card installments | No | No |

| Esusu | Split Pay + reporting | Yes | Yes |

| Jetty | Pay by 24th of month | Yes | Yes |

Livble

Livble is a flexible rent payment app that splits your monthly rent into 2, 3, or 4 installments for renters who need more control over their cash flow. It skips traditional credit scores in favor of cash flow underwriting, and works on iOS and Android.

What Does Livble Do?

Livble pays your landlord the full rent amount upfront, then lets you repay in installments throughout the month. It integrates directly into property management portals like TurboTenant and Buildium.

How Is Livble Similar to Flex Rent?

- Both pay landlords upfront and let tenants repay in chunks

- Both require an eligibility check before first use

- Both offer optional rent reporting to credit bureaus

How Is Livble Different from Flex Rent?

Livble uses cash flow underwriting instead of credit scores, approving roughly 3x more applicants at the same default rates, according to Plaid’s case study on the platform.

It also allows up to 4 installments versus Flex’s 2, and charges a per-use origination fee rather than a flat monthly membership. If you don’t split rent that month, you pay nothing.

Who Is Livble Best For?

Livble suits renters with limited credit history who need more than two installment options and pay through a TurboTenant or Buildium portal.

Key Features of Livble

- Split options: 2, 3, or 4 installments per month

- Underwriting: Cash flow data via Plaid, not just credit scores

- Credit reporting: Reports to major bureaus on-time payments

- Fee structure: Per-use origination fee; no charge in months you don’t split

Pricing

- Free plan: No – fee applies when you split

- Per-use fee: Origination fee varies by timing; $20 extra for after-hours Instant-Split

- Late fee: $15 if balance unpaid after 45 days

- Free trial: No

Rent App (Split Pay)

Rent App is a rent installment platform that splits your monthly rent into two equal payments, with the second due two weeks after the first. It works with both direct landlord payments and all major resident portals, with no landlord involvement needed.

What Does Rent App Do?

Rent App generates a virtual bank account you enter into your resident portal. When rent is pulled, it automatically handles the split behind the scenes. It also reports on-time payments to credit bureaus through optional autopay enrollment.

How Is Rent App Similar to Flex Rent?

- Both split rent into two payments aligned with paycheck schedules

- Both pay landlords the full amount upfront

- Both offer credit reporting to help build payment history

How Is Rent App Different from Flex Rent?

Rent App works with any resident portal that accepts ACH/eCheck payments, with no landlord sign-up required. Flex can sometimes require landlord participation for direct-pay setups.

Rent App splits payments evenly 50/50, while Flex’s split is determined by an approved credit line, which can be unequal. Rent App also launched full portal compatibility as of May 1, 2025.

Who Is Rent App Best For?

Rent App suits bi-weekly earners who want an even 50/50 split with zero landlord involvement and free credit reporting through autopay.

Key Features of Rent App

- Split structure: 50/50 – first half on due date, second half two weeks later

- Portal compatibility: Works with all ACH-enabled resident portals

- Credit reporting: Free via autopay enrollment

- Approval speed: Results within 1 business day

Pricing

- Free plan: No

- Monthly fee: Added to first split payment (exact amount not publicly listed)

- Free trial: No

Zenbase

Zenbase is a Canadian rent splitting service that divides your monthly rent into two payments timed around your paycheck cycle. It targets the mismatch between rent due dates (usually the 1st) and bi-monthly pay schedules.

What Does Zenbase Do?

Zenbase pays your landlord on time and lets you repay in two installments across the month. It also reports payments to credit bureaus and partners with property management companies directly.

How Is Zenbase Similar to Flex Rent?

Both services advance full rent to the landlord and let tenants repay in installments. Both require landlord or property participation, and both run a credit check during onboarding.

How Is Zenbase Different from Flex Rent?

- Zenbase is primarily a Canadian platform; Flex operates in the US

- Zenbase only offers a 2-payment split; Flex also offers 2 payments but with a different fee model

- Pricing: Zenbase starts at $9.90/month plus 0.75% of rent; Flex charges $14.99/month plus 1%

Who Is Zenbase Best For?

Zenbase suits Canadian renters at participating properties who need a simple two-payment split with built-in credit reporting.

