A bill comes due before your next paycheck. It happens to more people than you’d think.

Apps like Deferit solve this by letting you pay bills in installments, interest-free, without touching a credit card. But Deferit isn’t the only option, and for many users it isn’t the cheapest one either.

The buy now pay later space now includes dozens of platforms covering everything from utility bills to retail purchases. Some skip credit checks entirely. Others build your credit history while you pay.

This guide covers the 10 best alternatives, breaking down fees, credit reporting, bill coverage, and platform availability so you can match the right app to your actual situation.

Apps Like Deferit

Deferit lets you upload a bill, pay it in 4 interest-free installments, and avoid late fees. It charges $14.99/month plus a $0.99 processing fee per payment. The apps below cover the same core need, with different fee models, bill coverage, and platform support.

The global BNPL market hit $25.71 billion in 2024 and is projected to reach $90.15 billion by 2032, according to SNS Insider.

| App | Best For | Key Difference | Platforms |

| Zip | Household bills + retail | Per-transaction fee, no monthly sub | iOS, Android |

| WillowPays | No-credit-check bill pay | No credit check at all | Web-based |

| Affirm | Large purchases, long-term | Up to 60-month plans, 0%-36% APR | iOS, Android |

| Klarna | Shopping + bill flexibility | Pay in 30 days option + rewards | iOS, Android |

| Afterpay | Retail purchases | No interest, $10 late fee cap | iOS, Android |

| Sezzle | Credit-building shoppers | Reports to credit bureaus | iOS, Android |

| Split | Existing credit card users | Uses your existing card, no new credit line | iOS, Android |

| PayPal Pay Later | PayPal users | Tied to existing PayPal account | iOS, Android, Web |

| Gerald | Zero-fee BNPL + cash advance | No fees at all; unlocks cash advance | iOS, Android |

| Laybuy | 6-week payment flexibility | 6 weekly installments vs. 4 | iOS, Android |

Zip

Zip is a BNPL and deferred payment service that splits bills and purchases into 4 or 8 installments for users who need flexible bill payment across iOS and Android. It charges a per-transaction origination fee instead of a monthly membership, and supports both online and in-store purchases.

What Does Zip Do?

Zip lets users split purchases and household bills into 4 or 8 payments via its mobile app, virtual Visa card, or browser checkout, with payments auto-billed every two weeks.

How Is Zip Similar to Deferit?

- Both split bills into installments with no full payment upfront

- Both support utility and household bill payments

- Both available on iOS and Android

How Is Zip Different from Deferit?

No monthly fee: Zip charges an origination fee per transaction ($0 to $7.50 for Pay in 4), not a $14.99/month subscription. That makes it cheaper for occasional use.

Wider purchase scope: Zip works for retail, groceries, and in-store purchases. Deferit focuses specifically on service bills. Also, Zip does a soft credit pull at signup; Deferit does not always require one.

Who Is Zip Best For?

Zip suits users who only need occasional bill help and want to avoid a recurring monthly fee. Good fit for those who want one app for both bills and retail shopping.

Key Features of Zip

- Pay in 4: 4 equal payments every 2 weeks, origination fee $0-$7.50

- Pay in 8: 8 payments every 2 weeks, origination fee $0-$124

- Virtual Visa card: Works in-store and online anywhere Visa is accepted

- Free reschedule: 1 free payment reschedule per calendar month

- Bill pay via BPAY: Flat $2.50 processing fee per bill (AU market)

Pricing

- Free plan: Yes, no subscription fee

- Per-transaction fee: $0 to $7.50 (Pay in 4) or $0 to $124 (Pay in 8)

- Late fee: Up to $7 per missed payment

- Free trial: No

WillowPays

WillowPays is a bill-specific deferred payment service that pays your provider upfront and splits repayment into 4 weekly installments for users with no credit history or poor credit scores. It runs no credit check whatsoever, and approval is based entirely on the bill details.

What Does WillowPays Do?

WillowPays lets users upload a bill, get approved within 1 business day, and have Willow pay the provider directly within 1-3 business days. The user repays in 4 weekly installments with zero interest.

How Is WillowPays Similar to Deferit?

The model is nearly identical: upload a bill, the service pays it, you repay over time. Both charge a flat service fee, not interest. Both cover utility bills, insurance, car payments, and subscriptions.

How Is WillowPays Different from Deferit?

