Sezzle works well, but it is not always the best fit for every shopper or every purchase.

The buy now pay later space has expanded fast. You now have dozens of apps offering interest-free installments, flexible payment schedules, and instant approval with no hard credit check, each with different merchant networks, spending limits, and fee structures.

Some handle large purchases better. Others are built for credit building, in-store use, or shoppers with no credit history at all.

This guide covers the best apps like Sezzle available right now, with a direct breakdown of how each one works, what it costs, and who it actually suits. By the end, you will know exactly which BNPL alternative fits your situation, whether you need zero fees, a higher spending limit, or a platform that reports to credit bureaus.

Apps Like Sezzle

The global BNPL market is projected to grow from $42.22 billion in 2025 to $147.27 billion by 2031, a 23% CAGR (ResearchAndMarkets). That growth is driving real competition, and Sezzle is no longer the only solid option.

Whether you need a bigger merchant network, longer payment terms, or no credit check at all, there are solid alternatives worth knowing.

Klarna

Klarna is a fintech app that lets shoppers split purchases into installments, pay in 30 days, or finance over 6 to 24 months. It targets online shoppers who want flexible, interest-free payment plans with built-in shopping perks.

What Does Klarna Do?

Klarna lets users pay in 4 interest-free installments, defer a full payment up to 30 days, or finance purchases monthly across iOS and Android.

How Is Klarna Similar to Sezzle?

- Both offer a pay-in-4 interest-free model with soft credit checks

- Both target online shoppers looking to avoid credit card interest

- Both support deferred payment options at checkout

How Is Klarna Different from Sezzle?

Klarna operates in 45+ countries, while Sezzle is primarily US-focused. Klarna’s app includes price alerts, wishlists, and a one-time virtual card for non-partner stores. Sezzle does not offer these shopping features.

Klarna’s merchant network exceeds 800,000 retailers globally. Sezzle has around 41,800 active merchants.

Who Is Klarna Best For?

Klarna suits shoppers who want a broad merchant network, built-in deal-finding tools, and flexible payment terms beyond the standard 6-week pay-in-4 window.

Key Features of Klarna

- Pay in 4: 4 interest-free biweekly payments, no fees if on time

- Pay in 30 days: Full deferred payment, no interest

- Monthly financing: Up to 24 months, 0%–35.99% APR

- One-time virtual card: Shop at any online retailer, not just Klarna partners

- In-app shopping: Price alerts, wishlists, cashback at select merchants

Pricing

- Free plan: Yes, no subscription required

- Paid plans: N/A for consumers; interest applies on monthly financing (up to 35.99% APR)

- Late fee: Up to $7, capped at 25% of order value

- Free trial: N/A

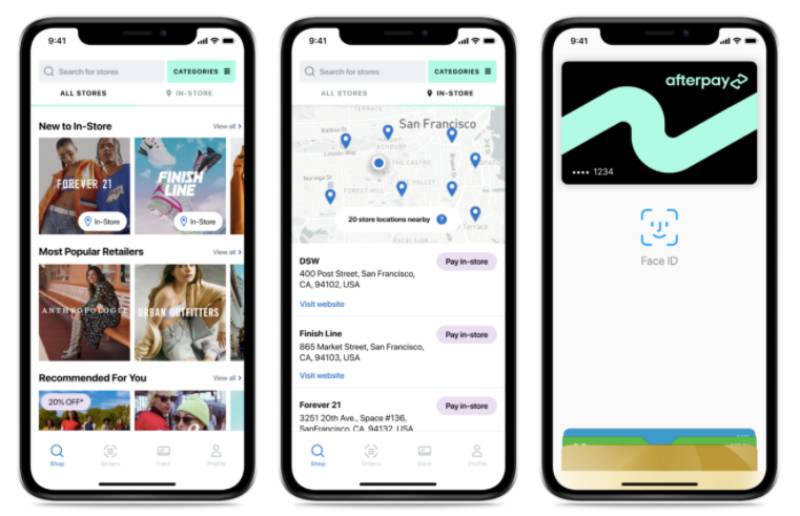

Afterpay

Afterpay is a buy now pay later app that splits purchases into 4 interest-free installments over 6 weeks. It targets fashion, lifestyle, and everyday retail shoppers, particularly Millennials and Gen Z.