Key Features of Zenbase

- Split: 2 installments per month

- Credit reporting: Reports to major bureaus

- Region: Primarily Canada

- Integration: Works via partner property management platforms

Pricing

- Free plan: No

- Paid plan: From $9.90/month plus 0.75% of rent

- Free trial: No

Deferit

Deferit is a bill deferral app that splits large bills, including rent and utilities, into four interest-free installments. No credit check is required for the soft inquiry process, and it works independently of your landlord.

What Does Deferit Do?

You submit your bill to Deferit, it pays the provider directly, and you repay over four installments. It covers rent, utilities, insurance, and other recurring bills up to a $2,000 cap.

How Is Deferit Similar to Flex Rent?

Both services pay your landlord directly and let you spread the cost over time. Both also offer credit reporting features, and both are designed for renters who need short-term cash flow help.

How Is Deferit Different from Flex Rent?

Deferit’s starting balance is only $200-$400, which won’t cover most people’s full rent. It’s better suited for partial rent coverage or utility bills.

It has a $2,000 maximum per bill, no landlord involvement needed, and charges zero interest. Unlike apps similar to Sezzle, Deferit is specifically built for recurring household bills, not retail purchases.

Who Is Deferit Best For?

Deferit suits renters with lower rent amounts (under $2,000) or those needing to split utility bills, who want zero interest and no hard credit pull.

Key Features of Deferit

- Split: 4 interest-free installments

- Max bill amount: $2,000

- Starting balance: $200-$400 for new users

- Landlord required: No – pays bills directly

Pricing

- Free plan: No

- Monthly membership: Required before approval (fee amount varies)

- Interest: None

- Free trial: No

Kasheesh

Kasheesh takes a completely different approach to flexible rent payments. Instead of advancing your rent, it lets you split a single payment across up to five cards, including credit, debit, and prepaid gift cards. No credit check. No landlord approval.

What Does Kasheesh Do?

You link your cards, set how much to charge each one, and Kasheesh generates a single virtual Mastercard that handles the split. Your landlord sees one normal payment. You’ve used multiple funding sources.

How Is Kasheesh Similar to Flex Rent?

Both help renters avoid the strain of one large payment hitting a single account at once. Both work with most landlords and payment portals, and both are designed for cash flow management.

How Is Kasheesh Different from Flex Rent?

Kasheesh doesn’t advance rent or create a loan. It just redistributes where the money comes from. There’s no credit check and no installment plan. It also lets you earn rewards across multiple cards simultaneously, which Flex doesn’t support.

Kasheesh offers 1-1.5% rewards on transactions, making it useful for renters who want to maximize credit card benefits while managing cash flow.

Who Is Kasheesh Best For?

Kasheesh suits renters who have funds spread across multiple cards or accounts and want to consolidate them into a single rent payment without a credit check or landlord involvement.

Key Features of Kasheesh

- Card split: Up to 5 cards (credit, debit, or prepaid)

- Credit check: None required

- Rewards: 1-1.5% on transactions

- Landlord approval: Not needed

Pricing

- Free plan: No

- Paid plans: Subscription required (exact pricing not publicly listed)

- Free trial: No

Bilt Rewards

Bilt Rewards is less about splitting rent and more about making it work for you. It’s a loyalty program and credit card that earns points on rent payments and reports to all three major credit bureaus for free.

What Does Bilt Do?

Bilt lets you earn points on your largest monthly expense and redeem them for travel, fitness, and even future rent. If your landlord doesn’t accept cards, Bilt mails them a check.

How Is Bilt Similar to Flex Rent?

Both are fintech tools built specifically around the rent payment process. Both offer credit bureau reporting, and both are designed to give renters more financial value from paying rent each month.

How Is Bilt Different from Flex Rent?

- Bilt doesn’t split payments – it focuses on rewards and credit building, not installments

- Requires a 670-850 credit score (good to excellent), much higher than Flex’s 500-580 minimum

- Performs a hard credit check at application, which affects your score

Who Is Bilt Best For?

Bilt suits renters with good-to-excellent credit who want to earn travel rewards and build credit history through rent, rather than split payments across the month.