No credit check at all: Deferit considers your payment history and account standing. Willow skips credit checks entirely. That opens access to more users.

No credit bureau reporting: Willow does not report on-time payments to credit bureaus. Deferit started reporting payments in September 2024, which helps users build credit over time.

Who Is WillowPays Best For?

WillowPays suits users with no credit history or low scores who need a utility or household bill covered quickly, and don’t need credit-building benefits.

Key Features of WillowPays

- No credit check: Approval based on bill, not credit history

- Flat fee structure: $6 for bills up to $100, $12 up to $200, $18 up to $300

- Starting limit: $250 for new users, increases with usage

- Approval timeline: Under 1 business day

Pricing

- Free plan: No subscription, flat service fee only

- Service fee: $6 per $100 of bill value (tiered)

- Interest: None

- Free trial: No

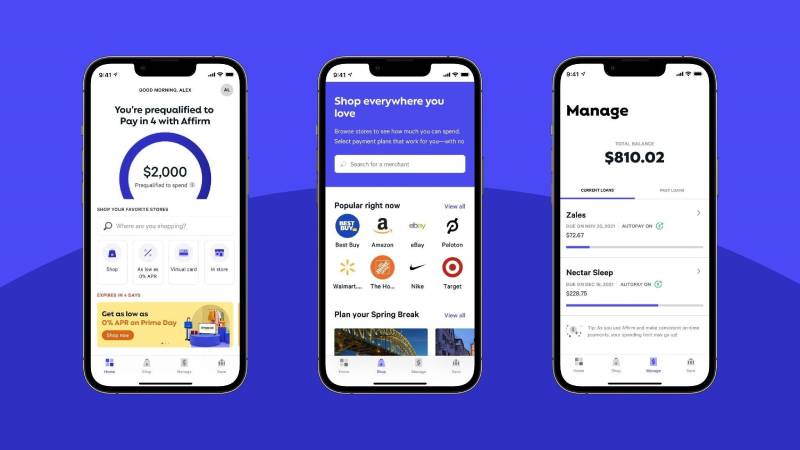

Affirm

Affirm is a BNPL and personal finance app that offers installment plans from 4 payments to 60 months for users who need flexible, longer-term payment structures beyond what bill-splitting apps offer. It reports to credit bureaus and charges no late fees.

What Does Affirm Do?

Affirm lets users split purchases at checkout into interest-free Pay in 4 plans or longer monthly plans up to 60 months, with APRs ranging from 0% to 36% depending on creditworthiness.

How Is Affirm Similar to Deferit?

Both offer a Pay in 4 interest-free option. Both help users manage cash flow by splitting large payments. Affirm also reports to credit bureaus, matching Deferit’s credit-building benefit introduced in late 2024.

How Is Affirm Different from Deferit?

Not designed for utility bills: Affirm works through merchant checkouts, not by uploading a bill photo. You can’t use it to pay your electricity or water bill directly.

Much wider loan range: Affirm finances up to $20,000 with terms up to 5 years. Deferit focuses on smaller household bills with a monthly credit limit. Affirm charges no late fees; Deferit’s consequences depend on account standing.

Who Is Affirm Best For?

Affirm suits users making larger one-time purchases (electronics, furniture, medical) who want transparent financing terms and don’t need direct bill upload functionality. If you’re also looking for apps similar to Affirm, there are solid options worth comparing.

Key Features of Affirm

- Pay in 4: 0% APR, no fees

- Monthly plans: 3 to 60 months, 0%-36% APR

- Affirm Card: Virtual Visa for in-store and online use

- No late fees: Ever, on any plan

- Credit reporting: Reports to credit bureaus

Pricing

- Free plan: Yes, Pay in 4 is free

- Monthly plans: 0%-36% APR based on credit

- Late fee: None

- Free trial: No

Klarna

Klarna is a flexible payment app that offers Pay in 4, Pay in 30 days, and monthly financing up to 36 months for shoppers who want broader payment options beyond bill splitting. It operates in 45+ countries and has over 90 million users globally.

What Does Klarna Do?

Klarna lets users split purchases at partner retailers into installments or defer payment for 30 days. The app also includes a shopping browser, price tracking, and up to 10% cashback at select retailers.

How Is Klarna Similar to Deferit?

Both offer a Pay in 4 interest-free structure. Both help users avoid upfront full payments and manage short-term cash flow gaps. Klarna’s Pay in 30 days option also functions as a bill deferral tool for eligible purchases.