What Does Afterpay Do?

Afterpay splits any eligible purchase into 4 equal payments, charged every two weeks, with no interest on short-term plans across iOS and Android.

How Is Afterpay Similar to Sezzle?

- Same pay-in-4 model with biweekly installments

- Both run soft credit checks only

- Both work online and in-store at participating retailers

How Is Afterpay Different from Sezzle?

Afterpay is now part of Block, Inc. (formerly Square), giving it deeper retail integrations. It also offers longer monthly plans (3, 6, 12, or 24 months) up to $20,000, while Sezzle caps standard pay-in-4 at a lower limit.

Afterpay charges a $10 late fee per missed payment, capped at 25% of order value. Sezzle allows one free reschedule per order before fees apply.

Who Is Afterpay Best For?

Afterpay suits fashion and lifestyle shoppers who want a simple pay-in-4 setup with no application process and access to a large network of brand-name retailers.

Key Features of Afterpay

- Pay in 4: Interest-free, 6-week repayment window

- Monthly plans: 3–24 months for larger purchases up to $20,000

- Spending limit: Starts ~$600, grows with payment history

- In-store support: Works via Afterpay card at physical retailers

Pricing

- Free plan: Yes

- Late fee: $10 per missed payment, capped at 25% of order value

- Monthly plan interest: Variable, standard rates apply

- Free trial: N/A

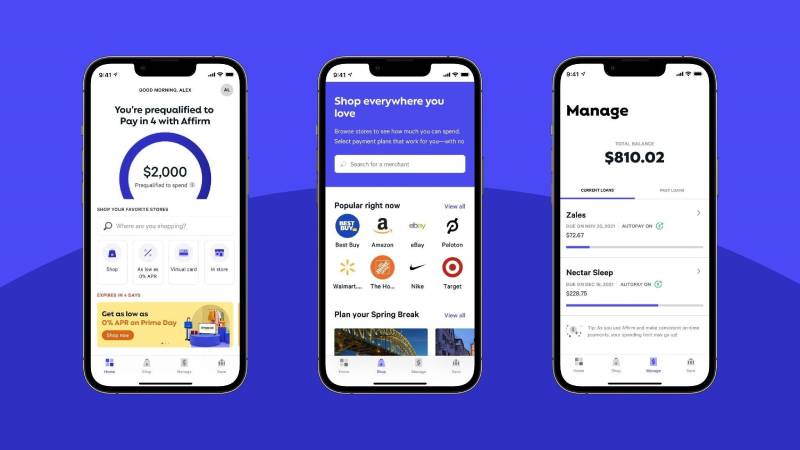

Affirm

Affirm is a point-of-sale financing app that offers pay-in-4 plans and long-term monthly installments from 3 to 60 months. It targets shoppers making mid-to-large purchases who want transparent pricing upfront.

What Does Affirm Do?

Affirm lets users split purchases into short-term interest-free payments or longer monthly plans, always showing the total cost (including any interest) before checkout on iOS and Android.

How Is Affirm Similar to Sezzle?

- Both offer pay-in-4 interest-free options

- Both support online and in-store purchases

- Both report payment history to credit bureaus (helping build credit)

How Is Affirm Different from Sezzle?

| Feature | Affirm | Sezzle |

| Max Loan Term | 48 months | 48 months |

| Financing Limit | Up to $20,000 | Up to $15,000 |

| Interest (Long Plans) | 0%–36% APR | 5.99%–34.99% APR |

| Late Fees | None | Up to $16.95 |

| Credit Impact | Soft check (Hard check for some loans) | Soft check (Hard check for Sezzle Up) |

Affirm’s Affirm Card works anywhere Visa is accepted in the US. Sezzle has no equivalent universal card product.

Who Is Affirm Best For?

Affirm suits shoppers financing large purchases (electronics, travel, furniture) who want full cost transparency and no surprise late fees, even if some plans carry interest.