Key Features of Bilt

- Rewards: Points on rent redeemable for travel, fitness, future rent

- Credit reporting: All three major bureaus, free

- Credit card: Bilt World Elite Mastercard, no annual fee

- Landlord check: Not required for all features; Bilt mails a check if needed

Pricing

- Free plan: Yes – free to join Bilt

- Credit card: No annual fee

- Processing fees: None for rent payments via Bilt

- Free trial: N/A

Best Egg Flexible Rent

Best Egg Flexible Rent, formerly known as Till, offers customized rent payment schedules for tenants at participating properties. It partners directly with landlords and property management companies rather than operating as a standalone consumer app.

What Does Best Egg Do?

Best Egg integrates into property management portals like AppFolio, creates a personalized payment schedule for each tenant, and sends automated reminders to keep payments on track. Landlords receive full rent upfront.

How Is Best Egg Similar to Flex Rent?

Both pay landlords the full amount at the start of the month and let tenants repay over time. Both require a credit check and are designed to reduce late payments in the rental market.

How Is Best Egg Different from Flex Rent?

Best Egg requires a 640+ credit score, higher than Flex’s 500-580 minimum, and only works at around 10 million enrolled homes in the US. It focuses on the landlord-side relationship rather than the consumer app experience.

The fee structure isn’t publicly listed. Costs are typically built into property management agreements, so tenants may or may not pay directly.

Who Is Best Egg Best For?

Best Egg suits tenants at AppFolio or other enrolled properties who have a 640+ credit score and want a customized repayment schedule with automated reminders.

Key Features of Best Egg

- Integration: AppFolio and other property management portals

- Schedule: Custom payment plans built around tenant cash flow

- Availability: Around 10 million enrolled US homes

- Credit requirement: 640+ recommended

Pricing

- Free plan: Depends on property arrangement

- Paid plans: Fee structure varies by property; not publicly listed

- Free trial: No

Splitit

Splitit is a buy now, pay later platform that has partnered with Letus (formerly RentMoola) to bring installment payments to rent. It uses your existing credit card line, with no new loan or separate application needed.

What Does Splitit Do?

Splitit holds a temporary authorization on your credit card and releases funds in installments on a set schedule. You pay rent over time using your existing credit limit. No new account. No credit pull.

How Is Splitit Similar to Flex Rent?

Both let renters spread rent across multiple payments without paying the full amount at once. Both pay the landlord the full rent upfront, and both are designed to reduce cash flow pressure around rent day.

How Is Splitit Different from Flex Rent?

Splitit only works with a single credit card. No debit cards. No prepaid cards. No mixing payment sources. Unlike apps comparable to Affirm, Splitit doesn’t issue new credit. It works off what you already have.

There are no additional fees or interest from Splitit itself, though your credit card’s interest applies if you carry a balance.

Who Is Splitit Best For?

Splitit suits renters who have enough available credit on a single card and want to break rent into installments without any new loan or credit check.

Key Features of Splitit

- Payment method: Single credit card only (no debit or prepaid)

- Credit check: None – uses existing credit line

- Fees: No fees from Splitit; standard card interest may apply

- Partner platform: Letus (formerly RentMoola)

Pricing

- Free plan: Yes – no fees from Splitit

- Interest: None from Splitit; credit card interest may apply if balance not paid

- Free trial: N/A

Esusu

Esusu is a financial technology platform focused on rent reporting and credit building. It offers Split Pay, a zero-interest short-term payment option funded through its non-profit partner, Stable Home Fund.

What Does Esusu Do?

Esusu reports on-time rent payments to all three major credit bureaus and offers a Split Pay feature that covers part of your rent as a 30-day, zero-interest loan. It integrates with property management systems and targets renters who want long-term financial improvement alongside payment flexibility.

How Is Esusu Similar to Flex Rent?

Both advance rent on your behalf and let you repay over the month. Both report to credit bureaus and are designed for renters who want to improve their financial standing.

How Is Esusu Different from Flex Rent?

- Esusu Split Pay loans are funded by a non-profit, making it zero-interest

- Requires a Plus or Premium Esusu subscription before accessing Split Pay

- Application must be submitted at least 7 business days before rent is due

Who Is Esusu Best For?

Esusu suits renters at participating properties who want zero-interest payment flexibility combined with active credit-building through bureau reporting.

