Most cash advance apps weren’t built for gig workers. They want a W-2, a fixed employer, a predictable paycheck. If you drive for Uber, deliver for DoorDash, or freelance on your own terms, that disqualifies you before you even apply.

That’s exactly the gap Ualett was designed to fill. But it’s not the only option.

Whether Ualett’s factor fee model feels too expensive, your bank isn’t supported, or you just need a smaller same-day cash advance, there are solid alternatives built for the same audience: independent contractors, rideshare drivers, delivery couriers, and self-employed workers who need fast access to earned wages without a credit check.

This guide covers the best apps like Ualett, how each one works, what it costs, and who it actually fits.

Apps Like Ualett

EarnIn

EarnIn is an earned wage access app that lets workers pull from wages they’ve already earned, before payday. It supports both iOS and Android, requires no credit check, and charges no mandatory fees.

What Does EarnIn Do?

EarnIn lets users access up to $150 per day and up to $1,000 per pay period from wages already earned, repaid automatically on the next payday.

How Is EarnIn Similar to Ualett?

Both skip credit checks entirely and use income verification instead. Neither charges interest. Both target workers who need fast access to cash between pay cycles, with same-day or next-day funding options available.

How Is EarnIn Different from Ualett?

- EarnIn requires W-2 employment with a fixed work location or employer email. Ualett is built specifically for gig workers and 1099 contractors.

- Ualett offers up to $2,000. EarnIn caps at $1,000 per pay period.

- EarnIn uses a voluntary tip model. Ualett charges a flat factor fee.

Who Is EarnIn Best For?

EarnIn suits salaried or hourly W-2 employees who need occasional early wage access without paying a subscription fee.

Key Features of EarnIn

- Cash Out: Up to $150/day, $1,000/pay period

- Lightning Speed: Instant transfer for $3.99-$5.99

- Balance Shield: Auto-advance when account balance drops low

- Early Pay: Get your direct deposit up to 2 days early

Pricing

- Free plan: Yes, no mandatory fees

- Paid plans: Optional Lightning Speed fee from $3.99

- Free trial: N/A

Dave

Dave is a personal finance app that provides cash advances up to $500 with no interest or credit check. It supports iOS and Android and targets everyday workers and gig economy participants.

What Does Dave Do?

Dave connects to your bank account and offers cash advances through its ExtraCash feature, repaid automatically on your next payday, plus budgeting tools and a built-in side hustle finder.

How Is Dave Similar to Ualett?

Both skip credit checks and charge no interest. Both serve gig workers with irregular income and offer quick, same-day or next-day funding options.

How Is Dave Different from Ualett?

Dave caps advances at $500. Ualett goes up to $2,000, making it the stronger pick for drivers needing a larger short-term cash advance.

Dave charges a monthly membership fee of $1-$8.99 depending on tier. Ualett uses a factor fee model with no subscription. Dave also includes a job board and budgeting tools that Ualett doesn’t offer.

Who Is Dave Best For?

Dave suits gig workers and hourly employees who want cash advances bundled with budgeting features and side hustle discovery, and who need advances under $500.

Key Features of Dave

- ExtraCash: Up to $500, no interest, no credit check

- Side Hustle Finder: Built-in gig job board

- Spending Insights: Budget tracking and overdraft alerts

- Goals Account: Automated savings tool

Pricing

- Free plan: No

- Paid plans: From $1/month; instant transfer fee $1.99-$25

- Free trial: No

Brigit

Brigit is a financial wellness app that combines cash advances with overdraft prediction, credit monitoring, and identity theft protection. Available on iOS and Android, it serves a broad range of workers including freelancers and gig contractors.

What Does Brigit Do?

Brigit monitors your bank account for low balance patterns and proactively sends cash advances up to $250 before overdrafts hit, with no credit check and no interest charges.

How Is Brigit Similar to Ualett?

- No credit check required

- Serves gig workers and independent contractors

- Offers flexible repayment. Brigit lets users extend their due date up to 3 times.

How Is Brigit Different from Ualett?

Brigit caps at $250. That’s far below Ualett’s $2,000 ceiling. Brigit’s strength is proactive overdraft prevention rather than large advance amounts. It also includes credit building tools, which Ualett doesn’t have. Brigit requires a paid subscription to unlock cash advances.

