Affirm made buy now, pay later a household term, but it was never the only option.

With 91.5 million Americans expected to use BNPL services in 2025, the demand for flexible installment payment options has never been higher. Some shoppers need wider merchant coverage. Others want to build credit, avoid fees, or finance a flight instead of a sofa.

Different apps solve different problems. Klarna leads on merchant reach. Afterpay keeps things simple. Perpay ties payments to your paycheck. Splitit works with the credit card you already have.

This guide covers the 10 best apps like Affirm available right now, with a clear breakdown of how each one works, what it costs, and who it actually suits.

Apps Like Affirm

The global BNPL market is projected to grow from $42.22 billion in 2025 to $147.27 billion by 2031, a CAGR of 23.15% (ResearchAndMarkets). That kind of growth means more options for shoppers, not fewer.

Below are the 10 best buy now, pay later alternatives to Affirm, covering different use cases, price points, and audiences.

Klarna

Klarna is a fintech lending platform that lets shoppers split purchases into installments or defer payment up to 30 days, for online and in-store buyers globally.

It supports iOS and Android, and operates in over 45 countries with a network of 800,000+ merchants including Amazon, Walmart, and Best Buy.

What Does Klarna Do?

Klarna gives users three payment options at checkout: Pay in 4 (interest-free, biweekly), Pay in 30 Days (full balance, no interest), and monthly financing up to 24 months.

How Is Klarna Similar to Affirm?

- Both offer pay-in-4 and monthly installment plans

- Both use soft credit checks that don’t affect your score

- Both target online shoppers looking for flexible payment plans

How Is Klarna Different from Affirm?

Klarna’s merchant network (800,000+) is significantly larger than Affirm’s (245,000+). It also offers a “Pay in 30 Days” deferred billing option that Affirm doesn’t. Late fees are capped at $7, much lower than most competitors.

In March 2025, Klarna replaced Affirm as Walmart’s official BNPL partner in the US.

Who Is Klarna Best For?

Shoppers who want the widest merchant coverage, a flexible mix of short-term and monthly plans, and access to in-app shopping deals.

Key Features of Klarna

- Merchant network: 800,000+ globally

- Plans: Pay in 4, Pay in 30 Days, monthly up to 24 months

- Late fee cap: $7 per missed payment

- Klarna Card: Virtual and physical card usable anywhere Visa is accepted

Pricing

- Free plan: Yes, Pay in 4 and Pay in 30 are free for consumers

- Paid plans: Monthly financing carries interest (varies by credit profile)

- Free trial: N/A

Afterpay

Afterpay is a buy now pay later app focused on short-term, interest-free installments for retail, fashion, and beauty shoppers. It’s now part of Block, Inc. (formerly Square).

Supports iOS and Android, available in the US, UK, Australia, New Zealand, Canada, and more.

What Does Afterpay Do?

Afterpay splits purchases into 4 equal payments due every two weeks. The first payment is collected at checkout, the remaining three are automatic.

How Is Afterpay Similar to Affirm?

| Feature | Afterpay | Affirm |

| Pay-in-4 option | Yes | Yes |

| Interest on standard plan | None | None |

| Soft credit check | Yes | Yes (Hard check for some long-term loans) |

| Monthly plans | Up to $25,000 limit | Up to 60 months |

How Is Afterpay Different from Affirm?

Afterpay’s minimum purchase is $35, making it more accessible for small purchases. Its late fee is capped at $68 per order (25% of order value), which is higher than Klarna but still capped. Afterpay doesn’t currently report Pay in 4 payments to credit bureaus.

Who Is Afterpay Best For?

Shoppers making smaller retail purchases in fashion, beauty, or lifestyle categories who want zero interest and instant approval with no credit check.

Key Features of Afterpay

- Spending range: $35 to $25,000 per loan

- Payment schedule: 4 payments, every 2 weeks

- Merchants: 15,000+ online and in-store worldwide

- Afterpay Pulse: Rewards program for on-time payment history

Pricing

- Free plan: Yes, no interest on Pay in 4

- Paid plans: Monthly plans available for larger purchases

- Free trial: N/A

Sezzle

Sezzle is a consumer credit alternative that offers pay-in-4 and long-term monthly plans, with a built-in credit-building feature for US and Canadian shoppers.