Key Features of Esusu

- Credit reporting: All three bureaus, on-time payments only

- Split Pay: Zero-interest 30-day loan via Stable Home Fund

- Subscription required: Plus or Premium plan for Split Pay access

- Lead time: Apply at least 7 business days before due date

Pricing

- Free plan: Basic tier available; Split Pay requires Plus or Premium

- Paid plans: Subscription pricing varies by plan tier

- Free trial: No

Jetty

Jetty is a renter financial services platform that originally offered Jetty Rent, letting tenants pay on the 1st with repayment due by the 24th. As of late 2025, availability of the rent product has been inconsistent, though its deposit and credit reporting services remain fully active.

What Does Jetty Do?

Jetty covers your full rent on the 1st and gives you until the 24th to repay in one or more installments. Jetty Credit reports payments to TransUnion, Experian, and Equifax. Jetty Deposit replaces the standard security deposit with a low monthly premium and a surety bond.

How Is Jetty Similar to Flex Rent?

Both pay landlords upfront on the 1st, require a credit check and application process, and include optional credit reporting features.

How Is Jetty Different from Flex Rent?

Jetty gives tenants until the 24th of the month to repay in full, rather than splitting across a fixed schedule. Approval takes several business days and applies to the following month’s rent. Jetty’s Rent product is currently in limited pilot.

The deposit replacement product is a meaningful differentiator. Jetty Deposit starts at around $7/month for $1,000 of coverage, which can save renters thousands at move-in.

Who Is Jetty Best For?

Jetty suits renters at enrolled properties who want flexible repayment timing until the 24th, or who need a security deposit alternative at move-in.

Key Features of Jetty

- Jetty Rent: Full rent paid on the 1st; repay by the 24th (limited availability)

- Jetty Deposit: From ~$7/month for $1,000 of surety bond coverage

- Jetty Credit: Reports to TransUnion, Experian, and Equifax

- Landlord required: Yes

Pricing

- Free plan: Free at qualifying properties for Jetty Credit

- Jetty Deposit: Starting around $7/month

- Jetty Rent: Monthly fee applies; amount varies

- Free trial: No

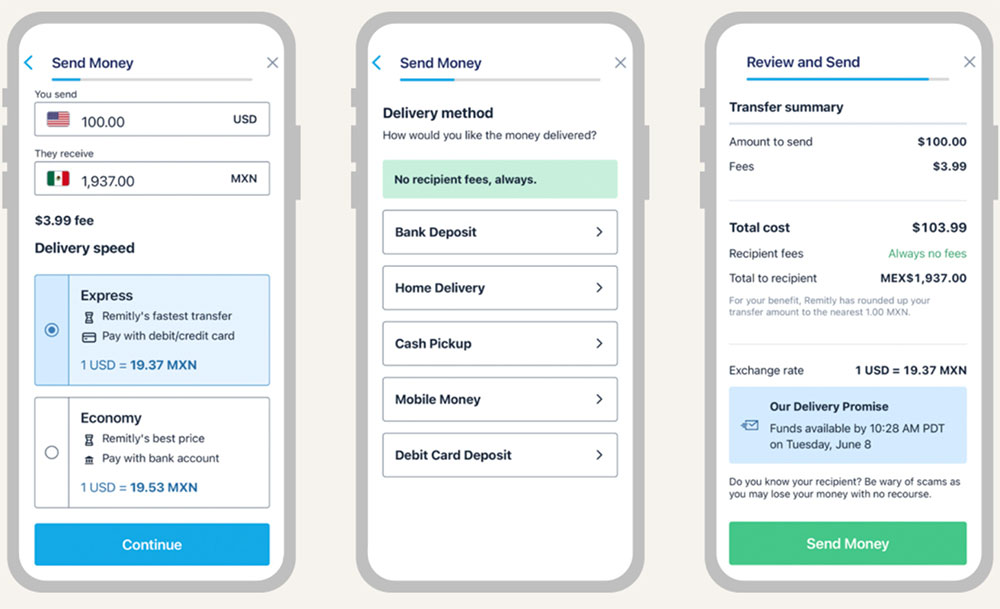

What Is Flex Rent and Why Do Renters Look for Alternatives?

Flex Rent pays your landlord the full rent amount on the 1st of the month. You repay Flex in two installments across the month, with a $14.99 monthly fee plus 1% of your rent.