Key Features of Affirm

- Pay in 4: Interest-free, biweekly

- Monthly financing: 3–60 months, 0%–36% APR

- Affirm Card: Visa card accepted everywhere in the US

- No late fees: Missed payments reported to bureaus, not charged

- Credit bureau reporting: To Experian (as of April 2025)

Pricing

- Free plan: Yes

- Interest: 0%–36% APR depending on term and creditworthiness

- Late fee: None

- Free trial: N/A

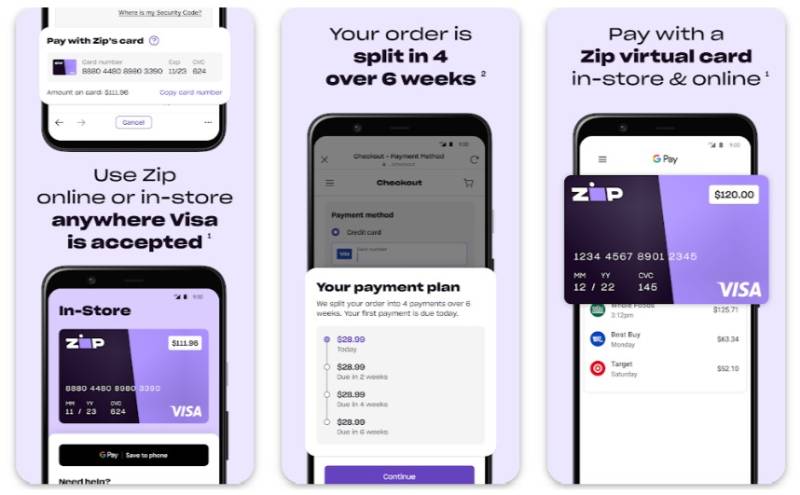

Zip (formerly Quadpay)

Zip is a buy now pay later app that splits purchases into 4 installments over 6 weeks, usable online and in-store anywhere Visa is accepted via a virtual card. It targets everyday shoppers who want wide merchant acceptance.

What Does Zip Do?

Zip generates a one-time virtual Visa card at checkout, letting users split any purchase into 4 installments at virtually any retailer, on iOS and Android.

How Is Zip Similar to Sezzle?

- Both use a pay-in-4 model with biweekly payments

- Both run soft credit checks that do not affect your FICO score

- Both support in-store and online purchases

How Is Zip Different from Sezzle?

Zip’s virtual Visa card works at any store that accepts Visa, not just partner merchants. This makes it significantly more flexible for in-store use. Sezzle is more restricted to its own merchant network.

Zip charges a $1 platform fee per installment ($4 per order total), plus late fees of $5–$10 depending on your state. Sezzle’s fee structure is different, with conditional convenience fees on card payments.

Who Is Zip Best For?

Zip suits shoppers who want to use BNPL at retailers that don’t officially partner with any pay-later service, including brick-and-mortar stores.

Key Features of Zip

- Virtual Visa card: Works anywhere Visa is accepted

- Pay in 4–8 installments: Short-term or longer plans available

- In-store support: Strong, via virtual card

- Long-term plans: Up to 48 months for larger purchases

Pricing

- Free plan: Yes

- Platform fee: $1 per installment ($4 per order)

- Late fee: $5–$10 depending on state

- Free trial: N/A

PayPal Pay in 4

PayPal Pay in 4 is a short-term installment payment option embedded in PayPal’s existing ecosystem. It targets existing PayPal users who want zero-friction BNPL without creating a new account.

What Does PayPal Pay in 4 Do?

PayPal Pay in 4 splits eligible purchases ($30–$1,500) into 4 interest-free biweekly payments, accessible directly within the PayPal app on iOS and Android.

How Is PayPal Pay in 4 Similar to Sezzle?

Both offer interest-free pay-in-4 plans with soft credit checks and biweekly payment schedules. Both are free to use for consumers who pay on time.

How Is PayPal Pay in 4 Different from Sezzle?

PayPal Pay in 4 works wherever PayPal is accepted globally, far outpacing Sezzle’s merchant coverage. The minimum purchase is $30, while Sezzle has no stated floor. PayPal also offers a separate “Pay Monthly” option (up to $10,000, 3–24 months) that Sezzle doesn’t match outside its long-term financing plans.

Who Is PayPal Pay in 4 Best For?

PayPal Pay in 4 suits existing PayPal users who want instant BNPL access without onboarding a new app or account, especially for purchases under $1,500.