How Is Klarna Different from Deferit?

Retail-focused: Klarna is built for merchant checkout, not household bill management. You can’t upload a utility bill to Klarna and have it paid like you can with Deferit.

Klarna also adds a full shopping ecosystem on top of payments. Deferit is purpose-built for bill deferral. Klarna charges late fees (amount varies by region); Deferit’s model is membership-based with set installments.

Who Is Klarna Best For?

Klarna suits regular online shoppers who want flexible checkout financing, cashback rewards, and price-tracking features, and don’t primarily need to manage utility or service bills.

Key Features of Klarna

- Pay in 4: 4 interest-free payments over 6 weeks

- Pay in 30: Full payment deferred 30 days, no interest

- Monthly financing: Up to 36 months, may charge interest

- Cashback: Up to 10% at select retailers

- Global reach: Available in 45+ countries

Pricing

- Free plan: Yes, Pay in 4 and Pay in 30 are free when paid on time

- Monthly financing: Up to 29.9% APR

- Late fee: Yes, varies by region

- Free trial: No

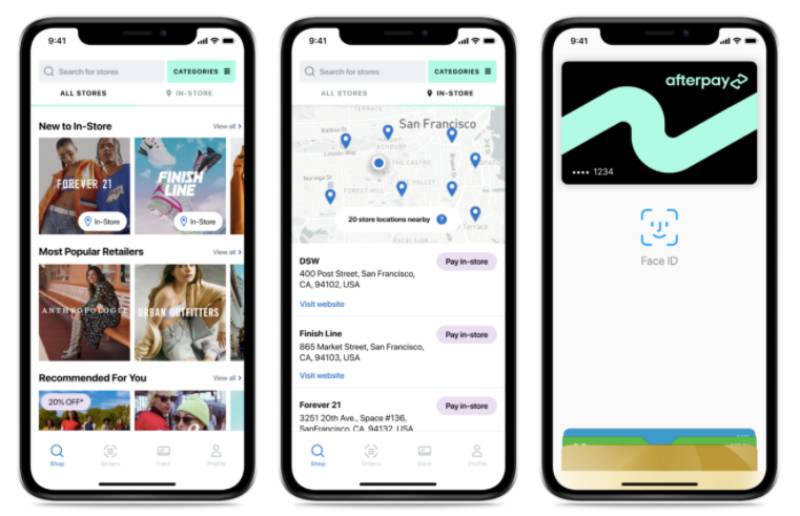

Afterpay

Afterpay is a retail-focused BNPL app that splits purchases into 4 interest-free payments over 6 weeks for online shoppers who want a simple, predictable payment schedule. It does not charge interest but applies a $10 late fee, capped at 25% of the order value.

What Does Afterpay Do?

Afterpay divides any approved purchase into 4 equal fortnightly payments. The first payment is due at checkout. No interest is ever charged on the Pay in 4 structure.

How Is Afterpay Similar to Deferit?

Same 4-payment structure. Both are interest-free for users who pay on time. Both help users split large expenses and avoid depleting their full account balance in one transaction.

How Is Afterpay Different from Deferit?

Retail only: Afterpay does not process utility bills, insurance payments, or household service bills. Deferit was built specifically for those. Afterpay’s $10 late fee is also a notable difference since Deferit’s model is membership-based with set installments and no separate late fee structure.

Merchants offering Afterpay see an average order value increase of 57%, according to Sezzle research, showing it’s firmly positioned as a retail tool.

Who Is Afterpay Best For?

Afterpay suits regular online shoppers who primarily want to split retail purchases like fashion, electronics, or home goods into 4 payments with no interest.