Available on iOS and Android. Operates primarily in the US and Canada with 41,800+ active merchants.

What Does Sezzle Do?

Sezzle lets users split purchases into 4 interest-free payments over 6 weeks, or choose monthly plans from 3 to 48 months for larger purchases up to $15,000.

How Is Sezzle Similar to Affirm?

Both offer pay-in-4 with no interest. Both use soft credit checks. Both support credit-building through optional reporting to credit bureaus. The range of apps like Sezzle follows a similar model to Affirm’s installment structure.

How Is Sezzle Different from Affirm?

Sezzle Up ($3/month) reports payment history to credit bureaus, a feature Affirm handles differently. Sezzle also allows one free payment reschedule per order, which Affirm doesn’t explicitly offer.

Its initial spending limit of $2,500 per transaction is lower than Affirm’s for qualified users.

Who Is Sezzle Best For?

First-time BNPL users or shoppers with limited credit history who want to build credit while making installment purchases at retail stores like Target and GameStop.

Key Features of Sezzle

- Spending limit: Up to $2,500 (pay-in-4), up to $15,000 (monthly)

- Credit building: Sezzle Up subscription at $3/month

- Payment reschedule: 1 free reschedule per order

- Merchant count: 41,800+ active merchants

Pricing

- Free plan: Yes, standard pay-in-4 is free

- Paid plans: Sezzle Up at $3/month for credit reporting

- Free trial: No

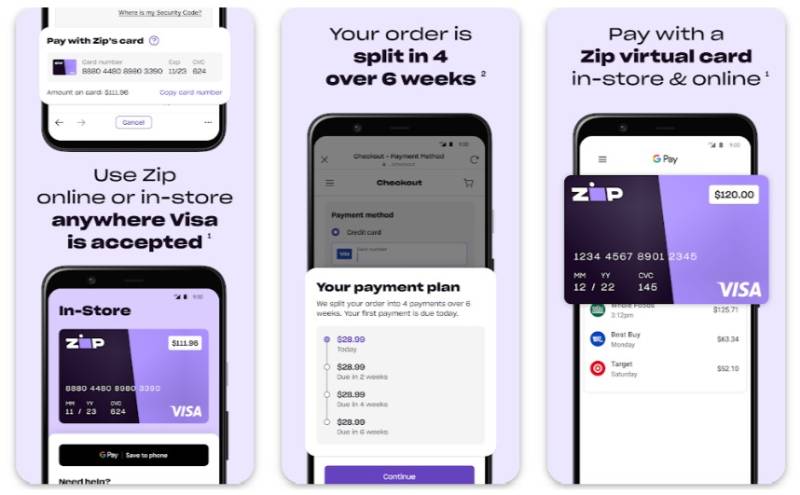

Zip (formerly QuadPay)

Zip is a point-of-sale financing app that lets users pay in 4 installments at almost any retailer using a virtual Zip card, even where BNPL isn’t natively integrated.

Available on iOS and Android. Operates primarily in the US, Australia, and New Zealand.

What Does Zip Do?

Zip issues a virtual Visa card at checkout, allowing users to split purchases into 4 equal payments over 6 weeks at any store that accepts Visa, online or in-store.

How Is Zip Similar to Affirm?

- Pay-in-4 structure with no interest on standard plans

- Soft credit check only, no impact on credit score

- Available for bad credit users with real-time approval

How Is Zip Different from Affirm?

Zip’s virtual card approach means it works at retailers that haven’t integrated BNPL natively, which Affirm can’t do. The tradeoff: Zip charges a $4 to $6 convenience fee per order, whereas Affirm charges no consumer fees at all (only potential interest on longer plans).

Who Is Zip Best For?

Shoppers who want BNPL availability at any retailer, not just Affirm’s partner merchants, and are comfortable paying a small per-order fee for that flexibility.

Key Features of Zip

- Virtual card: Works anywhere Visa is accepted

- Pay in 4: Biweekly payments, 6-week term

- Convenience fee: $4 to $6 per order

- Spending limits: $350 to $2,000 (Zip Pay), higher for Zip Money

Pricing

- Free plan: No, flat convenience fee per order

- Paid plans: $4 to $6 per transaction

- Free trial: N/A

PayPal Pay Later

PayPal Pay Later is a deferred payment platform built directly into the PayPal ecosystem. No new app, no separate account setup, just BNPL at checkout wherever PayPal is accepted.