Key Features of PayPal Pay in 4

- Pay in 4: Interest-free, purchases from $30 to $1,500

- Pay Monthly: $200–$10,000, 3–24 months, with interest

- No new account needed: Works inside the existing PayPal app

- Buyer protection: Covered by PayPal’s standard dispute resolution

Pricing

- Free plan: Yes

- Pay in 4 interest: 0%

- Pay Monthly interest: Variable (standard PayPal Credit rates)

- Free trial: N/A

Splitit

Splitit is an installment payment platform that uses a shopper’s existing Visa or Mastercard credit card to split purchases without any new application or credit check. It targets credit card holders who want installments without taking on new debt.

What Does Splitit Do?

Splitit places a hold on a user’s existing credit card for the full purchase amount, then charges installments of 2–24 monthly payments while the hold reduces with each payment.

How Is Splitit Similar to Sezzle?

- Both split purchases into manageable installments

- Both offer zero interest on the installment plan itself

- Both support online and in-store purchases

How Is Splitit Different from Sezzle?

Splitit requires no application, no new credit line, and no credit check. It works purely off your existing credit card limit. Sezzle requires a separate account and its own approval process.

Splitit’s white-label model means it can appear as part of a merchant’s own branding. Sezzle always appears as a third-party option at checkout. According to Splitit, this approach leads to 78% higher checkout conversions and 85% of users return for repeat purchases.

Who Is Splitit Best For?

Splitit suits credit card holders with available credit who want installment flexibility without opening a new account, particularly for purchases over $500 where earning card rewards matters.

Key Features of Splitit

- Installment range: 2–24 monthly payments

- No credit check: Approval based on available card credit only

- Card rewards: Users still earn points or cashback on the full purchase

- White-label: Merchants can brand the checkout experience

Pricing

- Free plan: Yes (no fees to consumers)

- Interest: None from Splitit; card’s own APR applies if you carry a balance

- Late fee: None from Splitit directly

- Free trial: N/A

Perpay

Perpay is a payroll-linked BNPL marketplace that deducts installment payments directly from a user’s paycheck. It targets shoppers with limited or no credit history who want to build credit through everyday purchases. If you want to explore more options in this category, check out these Perpay alternatives.

What Does Perpay Do?

Perpay lets users shop its curated marketplace of brand-name products and pay over time through automatic payroll deductions, with no hard credit check required, on iOS and Android.

How Is Perpay Similar to Sezzle?

- Both offer interest-free installments with no hard credit check

- Both report payments to credit bureaus to help users build credit

- Both target shoppers with limited credit access

How Is Perpay Different from Sezzle?

Perpay is tied to income-based underwriting, not credit score. Payments come directly from your paycheck, which eliminates missed payment risk. Sezzle works independently of your employer.

Perpay is marketplace-only. You cannot use it at external retailers. Sezzle works across 41,800+ partner merchants, offering far more shopping flexibility.

Who Is Perpay Best For?

Perpay suits salaried workers with thin credit files who want to buy name-brand electronics or appliances and build credit through automatic, paycheck-linked payments.

Key Features of Perpay

- Payroll deduction: Payments auto-deducted on each pay cycle

- No credit check: Eligibility based on income, not FICO score

- Credit reporting: Payments reported to all 3 major bureaus via Perpay+

- Installments: Up to 8 interest-free payments

Pricing

- Free plan: Yes

- Interest: 0%

- Late fee: None (payroll deduction prevents missed payments)

- Perpay+: Optional credit reporting add-on (requires $200+ in on-time payments over 4 months)

Zebit

Zebit is a no-credit-check BNPL marketplace that gives US consumers up to $2,500 in credit to shop across electronics, home goods, and fashion. It targets shoppers who have been rejected by other BNPL services due to credit issues.

What Does Zebit Do?

Zebit assigns a credit limit based on income verification (not a FICO check) and lets users shop its internal marketplace, paying off purchases interest-free over up to 6 months.

How Is Zebit Similar to Sezzle?

Both use soft credit checks and offer interest-free payment plans. Both are available to US shoppers with limited credit history. Both target budget-conscious consumers looking for deferred payment options on everyday items.

How Is Zebit Different from Sezzle?

- Zebit is marketplace-only; Sezzle works across 41,800+ external merchants

- Zebit gives up to 6 months to repay vs. Sezzle’s standard 6-week pay-in-4

- Zebit does not report payments to credit bureaus; Sezzle’s Up program does

- Products on Zebit may cost more than buying the same item elsewhere

Who Is Zebit Best For?