Key Features of Afterpay

- Pay in 4: 4 equal payments, 2 weeks apart, 0% interest

- Late fee: $10 per missed payment, capped at 25% of order value

- Virtual card: Usable in-store and online

- Pulse Rewards: Points for on-time payments

Pricing

- Free plan: Yes, no subscription

- Interest: None

- Late fee: $10, capped at 25% of order

- Free trial: No

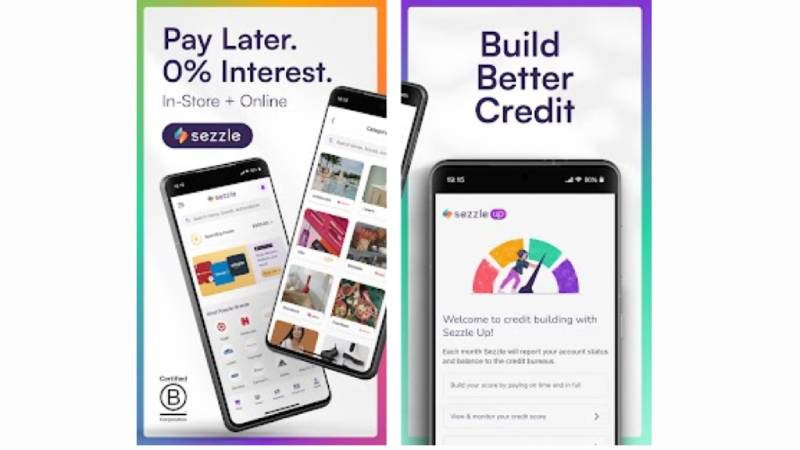

Sezzle

Sezzle is a U.S.-based BNPL app that splits purchases into 4 interest-free payments over 6 weeks and actively helps users build credit through its optional Sezzle Up feature. It recorded 64.1% year-over-year GMV growth in May 2025, according to SNS Insider.

What Does Sezzle Do?

Sezzle lets users split purchases into 4 equal, interest-free installments at partner merchants. It also offers a virtual card for broader use, and Pay in 2 and Pay in 5 options introduced in 2025.

How Is Sezzle Similar to Deferit?

Both offer interest-free installment plans. Both report on-time payments to credit bureaus (Sezzle via opt-in Sezzle Up). Both require no hard credit check for standard purchases.

How Is Sezzle Different from Deferit?

Retail vs. bills: Sezzle is designed for merchant purchases, not direct bill payments. You can’t upload a phone bill or utility invoice to Sezzle.

Sezzle’s monthly interest rates for longer plans run 5.99%-34.99%, while Deferit charges a flat membership fee with no interest. Sezzle also allows 1 free payment reschedule per order, which Deferit doesn’t offer in the same way. For more options in this space, check out our guide to apps like Perpay that combine credit-building with flexible payments.

Who Is Sezzle Best For?

Sezzle suits credit-conscious shoppers who want to build their credit score while splitting retail purchases into manageable installments.

Key Features of Sezzle

- Pay in 4: 4 installments over 6 weeks, 0% interest

- Sezzle Up: Opt-in credit reporting to all 3 bureaus

- Virtual card: Online and in-store use

- Purchase range: $150 to $15,000

- Free reschedule: 1 per order, no fee

Pricing

- Free plan: Yes, Pay in 4 is free

- Monthly plans: 5.99%-34.99% interest

- Late fee: Yes, plus rescheduling and failed payment fees after 1 free reschedule

- Free trial: No

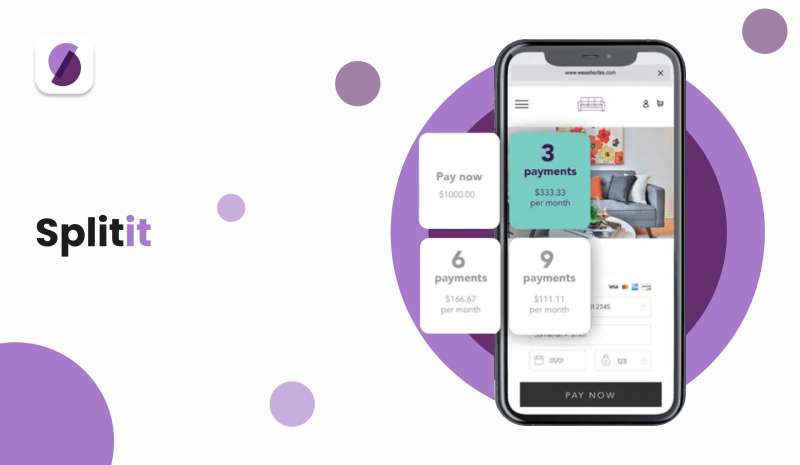

Splitit

Splitit is a unique installment payment tool that uses a shopper’s existing credit card balance to create payment plans, with no new credit application or credit check required. Samsung partnered with Splitit in 2025 to power installments through Samsung Wallet across 21 U.S. states.

What Does Splitit Do?