Available on iOS and Android. Accepted at millions of merchants globally.

What Does PayPal Pay Later Do?

It offers two options: Pay in 4 (4 biweekly payments, 0% APR) and Pay Monthly (longer-term loans from $200 to $10,000, with interest based on credit profile).

How Is PayPal Pay Later Similar to Affirm?

CNBC Select rates PayPal Pay in 4 as the best BNPL option for online shopping in 2026, citing its zero-fee structure and massive merchant availability. Like Affirm, it charges no late fees on Pay in 4 plans.

How Is PayPal Pay Later Different from Affirm?

| Attribute | PayPal Pay Later | Affirm |

| Dedicated app needed | No | Yes |

| Pay in 4 limit | $1,500 | Varies by merchant |

| Credit bureau reporting | No | Yes (Experian, Equifax, TransUnion) |

| Buyer protection | Yes (PayPal Purchase Protection) | No |

Who Is PayPal Pay Later Best For?

Existing PayPal users who want zero-friction BNPL without downloading a new app or creating a new account.

Key Features of PayPal Pay Later

- No late fees: On Pay in 4 plans

- Merchant coverage: Millions of PayPal-integrated stores

- Pay Monthly limit: Up to $10,000

- Buyer protection: Covered under PayPal Purchase Protection

Pricing

- Free plan: Yes, Pay in 4 is interest-free and fee-free

- Paid plans: Pay Monthly carries interest (APR varies by credit)

- Free trial: N/A

Splitit

Splitit is a card-linked installment solution that uses a shopper’s existing credit card to split purchases into monthly payments, with no new credit line and no credit check required.

No dedicated mobile app. Available through merchant integrations on Shopify, WooCommerce, Magento, BigCommerce, and Wix.

What Does Splitit Do?

Splitit places a hold on the full purchase amount on the user’s existing credit card, then releases it incrementally as each installment payment is made. Terms range from 3 to 24 months.

How Is Splitit Similar to Affirm?

Both offer installment-based checkout financing with interest-free options. Both target online retail shoppers who want to split purchases rather than pay upfront.

How Is Splitit Different from Affirm?

No new credit account is opened. No application, no approval process. Splitit works purely on available credit card balance. Your card continues to earn rewards during the repayment period.

In 2025, Splitit partnered with Samsung Wallet to power installment payments across 21 US states, which shows its move into mobile wallet financing.

Who Is Splitit Best For?

Shoppers who already have a credit card with available balance and want to split payments without opening a new credit line or going through an approval process.

Key Features of Splitit

- No credit check: Uses existing card balance only

- Terms: 3 to 24 months

- Reward points: Earned as usual on linked credit card

- Integrations: Shopify, WooCommerce, Magento, BigCommerce, Wix

Pricing

- Free plan: No consumer fees if credit card terms are met

- Paid plans: Merchant pricing on custom quote basis

- Free trial: N/A

Perpay

Perpay is a fintech lending platform built around payroll-linked payments, letting users shop and build credit simultaneously through automatic paycheck deductions.

Available on iOS and Android. US only. Purchases made through the Perpay marketplace only.

What Does Perpay Do?

Perpay approves users based on income, not credit score. Payments are deducted directly from each paycheck on a weekly, biweekly, or monthly schedule. No interest on purchases.

How Is Perpay Similar to Affirm?

Both offer zero-interest installment payment options with no late fees. Both target users who want to spread purchase costs over several months without traditional credit card debt.

For more alternatives in this category, the apps similar to Perpay follow a comparable paycheck-linked model.

How Is Perpay Different from Affirm?

Affirm works at 245,000+ merchant checkouts. Perpay is limited to its own marketplace (electronics, furniture, home goods). That’s a big limitation, but the payroll-deduction model means near-zero missed payments.

Perpay+ (optional add-on) reports payment history to credit bureaus after $200+ in on-time transactions within 4 months.

Who Is Perpay Best For?

Workers with steady employment income who want to buy consumer goods and build credit at the same time, without credit card dependency.