Zebit suits US consumers with poor or no credit who need electronics or home goods and want 6 months to pay with zero interest and no FICO impact.

Key Features of Zebit

- Credit limit: Up to $2,500 based on income

- Repayment term: Up to 6 months, interest-free

- No FICO check: Income verification only

- Brands available: Samsung, Apple, PlayStation, Macy’s, and 1,500+ others

Pricing

- Free plan: Yes

- Interest: 0% on all purchases

- Late fee: Not publicly disclosed

- Free trial: N/A

Paidy

Paidy is a Japanese BNPL service that lets shoppers in Japan buy online and pay monthly via convenience store or bank transfer, with no credit card required. It targets Japanese consumers who want cashless shopping without a card.

What Does Paidy Do?

Paidy consolidates a user’s monthly purchases into one bill, payable the following month at a convenience store or via direct bank debit, across iOS and Android in Japan.

How Is Paidy Similar to Sezzle?

- Both offer deferred payment with no credit card required

- Both run soft verification checks at signup

- Both allow consumers to split larger purchases into installments

How Is Paidy Different from Sezzle?

Paidy operates exclusively in Japan and supports local payment methods like convenience store cash payments. Sezzle is US and Canada focused. Paidy was acquired by PayPal in 2021 for approximately $2.7 billion, giving it strong institutional backing.

Who Is Paidy Best For?

Paidy suits Japan-based shoppers who want to buy online without a credit card and prefer paying monthly through familiar local channels like convenience stores.

Key Features of Paidy

- Monthly billing: All purchases bundled into one monthly statement

- Payment methods: Convenience store cash, bank transfer

- 3-pay installments: Split any purchase into 3 interest-free payments

- No credit card required: Phone number and email sufficient for signup

Pricing

- Free plan: Yes

- 3-pay fee: 300 yen per installment (waived for bank transfer)

- Interest: 0% on standard plans

- Free trial: N/A

ViaBill

ViaBill is a no-credit-check BNPL service offering interest-free installment payments across the US, Denmark, and Spain. It targets shoppers who want quick approval and guaranteed interest-free splits without a credit inquiry.

What Does ViaBill Do?

ViaBill splits purchases into 4 equal interest-free monthly payments at partner retailers, with instant approval and no credit check, on iOS and Android.

How Is ViaBill Similar to Sezzle?

- Both offer 4-installment interest-free payment plans

- Both provide near-instant approval at checkout

- Both target shoppers who want to avoid credit cards for smaller purchases

How Is ViaBill Different from Sezzle?

ViaBill’s standard plan caps at $300 credit, much lower than Sezzle’s limit. ViaBill+ extends this to $1,500 for a setup fee of $5.99–$29.99 monthly. Sezzle has no equivalent tiered subscription model.

ViaBill is accepted at major retailers like Amazon, Walmart, and Expedia. Sezzle’s network skews toward independent and mid-size retailers.

Who Is ViaBill Best For?

ViaBill suits shoppers making smaller online purchases (under $300) who want guaranteed interest-free splits with no credit check and instant approval at mainstream retailers.

Key Features of ViaBill

- Standard plan: Up to $300, 4 monthly interest-free payments

- ViaBill+: Up to $1,500, 4–24 flexible payments, in-store and online

- No credit check: Instant approval at checkout

- Accepted retailers: Amazon, Walmart, Expedia, Kmart, AliExpress

Pricing

- Free plan: Yes (standard, up to $300)

- ViaBill+: $5.99–$29.99 setup fee per month

- Interest: 0%

- Late fee: $29 on first missed payment

Comparison Table: Apps Like Sezzle at a Glance

| App | Pay-in-4 | Max Limit | Credit Check | Best For |

| Klarna | Yes | No preset cap | Soft | Large merchant network |

| Afterpay | Yes | $2,000–$3,000 | Soft | Fashion and lifestyle |

| Affirm | Yes | $17,500 | Soft/Hard | Large purchases, transparency |

| Zip | Yes | $1,000–$5,000 | Soft | In-store flexibility |

| PayPal Pay in 4 | Yes | $1,500 | Soft | Existing PayPal users |

| Splitit | No (2–24 mo) | Existing card limit | None | Credit card holders |

| Perpay | No | $1,000+ (income-based) | None | Credit builders, salaried workers |

| Zebit | No (6 months) | $2,500 | None (verification) | No-credit shoppers, US only |

| Paidy | No (monthly) | Variable | Soft | Japan-based shoppers |

| ViaBill | Yes | $1,500 | None | Small purchases, instant approval |

What Is Sezzle and How Does It Work?