The demand behind this model is real. Harvard’s Joint Center for Housing Studies found that in 2023, a record 22.6 million renter households spent more than 30% of their income on rent and utilities.

Flex isn’t accessible to everyone, though. The credit score floor sits at 500-580, a soft credit check is required, and landlord participation is sometimes needed for direct-payment setups.

Common rejection reasons include:

- Insufficient bank balance to cover the first payment

- Failed first-payment authorization

- Outstanding balance on the rent ledger

- Expired debit or credit card on file

Till’s 2021 research found 41% of workforce housing residents were late on rent at least once in the prior six months. That number reflects a structural cash flow problem, not just individual financial mismanagement.

The rental split payment app market reached $1.48 billion globally in 2024, growing at 17.9% annually, according to Dataintelo. More apps are entering this space precisely because Flex’s eligibility requirements leave a wide gap.

How Do Rent Installment Apps Work?

Not every app in this category operates the same way. The three core models differ in how money flows, who holds risk, and what credit requirements apply.

| Model | How It Works | Examples | Credit Check |

| Advance and repay | App pays landlord upfront; tenant repays in installments | Flex, Livble, Zenbase | Yes (credit or cash flow) |

| Card splitting | Rent split across multiple cards; landlord gets one payment | Kasheesh, Splitit | No |

| Rewards + reporting | Points earned on rent; credit bureau reporting added | Bilt Rewards | Hard check required |

The advance-and-repay model is what most renters picture when they think about flexible rent payment options. The app essentially acts as a short-term lender.

Livble’s approach stands out. Instead of relying on credit scores, it uses cash flow underwriting via Plaid, approving roughly 3x more applicants at the same default rate compared to credit-score-only models, according to Plaid’s case study on the platform.

The virtual account method is how landlord-free services work. Rent App generates a routing and account number you enter into your resident portal. Your portal sees a standard ACH payment. The split happens behind the scenes.

Credit reporting is a secondary layer built into several of these apps. Payment history makes up 35% of a FICO score, which is why apps like Esusu, Bilt, Livble, and Rent App have made bureau reporting a central feature rather than an afterthought.

Which apps work without landlord approval?

Landlord involvement is the most common friction point. Flex sometimes requires it. Livble and Best Egg require property management portal participation.

Independent options:

- Kasheesh: no landlord involvement; generates a virtual Mastercard

- Deferit: pays bills directly; landlord doesn’t need to know

- Rent App: virtual account numbers work in any ACH-enabled portal

- Splitit: uses existing credit line through Letus-partnered portals

Fannie Mae data shows 58% of renters are more likely to rent from a landlord who reports payments. That stat helps explain why more platforms are building landlord-optional workflows, since tenant demand for these tools is real regardless of property participation.

Which apps have no credit check?

No check required: Kasheesh, Splitit.

Soft check only: Deferit.

Cash flow underwriting (no hard pull): Livble uses Plaid bank data instead of credit scores, which is why it reaches renters that traditional credit-gated apps reject.

Bilt is at the opposite end. It requires a 670-850 credit score (good to excellent) and performs a hard credit check at application. It’s built for renters with established credit who want rewards, not renters looking for emergency payment flexibility.

How to Choose the Right App Based on Your Situation?

The right pick depends on four variables: credit score, whether your landlord participates, how many installments you need, and your rent amount.

| Situation | Best Options | Why |

| No credit / thin credit | Kasheesh, Deferit, Livble | No hard pull; cash flow model |

| Landlord not enrolled | Kasheesh, Deferit, Rent App | Work independently |

| Need 3-4 installments | Livble, Deferit | Both offer up to 4 splits |

| Good credit, want rewards | Bilt Rewards | 670+ score; no processing fee |

| Rent over $2,000 | Flex, Livble, Rent App | Deferit caps at $2,000 |

Redfin’s November 2025 survey found that nearly half of Americans struggle to afford their housing payments. That’s not a niche problem. It spans renters earning $30,000 to $75,000 per year, and even households earning over $75,000 saw cost burden rates rise to 13% in 2023, per Harvard’s JCHS.

If you’re choosing based on cost, run the numbers for your specific rent amount. A $2,000/month rent costs $34.99/month with Flex ($14.99 fee + $20 at 1%). Zenbase charges $9.90 plus $15 (0.75% of $2,000). The difference is small but adds up over 12 months.