Key Features of Perpay

- Approval basis: Income verification, not credit score

- Payment method: Automatic paycheck deductions

- Terms: Up to 6 months, no interest

- Credit building: Optional via Perpay+ after qualifying activity

Pricing

- Free plan: Yes, no interest or late fees

- Paid plans: Perpay+ for credit reporting (optional add-on)

- Free trial: N/A

Zebit

Zebit is a consumer lending technology platform that offers interest-free financing to shoppers with limited or damaged credit, through its own closed marketplace.

Available on iOS and Android. US only.

What Does Zebit Do?

Zebit gives approved users a credit line to shop its marketplace (electronics, home goods, fashion) and pay over up to 6 months, with no interest and no hard credit check.

How Is Zebit Similar to Affirm?

- Both offer interest-free installment financing

- Both use soft credit checks during the application process

- Both target users who want to avoid traditional credit card debt

How Is Zebit Different from Affirm?

Zebit doesn’t report payment history to credit bureaus, so it won’t help build credit. Products on Zebit can be priced higher than identical items found elsewhere. No returns or refunds on unwanted items.

Affirm works across 245,000+ external merchants. Zebit is a closed ecosystem with no outside retailer access.

Who Is Zebit Best For?

Shoppers with limited credit options who need immediate purchasing access and are comfortable shopping within Zebit’s own product catalog.

Key Features of Zebit

- Credit line: Based on income verification

- Repayment: Up to 6 months, 0% interest

- No hard credit check during application

- Product range: Electronics, home goods, fashion

Pricing

- Free plan: Yes, no interest or hidden fees

- Paid plans: N/A

- Free trial: N/A

Uplift

Uplift is a travel-focused BNPL app that lets users finance flights, hotels, cruises, and vacation packages through monthly installment loans with low APRs.

Available on iOS and Android. Operates in the US and Canada.

What Does Uplift Do?

Uplift integrates directly with travel booking platforms, letting shoppers apply for financing at checkout and pay over monthly installments. According to Fliggy, BNPL travel bookings rose over 20% in 2024 year-over-year, showing this is a real and growing category.

How Is Uplift Similar to Affirm?

Both offer monthly installment financing at merchant checkouts, both use soft credit checks for initial approval, and both offer transparent terms without hidden fees.

How Is Uplift Different from Affirm?

Uplift’s merchant fees run 2 to 4%, lower than most BNPL competitors. It works with partners like Air Canada, American Airlines, AeroMexico, and Atlantis Resorts. Affirm covers general retail; Uplift focuses almost entirely on high-ticket travel purchases.

Who Is Uplift Best For?

Travelers booking flights, hotels, or vacation packages who want monthly payment flexibility without putting the full cost on a credit card upfront.

Key Features of Uplift

- Industry focus: Airlines, hotels, cruises, travel agencies

- Partners: Air Canada, American Airlines, AeroMexico, Atlantis

- Merchant fee: 2 to 4% per transaction

- Terms: Monthly installments, length varies by purchase

Pricing

- Free plan: No interest plans available for qualified users

- Paid plans: Interest applies on some plans (rate varies by credit)

- Free trial: N/A

FuturePay

FuturePay is a revolving credit alternative app that gives online shoppers a reusable digital credit line (called MyTab) for repeat purchases across partner merchants.

Available via web and mobile browser. US only.

What Does FuturePay Do?

FuturePay assigns users a revolving MyTab credit line. Shoppers add purchases to their tab and pay off the balance monthly, similar to a credit card but without the card itself.

How Is FuturePay Similar to Affirm?

Both provide checkout financing tools for online shoppers and both aim to replace traditional credit card use at the point of sale. Both offer flexible repayment on purchases made through partner merchants.

How Is FuturePay Different from Affirm?

Affirm creates a new loan for each purchase. FuturePay uses a revolving tab model, so repeat shoppers don’t re-apply every time. The tradeoff is a smaller merchant network compared to Affirm’s 245,000+ partners.

FuturePay is best suited for repeat shoppers at specific stores, not one-off large purchases.

Who Is FuturePay Best For?

Regular online shoppers at FuturePay’s partner merchants who want a reusable credit line without opening a traditional credit card account.