Sezzle is a buy now pay later app that splits purchases into 4 equal interest-free installments paid over 6 weeks. The first payment is due at checkout; the remaining 3 come automatically every two weeks from your linked debit card, credit card, or bank account.

It runs a soft credit check at signup, which does not affect your FICO score.

Core plan details:

- Pay-in-4: interest-free, 6-week window, one free reschedule per order

- Long-term financing: 3 to 48 months, up to $15,000 in spending power, interest up to 34.99% APR

- Convenience fees apply on card payments after the first installment (avoidable by switching to a bank account)

- Merchant network: ~41,800 active merchants including Target and GameStop

Sezzle Up is an optional credit-building program. Opt in and Sezzle reports your payment history to all three major credit bureaus.

According to a 2025 LendingTree survey, Sezzle holds an 11% usage share among BNPL users in the US, placing it behind PayPal (56%), Klarna (38%), Affirm (38%), and Afterpay (38%).

How Do BNPL Apps Like Sezzle Make Money?

BNPL platforms look free to use. For most short-term pay-in-4 plans, they actually are, as long as you pay on time. The revenue comes from elsewhere.

Merchant discount rate (MDR) is the primary source. Every time a customer pays with a BNPL app, the retailer pays the BNPL provider a percentage of the sale.

| Revenue Source | Who Pays | Typical Range |

| Merchant Discount Rate | Retailer | 2% to 8% per transaction |

| Late Fees | Consumer | $7 to $10 per missed payment |

| Interest (Long-term) | Consumer | 0% to 33.99% APR |

| Subscription Tiers | Consumer | $4.99 to $44.99/month (e.g., Klarna Plus/Max) |

BNPL merchant fees run significantly higher than standard credit card processing (2% to 3%). Merchants accept this because merchants who offer BNPL see average order values increase by around 45%, according to Star Trend Report data.

Klarna is a good example of how this plays out at scale. It processed over $105 billion in purchases in 2024 and posted a net income of $21 million, its first profitable year, driven mainly by merchant fees and a growing advertising business that brought in $180 million that year.

Consumer fees (late charges, interest on longer plans, subscription add-ons) are secondary but growing as the market matures and competition on MDR tightens.

The CFPB classifying BNPL lenders as credit card providers in May 2024 would have required billing statements and formal dispute processes. The Trump administration moved to rescind that rule in March 2025, reducing direct compliance costs for providers.

What Are the Key Differences Between Pay-in-4 Apps and Installment Financing Apps?

Not all flexible payment apps work the same way. The pay-in-4 model and longer installment financing are two different products that suit different purchase sizes and credit situations.

When Does a Pay-in-4 Plan Make Sense?

Pay-in-4 is built for everyday retail. Short repayment window, no interest, and soft credit check only.

Typical use case fit:

- Purchases under $1,000 (fashion, electronics, home goods)

- Shoppers who want zero interest and no long-term commitment

- Users with limited or no credit history who can’t qualify for traditional credit

Nearly 30% of adults with credit scores between 620 and 659 use BNPL, roughly three times the rate of those with scores above 720, according to Digital Silk research.

That pattern shows pay-in-4 pulling in credit-constrained shoppers who need a zero-interest option for smaller purchases without triggering a hard inquiry.

When Does Installment Financing Make More Sense?

Purchase size and repayment flexibility are the deciding factors here.

Affirm’s financing range goes from $50 to $25,000 with terms from 3 to 60 months. Klarna’s monthly plans extend up to 24 months. These are better suited to high-ticket items where spreading cost over many months matters more than avoiding interest entirely.

Credit reporting is also different. Affirm began furnishing all BNPL loan data to Experian and TransUnion in April 2025. Standard pay-in-4 products from Afterpay, Zip, and standard Klarna plans do not report to bureaus.

| Feature | Pay-in-4 (Sezzle, Afterpay, Zip) | Installment Financing (Affirm, Klarna Monthly) |

| Repayment Window | 6 weeks | 3 to 60 months |

| Interest | 0% | 0% to 36% APR |

| Credit Check | Soft only | Soft or hard (larger amounts) |

| Max Limit | $300 to $4,000 typically | Up to $25,000 |

| Bureau Reporting | Usually no | Yes (Affirm); varies by platform |

Does Using BNPL Apps Affect Your Credit Score?