Kasheesh is the fastest setup. No credit check. No landlord approval. Same-day. If you need actual installment scheduling rather than card splitting, Deferit is the next-best option for renters with low credit, as long as your rent stays under $2,000.

Esusu’s Split Pay is worth considering for renters at participating properties who want zero-interest financing. Esusu’s partnership with Stable Home Fund funds the loan at 0% for the 30-day repayment period, which no other app in this category matches.

What Are the Fees and Costs Across These Apps?

The rental split payment app market is growing partly because these tools solve a real cash flow problem. But fees matter. A few dollars here and there adds up when it’s monthly.

| App | Monthly Fee | Per-Rent Fee | Interest |

| Flex | $14.99 | 1% of rent | None from Flex |

| Zenbase | $9.90 | 0.75% of rent | None |

| Livble | None | Origination fee (varies by timing) | $15 after 45 days |

| Deferit | Membership required | None | None |

| Bilt | None | None for rent | Card interest applies |

| Splitit | None | None from Splitit | Card interest applies |

Livble only charges when you actually split. If you skip a month, no fee applies. That’s a key difference from Flex and Zenbase, which charge a flat membership regardless of use.

For Kasheesh, the reward play changes the math. If you earn 1-1.5% back across cards and pay balances off monthly, the effective cost approaches zero and potentially goes negative compared to paying rent with a debit card that earns nothing.

Splitit and Kasheesh both carry credit card interest risk. If you carry a balance, standard card APRs (often 20-29%) make this far more expensive than any flat-fee app. Use them only if you can pay each card off monthly.

One hidden cost that rarely gets mentioned: Flex charges a 2.5% processing fee on top of the 1% if you pay using a credit card rather than a debit card. Some buildings also pass through a $3 fee when Flex is used. Both show up in the confirmation screen before you commit.

Do These Apps Help Build Credit?

Only 13% of renters currently benefit from positive rental reporting in their credit files, according to VantageScore’s November 2025 analysis of over 600,000 renters. That’s a significant gap given that 42.5 million renter households exist in the US.

TransUnion found that more than three-quarters of consumers who reported their rent saw credit score improvements, with an average increase of nearly 60 points. For renters with no credit or thin files, that’s not a minor boost.

Which apps report to credit bureaus?

Reports to all three bureaus:

- Esusu (Equifax, Experian, TransUnion)

- Bilt Rewards (all three, free)

- Jetty Credit (TransUnion, Experian, Equifax)

Reports with conditions:

- Livble: reports on-time payments

- Zenbase: reports to major bureaus

- Rent App: free credit reporting via autopay enrollment only

No reporting: Kasheesh, Splitit.

What is the actual credit impact?

Urban Institute research found rent reporting increased credit visibility by 12 percentage points and raised the likelihood of near-prime scores (above 601) by 25% for renters who had low or no scores at enrollment.

Not all outcomes are positive. Renters with higher existing scores risk a small dip because adding a new rental tradeline shortens average credit history length, according to FICO’s vice president of scores and predictive analytics (Urban Institute, 2025).

Esusu’s model is the most compelling long-term play. The platform doesn’t report missed payments to bureaus. It only reports on-time payments, removing the downside risk that other reporting services carry when a payment is late or fails.

Jetty is the exception. Miss a payment with Jetty Credit and you lose the reporting feature permanently. There’s no reinstatement. That’s a meaningful penalty for someone using the service specifically to build credit history.

What Should Renters Know Before Signing Up for Any of These Apps?

Most of the friction in this category comes from eligibility windows and timing requirements that apps don’t advertise upfront. Reading the fine print before the 1st of the month is the only way to avoid a missed payment.

Timing windows that block access:

- Livble: rent due date must fall between the 28th of the prior month and the 9th of the current month

- Esusu Split Pay: application must be submitted at least 7 business days before rent is due

- Jetty Rent: approval applies to the following month’s rent, not the current one

Livble has a “one prior payment” rule. You need at least one successful payment through the TurboTenant or Buildium portal before the Livble option appears in your dashboard. If you’re a new tenant, expect to wait one rent cycle.