Key Features of FuturePay

- Credit model: Revolving MyTab (not per-purchase loans)

- Reusable: No new application per purchase

- Payment: Monthly balance payoff

- Platform: Web and mobile browser, no dedicated app

Pricing

- Free plan: No interest on paid-in-full monthly balances

- Paid plans: Interest applies to carried balances

- Free trial: N/A

What Is Affirm and How Does It Work?

Affirm is a point-of-sale lending platform founded in 2012 in San Francisco. It lets shoppers split purchases at checkout into smaller payments, without charging late fees or hidden costs.

It operates across 245,000+ merchant partners, including Amazon, Walmart, Target, Best Buy, and Shopify stores.

| Plan | Term | Interest | Credit Check |

| Pay in 4 | 6 weeks (biweekly) | 0% | Soft only |

| Pay in 30 | 30 days | 0% | Soft only |

| Pay Monthly | 3 to 60 months | 0% to 36% APR | Soft or hard |

Affirm charges merchants a transaction fee of roughly 4 to 6% per sale. That fee is how Affirm subsidizes the 0% APR plans offered to consumers.

In Affirm’s fiscal Q1 2025, total revenue grew 41% year-over-year to $698 million, with merchant network revenue up 29% (Affirm SEC filing).

As of April 2025, Affirm reports all BNPL loans to Experian. It also reports to Equifax and TransUnion, making it the only major BNPL provider to report across all three bureaus.

That credit reporting piece matters more than it used to. FICO launched its new BNPL-specific scoring models, FICO Score 10 BNPL and FICO Score 10T BNPL, in fall 2025, trained on data from 500,000 Affirm users (FICO, 2025).

How Do Buy Now Pay Later Apps Make Money?

Most people assume BNPL is free. It isn’t, just not in an obvious way.

BNPL companies primarily earn through merchant transaction fees, not consumer charges. Merchants pay to offer installment options at checkout because it drives higher order values and conversion rates.

BNPL delivers an 85% higher average order value than other payment methods, and up to 40% of BNPL sales come from first-time customers to the retailer (Capital One Shopping, 2026).

Where the revenue actually comes from

Merchant fees: 2% to 8% per transaction, depending on the platform and loan term.

Consumer interest: Applies only on longer-term monthly plans. Pay-in-4 is typically free of consumer-side interest.

Late fees: Declining across the industry. The CFPB found that in 2023, only 4.1% of BNPL loans were assessed a late fee, down from 5.2% in 2022.

Loan sales: Affirm sells a portion of originated loans to third-party investors, earning additional revenue from the spread between sale proceeds and loan carrying value.

Convenience fees: Some platforms (like Zip) charge consumers a flat $4 to $6 per order instead of merchant fees. That’s an explicit cost shift to the buyer.

The 0% APR plans consumers see at checkout are subsidized by the merchant, not offered out of goodwill. Peloton, for example, pays Affirm a higher merchant fee to offer zero-interest financing as a sales tool.

How fee structures compare by platform

| Platform | Merchant Fee | Consumer Late Fee | Convenience Fee |

| Affirm | 4% to 6% | None | None |

| Klarna | Varies | Up to $7 | None |

| Afterpay | 4% to 6% + $0.30 | Up to $68 | None |

| Zip | Varies | Varies | $4 to $6 per order |

| Sezzle | ~6% + $0.30 | $0 to $5.99 | None |

What Is the Difference Between Pay-in-4 and Monthly Installment Plans?

These are two structurally different products that happen to live under the same “BNPL” label. Mixing them up is where most shoppers get burned.

Pay-in-4 is a short-term, always-interest-free structure. Monthly installment loans are closer to personal loans, with potential APR attached.

| Feature | Pay-in-4 | Monthly Installments |

| Term | 6 weeks | 3 to 60 months |

| Interest | Always 0% | 0% to 36% APR |

| First Payment | Due at checkout | Due at checkout or deferred |

| Credit Check | Soft inquiry only | Soft or hard (Varies by platform) |

| Best For | Purchases under $500 | Purchases over $500 (Electronics, furniture, travel) |

The average BNPL loan is just $135, according to CFPB data, which reflects how heavily the pay-in-4 structure dominates actual usage.

Monthly plans make more sense for high-ticket categories. Electronics, home appliances, and travel packages routinely exceed $500, where 6-week repayment is impractical.

Which BNPL Apps Offer Long-Term Monthly Financing?