Splitit pre-authorizes the full purchase amount on the user’s credit card, then charges equal monthly installments until the balance is paid off. Plans run 3 to 24 months with no added interest from Splitit itself.

How Is Splitit Similar to Deferit?

Both give users financial flexibility by spreading payments over time. Both avoid the need for a new loan or hard credit inquiry. Both offer interest-free installment options depending on the plan.

How Is Splitit Different from Deferit?

Requires an existing credit card: Splitit only works if you already have a credit card with available balance. Deferit works with a debit card and bank account. No credit card means no Splitit.

Splitit also doesn’t cover bill uploads. It’s tied to merchant checkouts. Merchant fees run 1.5%-6.5% per transaction plus a flat per-installment charge.

Who Is Splitit Best For?

Splitit suits existing credit card holders who want to break up a large purchase into monthly installments without opening a new line of credit or undergoing an approval process.

Key Features of Splitit

- No new credit line: Uses existing credit card

- No credit check: No application process

- Plan length: 3 to 24 months

- No customer fees: Only subject to your card’s own interest if unpaid

- Approval rate: Over 85%, per Splitit data

Pricing

- Free plan: Yes, no fees charged to consumers

- Interest: None from Splitit; your card may charge if balance isn’t paid

- Free trial: No

PayPal Pay Later

PayPal Pay Later is a BNPL option built into the PayPal ecosystem that lets existing PayPal users split purchases into 4 interest-free payments or access monthly financing up to $10,000. It leverages PayPal’s trusted global payment infrastructure.

What Does PayPal Pay Later Do?

PayPal’s Pay in 4 splits purchases of $30-$1,500 into 4 equal fortnightly payments. Pay Monthly covers purchases up to $10,000 with APRs that may apply depending on terms and creditworthiness.

How Is PayPal Pay Later Similar to Deferit?

Both offer a 4-payment installment structure. Both aim to help users avoid paying the full amount upfront and manage short-term cash flow. PayPal Pay in 4 charges no interest, similar to Deferit’s interest-free model.

How Is PayPal Pay Later Different from Deferit?

No bill upload feature: PayPal Pay Later works at merchant checkout only. You can’t pay a utility bill, car insurance, or phone plan by uploading an invoice.

Merchants pay 4.99% + $0.49 per transaction (as of January 2025). That’s the cost on the merchant side. For consumers, the main drawback is the requirement to already have a PayPal account, unlike Deferit which works as a standalone app.

Who Is PayPal Pay Later Best For?

PayPal Pay Later suits existing PayPal users who frequently shop at PayPal-integrated merchants and want a no-friction BNPL option without setting up a separate account.

Key Features of PayPal Pay Later

- Pay in 4: $30-$1,500 purchases, 0% interest

- Pay Monthly: Up to $10,000 financing, interest may apply

- Purchase protection: Backed by PayPal buyer protection

- No new account needed: Uses existing PayPal login

Pricing

- Free plan: Yes, Pay in 4 is free for consumers

- Monthly financing: Interest may apply; varies by plan

- Late fee: No consumer late fee for Pay in 4

- Free trial: No

Gerald

Gerald is a zero-fee BNPL and cash advance app that lets users buy essentials from its in-app store and access free cash advance transfers with no interest, no late fees, and no subscription costs. It’s backed by Y Combinator and primarily targets users managing household expenses on tight budgets.

What Does Gerald Do?

Gerald lets users make BNPL purchases from its Cornerstore for household essentials, then unlocks a free cash advance transfer to a linked bank account. No fees apply anywhere in the process if the user first meets the minimum BNPL spend threshold.

How Is Gerald Similar to Deferit?

Both target users with tight cash flow and household expense management needs. Both charge zero interest. Both work without requiring a traditional credit check. Both are positioned as a financial buffer between paychecks.

How Is Gerald Different from Deferit?

No direct bill upload: Gerald doesn’t let you upload a utility bill and have it paid like Deferit does. The BNPL is limited to Gerald’s own Cornerstore.

Cash advance unlocking model: Gerald requires you to spend a portion of your advance in the store before you can transfer the rest to your bank. That’s a meaningful constraint. Deferit lets you apply cash directly to specific service bills without this requirement.

Who Is Gerald Best For?

Gerald suits users who need both household essentials purchasing flexibility and occasional small cash advances, and want to avoid all fees. It works well as a cash advance option for Chime users specifically.