Until recently, the answer was almost always no. That changed in 2025.

FICO launched two new scoring models, FICO Score 10 BNPL and FICO Score 10 T BNPL, in fall 2025. These models incorporate BNPL loan data into credit score calculations for the first time, according to FICO’s official announcement.

The models were developed after a 12-month joint study with Affirm analyzing over 500,000 consumers. FICO found that for consumers with five or more Affirm loans, scores typically increased or stayed stable under the new model during early testing.

Which platforms report, and which don’t:

- Affirm: Reports all BNPL loans to Experian and TransUnion (since April 2025)

- Sezzle Up: Optional opt-in reports to all 3 major bureaus; users with scores below 600 saw an average 20-point increase within 4 months (Ainvest, 2025)

- Perpay+: Reports after $200+ in on-time payments over 4 months

- Klarna: Reports Term Loans only, not pay-in-4 or Pay in 30

- Afterpay, Zip: Do not report standard plans to bureaus

The soft credit check at signup still applies across all major platforms and does not affect your FICO score regardless of which app you use.

Empower research found that 40% of BNPL users cite “no credit impact” as a top benefit. That calculation is changing as FICO’s new models roll out. Missed payments on reporting platforms now carry real credit consequences.

The CFPB previously flagged BNPL as “phantom debt” because most loans were invisible to lenders. Around 63% of BNPL borrowers had multiple loans outstanding simultaneously, according to CFPB analysis, a pattern lenders couldn’t see until now.

How to Choose the Right App Like Sezzle for Your Situation

The right platform depends on your purchase size, credit status, where you shop, and how much fee risk you’re willing to carry.

Empower data shows the average monthly BNPL spend per user hit $243.90 in June 2025, up nearly 21% from the same month in 2024. That growth includes more people using these apps for larger, less predictable purchases, which makes choosing the right plan more consequential.

| Your Situation | Best Fit | Key Reason |

| No credit history | Perpay or Zebit | Income-based approval, no FICO check |

| Rebuilding credit | Sezzle Up or Affirm | Bureau reporting on timely payments |

| Large purchase ($2,000+) | Affirm or Splitit | High limits, long terms, transparent APR |

| In-store flexibility | Zip or Klarna | Virtual Visa card works anywhere |

| Existing PayPal account | PayPal Pay in 4 | No new app, works wherever PayPal is accepted |

| Want to keep card rewards | Split | Uses existing credit card, no new account needed |

For shoppers who explore other zero-interest installment options similar to Zebit, the key trade-off is always merchant coverage vs. repayment flexibility.

Fee sensitivity matters. Affirm charges no late fees (but reports missed payments). Zip charges $1 per installment ($4 per order) regardless of whether you pay on time. Splitit has no consumer fees at all if you have an available credit card balance.

55% of BNPL users choose these services because they can afford things they otherwise couldn’t, according to Digital Silk data. That’s fine for planned purchases with clear repayment capacity, and riskier for impulse buys stacked across multiple providers simultaneously.

Are BNPL Apps Safe to Use?

Safe for most users who pay on time. Genuinely risky for anyone juggling multiple open plans without tracking them.

BNPL delinquency rates remain low compared to other consumer credit. The Financial Technology Association reports delinquency below 2% across its member BNPL lenders, versus 8.8% for credit card balances transitioning to delinquency in Q3 2024 (Richmond Fed).

Platform-level safety by provider:

- Affirm: SEC-listed public company (NASDAQ: AFRM), reports to credit bureaus, no late fees

- Afterpay: Owned by Block, Inc. (NYSE: SQ), Australian FSA oversight

- Klarna: Swedish FSA regulated, operates in 45 countries under EU financial law

- Sezzle: US-based, licensed lender, NMLS registered

All major platforms use bank-level encryption. Payment data is linked to your existing debit card, credit card, or bank account, with no storage of full card numbers within the BNPL app itself.