Klarna: Up to 24 months. Requires a soft credit check; hard inquiry possible for longer terms.

Sezzle: 3 to 48 months. Up to $15,000 per purchase. Interest ranges from 0% to 34.99% based on credit profile.

Affirm: 3 to 60 months. The widest term range in the consumer BNPL space. APR from 0% to 36%.

Uplift: Monthly plans specifically for travel, flights, hotels, and cruises. Works with Air Canada and American Airlines, among others.

PayPal Pay Monthly covers $200 to $10,000, with terms up to 24 months. That limit stops short of Affirm’s 60-month ceiling, which handles purchases up to several thousand dollars for furniture or home improvement.

Does Using Buy Now Pay Later Apps Affect Your Credit Score?

Until 2025, the honest answer was: mostly no. That’s changing.

53.6 million consumers, roughly one in five US adults, used a BNPL loan in 2023, a 12% increase from 2022 (CFPB, December 2025). Most of those loans left no trace on any credit report.

FICO launched its BNPL-specific scoring models, FICO Score 10 BNPL and FICO Score 10T BNPL, in fall 2025. Those scores are now available to lenders alongside traditional FICO scores.

Soft vs. hard credit checks across platforms

Most BNPL apps use soft inquiries only. A soft check lets the platform assess your creditworthiness without it appearing on your report or affecting your score.

- Soft check only: Klarna, Afterpay, Sezzle, Zip, PayPal Pay in 4

- Soft check (Pay in 4) / potential hard check (monthly plans): Affirm, Klarna long-term

- No credit check at all: Splitit (uses existing card balance), Zebit (income-based only)

Affirm’s hard inquiry policy applies specifically to longer-term monthly plans. The six-week Pay in 4 product uses a soft check only.

Which platforms report to credit bureaus?

Reports positive history (all three bureaus): Affirm, as of April 2025. This is the only major BNPL provider with full bureau coverage.

Reports positive history (opt-in, one bureau): Sezzle Up ($3/month subscription, reports to one bureau).

Reports positive history (income-linked deductions): Perpay, after qualifying on-time payments of $200+ within 4 months.

Does not report positive history: Afterpay, PayPal Pay in 4, Zebit, Zip, Klarna Pay in 4.

Nearly 24% of BNPL users made a late payment in 2024, up from 18% in 2023 (Federal Reserve). Under the new FICO models, those late payments now have direct scoring consequences.

The CFPB found that about 63% of BNPL borrowers had multiple BNPL loans outstanding at the same time in 2023. Each of those loans now carries scoring exposure under the new model.

How Do You Choose the Right App Like Affirm for Your Situation?

The right BNPL app depends on three things: what you’re buying, your credit profile, and whether you want the purchase to build credit history.

Most shoppers default to whichever platform appears at checkout. That’s usually fine for small purchases. For anything over $300, it’s worth a 60-second comparison.

| Use Case | Best App | Key Reason |

| Broad retail (wide merchant access) | Klarna | 800,000+ merchants globally |

| Small fashion or beauty purchases | Afterpay | Starts at $35, simple Pay in 4 |

| Travel booking | Uplift | Built for airlines, hotels, cruises |

| Already have a credit card | Split | No new credit line, earns card rewards |

| Building credit | Affirm or Sezzle Up | Bureau reporting included or opt-in |

| No credit history | Perpay or Zebit | Income-based approval, no credit check |

BNPL purchases resulted in an 85% higher average order value compared to other payment methods (Capital One Shopping). That statistic explains why so many retailers push BNPL at checkout. It’s worth being aware of that pressure when deciding whether to split a purchase.

Which App Like Affirm Is Best for Building Credit?

Affirm is currently the strongest option. It reports to all three bureaus as of April 2025, meaning on-time payments build a documented history with Equifax, Experian, and TransUnion simultaneously.

FICO’s joint study with Affirm found that consumers with five or more Affirm loans typically saw higher scores or no score changes under the new BNPL scoring model, provided payments were on time (FICO, 2025).

Sezzle Up ($3/month) is a lower-cost entry point for credit building, though it reports to one bureau only. Perpay requires on-time transactions exceeding $200 within four months before reporting kicks in, and purchases are limited to its own marketplace.

Which App Like Affirm Works With No Credit Check?