Key Features of Gerald

- Zero fees: No interest, no late fees, no subscription, no transfer fees

- BNPL + cash advance: BNPL purchase unlocks free cash advance transfer

- Instant transfers: Available for eligible banks at no cost

- eSIM mobile plans: Pay for T-Mobile-powered plans via BNPL

- Rewards: On-time payment rewards redeemable in Cornerstore

Pricing

- Free plan: Yes, completely free

- Subscription: None

- Interest: None

- Free trial: N/A, always free

Laybuy

Laybuy is a BNPL app that splits purchases into 6 weekly interest-free payments, offering more spread-out repayment than most 4-payment BNPL apps. It originated in New Zealand and has a strong presence in the UK and Australia, now operating under the Klarna brand in some markets.

What Does Laybuy Do?

Laybuy pays merchants immediately on behalf of the customer, then collects 6 equal weekly installments. It supports online and in-store purchases via virtual card, QR code, and Apple/Google Pay integration.

How Is Laybuy Similar to Deferit?

Both pay the provider upfront and let the user repay over time in fixed installments. Both are interest-free. Both are designed to help users avoid lump-sum payments that strain their budget.

How Is Laybuy Different from Deferit?

6 payments vs. 4: Laybuy spreads repayment across 6 weeks instead of Deferit’s 4 payments. That lowers each individual installment amount, which helps for larger purchases.

Retail-focused, not bill-specific: Like most BNPL services, Laybuy operates at merchant checkout. It doesn’t handle direct utility bill uploads. Also, Laybuy is primarily strong in the UK and ANZ markets, not the US.

Who Is Laybuy Best For?

Laybuy suits shoppers in the UK and Australia who want a longer repayment window than standard 4-payment apps and shop at Laybuy-integrated merchants.

Key Features of Laybuy

- 6 weekly payments: Interest-free installments every week

- Boost feature: Pay excess upfront to access higher purchase limits

- Instant merchant payout: Laybuy assumes credit and fraud risk

- In-store support: Virtual card, QR code, Apple/Google Pay

Pricing

- Free plan: Yes, no consumer subscription

- Interest: None

- Late fee: Yes, applies on missed payments

- Free trial: No

What Is Deferit and How Does It Work?

Deferit is a bill budgeting and deferred payment platform that pays your service bills upfront, then lets you repay in 4 interest-free installments over time. Over 550,000 Americans use it, and the platform has processed more than $400 million in bills to date, according to Deferit’s own data.

The core workflow is simple. Upload a photo or file of any bill, Deferit pays the provider directly (by ACH, check, or credit card), and you repay in biweekly installments.

What Deferit covers:

- Utilities: electricity, gas, water, internet

- Phone and TV service bills

- Car payments, insurance premiums, subscriptions

- Rent (in select states)

New members start with a credit limit of $100 to $400. That limit increases with consistent on-time repayments.

Fee structure: $14.99/month membership + $0.99 per payment processing fee. No interest. No late fees.

Starting September 2024, Deferit began reporting every on-time bill payment to all three major credit bureaus: Experian, Equifax, and TransUnion. That single change turned it from a cash flow tool into a credit-building service as well.

The app is iOS-first and available in the U.S. and Australia. Not all states support the Pay in 4 split feature; the credit builder and bill management tools are available nationwide.

How Do Bill Payment Installment Apps Differ from General BNPL Apps?

The BNPL market reached an estimated $70 billion in U.S. transaction volume in 2025, according to the Richmond Federal Reserve. But most of that is retail-only. Only a small category of apps actually handles household bills the way Deferit does.

This distinction matters more than most comparisons show.

| Feature | Bill-Specific Apps | General BNPL Apps |

| Bill upload model | Yes (Deferit, WillowPays) | No |

| Pays provider directly | Yes | No (merchant checkout only) |

| Utility bill coverage | Yes | Usually not |

| Fee model | Flat fee or subscription | Origination fee or late fee |

| Credit check | Soft or none | Soft pull (most) |

Which apps pay bills directly like Deferit does?

Zip supports bill payments via BPAY (Australia) with a flat $2.50 per-bill processing fee. In the U.S., Zip functions as a general BNPL service, not a direct bill-upload platform.

WillowPays is the closest U.S. equivalent. Upload any bill, get approved within one business day, Willow pays the provider within 1-3 days, and you repay in 4 weekly installments.