The real risk isn’t the platforms. It’s loan stacking. The CFPB found that 66% of BNPL users carry multiple BNPL loans simultaneously, and 33% borrow from more than one lender at once. That creates repayment obligations that don’t show up on traditional credit reports (yet) and can compound quickly.

New York signed the Buy-Now-Pay-Later Act into law in May 2025, the first state-level licensing regime for BNPL lenders. It requires disclosure standards, dispute resolution processes, fee limits, and data privacy protections. Other states may follow, especially after the federal CFPB pulled back on enforcement of its own BNPL rule.

Also worth knowing: around 25% of American BNPL users made a late payment in 2024, up from 18% the previous year, according to the Federal Reserve. The combination of rising usage, expanding purchase categories (groceries, food delivery, travel), and reduced regulatory oversight makes staying on top of payment schedules more important than ever.

FAQ on Apps Like Sezzle

What is the best app like Sezzle?

Klarna and Afterpay are the closest alternatives for general online shopping. Affirm is better for large purchases. Perpay suits shoppers with no credit history. The best option depends on your purchase size, merchant preference, and whether you need credit bureau reporting.

Which BNPL apps work with no credit check?

Perpay, Zebit, and ViaBill do not require a traditional credit check. They use income verification or assign limits instantly at checkout. Sezzle, Klarna, Afterpay, and Zip all run soft credit checks that do not affect your FICO score.

Do apps like Sezzle build credit?

Most do not by default. Sezzle Up, Affirm, and Perpay+ report payments to credit bureaus. Affirm reports all loans to Experian and TransUnion as of April 2025. Standard Afterpay, Zip, and Klarna pay-in-4 plans do not report.

What apps let you pay in 4 interest-free installments?

Klarna, Afterpay, Zip, PayPal Pay in 4, and ViaBill all offer a pay-in-4 interest-free model. Each splits the purchase into equal biweekly payments with no interest charged on the short-term plan as long as you pay on time.

Is Afterpay or Klarna better than Sezzle?

Klarna has a larger merchant network (800,000+ retailers globally) and more payment options. Afterpay dominates fashion and lifestyle retail. Sezzle focuses on independent and mid-size US merchants. For sheer coverage, Klarna edges out both for most shoppers.

What BNPL app has the highest spending limit?

Affirm offers the highest limit at up to $25,000 on long-term financing plans. Sezzle goes up to $15,000. Klarna has no preset cap on point-of-sale loans. Afterpay caps short-term plans at $4,000 and monthly plans at $20,000.

Can I use BNPL apps in-store?

Yes. Zip and Klarna generate a one-time virtual Visa card usable anywhere Visa is accepted. Afterpay works in-store via its card at participating retailers. Sezzle supports in-store payments at partner merchants through its virtual card feature.

Are there BNPL apps for bad credit?

Perpay and Zebit are designed for shoppers with poor or no credit. Both use income-based approval instead of FICO scores. Zebit gives up to $2,500 in credit after income verification. Neither reports negative payment behavior to credit bureaus.

What is the difference between Splitit and Sezzle?

Splitit uses your existing credit card balance, so there is no new application or credit check. Sezzle opens a separate account with its own approval process. Splitit also lets you earn card rewards on the full purchase amount, which Sezzle does not.

Will using BNPL apps affect my credit score?

It depends on the platform. FICO launched new scoring models in fall 2025 that incorporate BNPL data for the first time. Missed payments on reporting platforms like Affirm now carry real credit consequences. Soft approval checks at signup never affect your score.

Conclusion

This conclusion is for an article presenting apps like Sezzle, a category that has grown well beyond a single pay-in-4 model.

Whether you need a larger spending limit, no credit check, or a deferred payment plan that actually reports to credit bureaus, there is a solid option in this list.

Affirm works best for high-ticket financing. Splitit suits credit card holders who want installments without new debt. Perpay and Zebit cover shoppers with thin credit files.

The BNPL market is also shifting. FICO’s new scoring models mean your repayment behavior on platforms like Affirm and Sezzle Up now carries real credit consequences.

Pick the platform that matches your purchase size, merchant network, and fee tolerance. Getting that match right matters more than going with the most recognizable name.

- Android App Bundle vs APK - August 1, 2026

- PHP Cheat Sheet - July 31, 2026

- How Computer Vision, built on existing systems, increases inventory accuracy by 20%+ and protects profit margins - July 31, 2026