Three solid options here, each with a different limitation to weigh.

- Splitit: Uses your existing credit card balance. No new account, no approval process, no inquiry at all. Works only if you have available credit on a card.

- Zebit: Income verification instead of credit check. Closed marketplace only, no external retailer access.

- Perpay: Income and payroll-linked. Approves based on employment, not credit score. Limited to Perpay’s own product catalog.

Afterpay and Sezzle both use soft credit checks, so they don’t affect your score, but they aren’t fully check-free. If zero credit involvement is the goal, Splitit or Zebit are the cleaner options.

One thing the CFPB flagged: 33% of BNPL borrowers were borrowing from multiple providers at once in 2023. Managing several open installment schedules across different apps makes missed payments significantly more likely. Limit active BNPL loans to one or two at a time.

Checking out fintech apps that sit alongside BNPL, like cash advance tools or earned wage access platforms, can also fill gaps that buy now pay later services don’t cover, especially for irregular income or emergency expenses.

FAQ on Apps Like Affirm

What are the best apps like Affirm?

The top buy now, pay later alternatives are Klarna, Afterpay, Sezzle, Zip, PayPal Pay Later, Splitit, Perpay, Zebit, Uplift, and FuturePay. Each targets a different use case, from broad retail to travel financing to credit building.

Which app like Affirm has no credit check?

Splitit requires no credit check at all. It uses your existing credit card balance. Zebit and Perpay skip credit checks too, approving users based on income verification instead. All three work without a hard inquiry.

Do apps like Affirm affect your credit score?

Most use soft credit checks that don’t impact your score. However, since fall 2025, FICO now includes BNPL data in new scoring models. Missed payments on any platform can damage your credit if sent to collections.

Which BNPL app is best for building credit?

Affirm reports to all three bureaus: Equifax, Experian, and TransUnion. Sezzle Up offers credit reporting for $3 per month. Perpay reports after qualifying on-time payments. These are the strongest options for building a credit history.

What is the difference between Affirm and Klarna?

Klarna has a larger merchant network (800,000+) and offers a “Pay in 30 Days” option Affirm doesn’t. Affirm supports longer loan terms, up to 60 months. Klarna’s late fees are capped at $7; Affirm charges none at all.

Are there apps like Affirm for bad credit?

Yes. Zip is rated best for bad credit by CNBC Select. Perpay and Zebit approve based on income, not credit score. Sezzle also has a high approval rate for users with limited credit history.

What app splits purchases into 4 payments like Affirm?

Klarna, Afterpay, Sezzle, Zip, and PayPal Pay in 4 all offer the same pay-in-4 installment structure. Each splits the total into four equal payments due every two weeks, with the first payment collected at checkout.

Which BNPL app works for travel purchases?

Uplift is built specifically for travel. It works with airlines like Air Canada and American Airlines, plus hotel and cruise partners. PayPal Pay Later and Affirm’s monthly plans also cover travel, but Uplift is the dedicated option.

Is there an app like Affirm that works anywhere?

Zip comes closest. It generates a virtual Visa card usable at any retailer that accepts Visa, even stores without native BNPL integration. Klarna’s physical card works similarly across its global merchant network.

What app like Affirm is best for online shopping?

PayPal Pay in 4 is rated best for online shopping by CNBC Select. It works anywhere PayPal is accepted, requires no new app, charges zero interest and zero late fees on Pay in 4 plans.

Conclusion

This conclusion is for an article presenting the strongest installment payment options available as Affirm alternatives in 2025.

No single platform wins across every category. Klarna suits frequent online shoppers. Splitit works best if you already carry a credit card with available balance. Uplift is the go-to for travel financing.

Credit impact is no longer a minor consideration. With FICO’s new BNPL scoring models now live, choosing a platform that reports to credit bureaus, like Affirm or Sezzle Up, carries real long-term weight.

Watch for convenience fees, closed marketplaces, and late fee structures before committing. The best deferred payment platform is the one that fits your purchase size, credit goals, and repayment schedule without surprises.

- How to Rename a Repository in GitHub: Quick Guide - July 28, 2026

- What Modern Teams Should Know Before Replacing Legacy PAM Tools - July 27, 2026

- How to Redeem a Google Play Gift Card - July 26, 2026