Both WillowPays and Deferit operate outside standard merchant checkout. That’s what separates them from every other app on this list.

Which BNPL apps can be used for bills indirectly?

Klarna explicitly does not support rent or utility bill payments, per their own product documentation.

Affirm’s virtual card can theoretically be used at billers that accept Visa, but there’s no direct bill-upload workflow. Splitit works through existing credit cards at merchant checkouts only.

The practical gap: if you need to pay an electric bill directly to your utility company, Deferit and WillowPays are the only apps on this list that handle the payment on your behalf without requiring you to find a participating merchant.

Managing cash flow is the top reason people choose BNPL, cited by 36% of users in Numerator’s 2025 survey. For people with irregular income or tight budgets between paychecks, bill-specific apps solve a more immediate problem than retail BNPL does.

What Are the Fee and Cost Differences Between Deferit Alternatives?

Deferit’s $14.99/month adds up to $179.88/year regardless of how many bills you process. That math only works in your favor if you’re splitting multiple bills per month consistently.

| App | Monthly Fee | Per-Transaction | Late Fee |

| Deferit | $14.99 | $0.99/payment | None |

| WillowPays | None | $6 per $100 of bill | None |

| Zip (Pay in 4) | None | $0-$7.50 origination | Up to $7 |

| Affirm | None | 0%-36% APR | None |

| Afterpay | None | None (on time) | $10, capped at 25% |

| Sezzle | None | None (Pay in 4) | Multiple fees possible |

| Splitit | None | None to consumer | None |

| Gerald | None | None | None |

| Klarna | None | None (Pay in 4) | Varies by region |

| Laybuy | None | None | Yes |

For occasional bill help (1-2 bills per month), WillowPays is cheaper. For high-frequency users paying 4+ bills monthly, Deferit’s flat subscription becomes more cost-efficient per transaction.

Gerald has zero fees across every category. The catch: you must first spend part of your advance in Gerald’s in-app Cornerstore before you can transfer remaining funds to your bank account.

Nearly 60% of BNPL users admit to using the service to finance purchases they couldn’t otherwise afford, according to Motley Fool Money’s 2025 report. Fee transparency matters here. A subscription that seems manageable can compound fast if the user’s financial situation is already tight.

Which Apps Like Deferit Help Build Credit?

Most BNPL apps don’t report payments to credit bureaus at all. The CFPB confirmed in its January 2025 report that lenders generally don’t report BNPL pay-in-four transactions to credit reporting agencies. Deferit is an explicit exception to that norm.

Here’s where each app stands on credit reporting:

- Deferit: Reports all on-time payments to Experian, Equifax, and TransUnion (since September 2024)

- Sezzle: Opt-in Sezzle Up feature reports to all 3 bureaus

- Affirm: Reports on monthly installment plans; does not report Pay in 4 transactions

- Zip: Reports to credit bureaus; missed payments can negatively affect score

- WillowPays, Splitit, Gerald, Laybuy, Afterpay, Klarna: Do not report Pay in 4 payments to bureaus

The majority of BNPL users (61%) carry subprime or deep subprime credit scores, per the CFPB’s 2025 research. For that group, credit-reporting installment apps aren’t just convenient. They’re one of the few accessible paths to credit improvement.

If credit building is the primary goal alongside bill management, Deferit and Sezzle are the two apps on this list with the clearest, most consistent reporting structures.

Sezzle’s reporting is opt-in via Sezzle Up. Deferit reports automatically. That difference matters for users who might forget to activate an optional feature.

For users specifically looking for apps similar to Possible Finance that combine installment access with credit building, the overlap with Deferit’s model is worth examining before choosing.

How Do You Choose the Right Deferit Alternative for Your Situation?

The right app depends on two variables: what you’re paying and how often you need help. Most people only need one answer.

| Your Situation | Best Option | Why |

| Pay multiple bills monthly | Deferit | Flat subscription covers all bills |

| Occasional bill help, no credit history | WillowPays | No credit check, flat fee per bill |

| Need retail + bill flexibility | Zip | Dual-purpose, no monthly fee |

| Building credit while splitting payments | Deferit or Sezzle Up | Both report to all 3 bureaus |

| Large purchase, long repayment | Affirm | Up to $20,000, up to 60 months |

| Zero fees, no strings attached | Splitit (credit card holders only) | No fees to consumer at all |

Around 53% of BNPL users are 35 years old or younger, according to Empower’s 2025 data. That demographic tends to have thinner credit files, which makes the credit-reporting distinction between apps more meaningful than for older users with established history.