State restrictions are also a factor. Livble has noted availability gaps due to state-level regulations, with TurboTenant actively working to restore access in affected states. If the Livble widget doesn’t appear in your dashboard, check whether your state is currently restricted.

What happens when a payment fails:

- Flex: locks you out the following month

- Rent App: notifies your landlord after two failed attempts

- Jetty Credit: removes you from credit reporting permanently

- Deferit: may charge additional fees if payment cancels without notice

The US Census Bureau’s Household Pulse survey found that 41% of renters surveyed between January and September 2024 reported their monthly rent increased by at least $100 in the prior year. These apps exist as a response to that pressure. But they work only if you understand the eligibility rules before you need them, not after.

FAQ on Apps Like Flex Rent

What are the best apps like Flex Rent?

The top alternatives include Livble, Rent App, Zenbase, Deferit, Kasheesh, Bilt Rewards, Best Egg, Splitit, Esusu, and Jetty. Each takes a different approach, from installment plans to card splitting to rewards programs. Your best option depends on your credit score and landlord setup.

Do rent installment apps require a credit check?

Not all of them. Kasheesh and Splitit require no credit check. Deferit runs a soft inquiry only. Livble uses cash flow underwriting via Plaid instead of credit scores, approving roughly 3x more applicants than credit-score-only models at the same default rate.

Can I use these apps without my landlord’s permission?

Yes, several work independently. Kasheesh, Deferit, and Rent App all operate without landlord involvement. Rent App provides virtual routing numbers you enter into any ACH-enabled portal. Your landlord simply receives a standard bank payment.

How much do flexible rent payment apps cost?

Fees vary widely. Flex charges $14.99/month plus 1% of rent. Zenbase starts at $9.90/month plus 0.75%. Livble charges a per-use origination fee only in months you split. Bilt and Splitit charge no monthly fee, though credit card interest may apply.

What happens if I miss a payment on these apps?

Consequences differ by platform. Flex locks you out the following month. Rent App notifies your landlord after two failed attempts. Jetty Credit removes you from its reporting program permanently. Deferit may apply additional fees when payments cancel unexpectedly.

Do these apps help build credit?

Several do. Esusu, Bilt, Livble, Zenbase, and Rent App all report on-time payments to credit bureaus. TransUnion found over 75% of consumers who reported rent saw score improvements, with an average increase of nearly 60 points. Kasheesh and Splitit do not report.

What is the difference between Flex Rent and Livble?

Flex splits rent into two payments and charges a flat monthly fee. Livble offers up to four installments and uses cash flow data instead of credit scores for eligibility. Livble only charges when you actually split, while Flex bills monthly regardless of use.

Can I split rent payments without a credit score?

Yes. Kasheesh has zero credit requirements and splits payments across up to five cards. Deferit runs only a soft check. Livble’s cash flow model approves applicants that traditional credit-gated apps reject, making it a practical option for renters with limited credit history.

Is Deferit a good Flex Rent alternative?

For some renters, yes. Deferit splits bills into four interest-free installments with no landlord involvement required. The main limitation is a $2,000 cap per bill and a starting balance of only $200-$400 for new users, which won’t cover most full rent payments.

Which app is best for earning rewards on rent?

Bilt Rewards is the clear leader here. It earns points on rent with no processing fees, reports to all three credit bureaus for free, and redeems points for travel or future rent. It requires a 670+ credit score and the Bilt World Elite Mastercard.

Conclusion

This conclusion is for an article presenting the strongest apps like Flex Rent available to renters today.

No single app wins for everyone. Livble works best for renters with thin credit. Kasheesh fits those who need same-day setup with no eligibility hoops. Bilt suits renters with solid credit who want rewards on top of rent reporting.

The key is matching the tool to your situation: your credit history, your landlord setup, and how many installment payments you actually need.

Rent affordability isn’t getting easier. Flexible rent payment options, rent deferral tools, and cash advance alternatives exist precisely because the traditional one-lump-sum model no longer fits how most renters get paid.

Pick the app that fits your cash flow. Then use it consistently.

- Angular Cheat Sheet - August 4, 2026

- How to Install Plugins in Notepad++ - August 3, 2026

- Best 5 AI Penetration Testing Tools for Web and Mobile Applications - August 2, 2026