What should you check before signing up for a bill payment app?

State availability: Deferit’s Pay in 4 feature is not available in all U.S. states. WillowPays and Gerald have their own geographic limitations.

Platform: Deferit is iOS-first. Zip and WillowPays are available via web browsers, which opens Android access. Check your device before committing.

Three other factors worth verifying upfront:

- Does the app accept your specific bill type (some exclude rent, loans, and retail purchases)?

- Does signup require a hard or soft credit pull?

- What is the starting credit or advance limit for new users?

Deferit starts new users at $100-$400. WillowPays starts at $250. Affirm can go up to $20,000. The right starting limit depends entirely on the size of the bill you’re trying to cover.

For users who also want to explore apps like Flex Rent for splitting rent specifically, the feature overlap with Deferit’s rent coverage is worth comparing directly before choosing one platform.

FAQ on Apps Like Deferit

What is the closest app to Deferit for paying bills in installments?

WillowPays is the closest alternative. It uses the same upload-and-split model: you submit a bill, Willow pays the provider, and you repay in 4 weekly installments with zero interest. No credit check required.

Do apps like Deferit check your credit?

Most perform a soft credit pull, which does not affect your score. WillowPays skips credit checks entirely. Deferit itself uses a soft inquiry at signup. Zip and Sezzle also use soft pulls for standard pay in 4 approvals.

Can I use Afterpay or Klarna to pay utility bills?

No. Afterpay and Klarna operate through merchant checkouts only. They do not accept direct bill uploads. For utility bill payment assistance, you need a bill-specific service like Deferit or WillowPays.

Which apps like Deferit help build credit?

Deferit reports on-time payments to all three major bureaus. Sezzle Up offers opt-in credit reporting. Affirm reports on monthly installment plans but not on Pay in 4 transactions. Most BNPL apps do not report at all.

Are there free alternatives to Deferit with no monthly fee?

Yes. Zip, Afterpay, Klarna, and Sezzle charge no monthly subscription. Gerald is completely fee-free. WillowPays charges a flat per-bill service fee instead of a recurring membership, making it cheaper for occasional bill help.

What bills can Deferit alternatives pay?

Deferit covers utilities, phone, internet, insurance, car payments, and subscriptions. WillowPays covers similar categories. General BNPL apps like Klarna and Affirm are limited to retail merchant purchases and cannot pay service providers directly.

Which app like Deferit works on Android?

Deferit is iOS-first. Zip, Afterpay, Klarna, Sezzle, Affirm, and Gerald are all available on both iOS and Android. WillowPays operates through a web browser, which makes it accessible on any device including Android.

How does Splitit differ from Deferit?

Splitit uses your existing credit card to create installment plans, with no new credit line or loan. Deferit pays bills directly to providers. Splitit works at merchant checkouts only and requires an active credit card with available balance.

What is the best no-interest bill payment app?

Deferit and WillowPays both offer interest-free installments specifically for household bills. For retail purchases, Afterpay, Klarna Pay in 4, and Sezzle are interest-free when paid on time. Gerald charges no interest on any transaction.

Can apps like Deferit help with short-term financial hardship?

Yes. These deferred payment services are designed for income gaps and unexpected expenses. Deferit has saved users over $39 million in late fees. Gerald also offers a small cash advance after a qualifying BNPL purchase.

Conclusion

This conclusion is for an article presenting apps like Deferit, a category that has grown well beyond simple bill deferral into a broader set of flexible bill payment and cash flow tools.

No single app wins for every situation. WillowPays works best for no-credit-check bill coverage. Sezzle and Affirm serve shoppers who want deferred payment with credit-building potential. Splitit suits existing credit card holders who want zero added fees.

The right choice comes down to three things: what you’re paying, how often, and whether credit reporting matters to you.

Deferit’s combination of household bill management, interest-free installment plans, and bureau reporting is still hard to match in one app. But the alternatives above close that gap depending on your specific financial needs.

- Android App Bundle vs APK - August 1, 2026

- PHP Cheat Sheet - July 31, 2026

- How Computer Vision, built on existing systems, increases inventory accuracy by 20%+ and protects profit margins - July 31, 2026