Who Is Brigit Best For?

Brigit suits workers who frequently face overdraft risk and want proactive financial management alongside small cash advances under $250.

Key Features of Brigit

- Auto Advance: Automatic transfer when balance is predicted to go negative

- Credit Builder: Reports to major credit bureaus (paid plan)

- Identity Theft Protection: Included on premium tier

- Earn Extra: In-app gig and side hustle opportunities

Pricing

- Free plan: Yes, budgeting tools only

- Paid plans: $8.99-$14.99/month for cash advance access

- Free trial: No

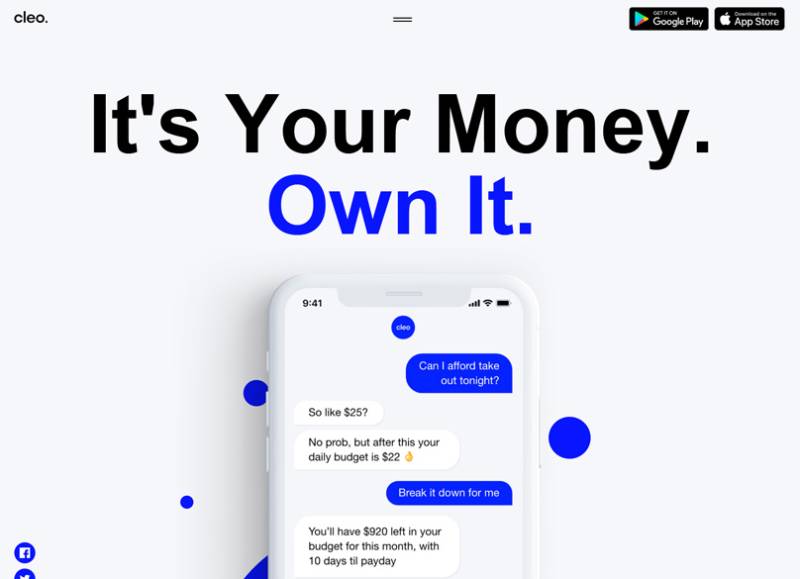

Cleo

Cleo is an AI-powered budgeting app with cash advance functionality, targeting gig workers, freelancers, and self-employed individuals who want financial coaching alongside instant pay access. Available on iOS and Android.

What Does Cleo Do?

Cleo uses an AI chatbot interface to help users track spending, set budgets, and access cash advances up to $250 with no employment verification or credit check required.

How Is Cleo Similar to Ualett?

Both accept gig workers with no credit check and no minimum income requirement. Both offer same-day cash advance access and flexible repayment tied to the user’s next deposit cycle.

How Is Cleo Different from Ualett?

Cleo’s advance cap is $250. Ualett’s is $2,000. Cleo’s differentiator is its AI-driven financial coaching and conversational interface. Ualett is purpose-built for rideshare and delivery drivers. Cleo also charges a monthly subscription for advance access, while Ualett uses a factor fee model.

Who Is Cleo Best For?

Cleo suits freelancers and multi-platform gig workers who want small cash advances paired with AI budgeting coaching, and who don’t need more than $250 at a time.

Key Features of Cleo

- Cleo Advance: Up to $250, no credit check, no employment verification

- AI Chatbot: Conversational financial coaching and spending analysis

- Overdraft Cover: Automatic alerts and overdraft buffer

- Repayment Flexibility: Reschedule repayment date as needed

Pricing

- Free plan: Yes, budgeting tools only

- Paid plans: $5.99/month for cash advance access

- Free trial: No

Branch

Branch is a gig-focused banking and wage access app that integrates directly with platforms like Uber, DoorDash, Lyft, and Instacart. It combines a digital wallet, debit card, and instant pay access in one place. Available on iOS and Android.

What Does Branch Do?

Branch lets gig workers receive earnings from multiple platforms into a single digital wallet, access instant wage advances, and manage income with no monthly subscription fee.

How Is Branch Similar to Ualett?

| Feature | Branch | Ualett |

| Target users | Gig and rideshare workers | Gig and rideshare workers |

| Credit check | No | No |

| Platform integrations | Uber, DoorDash, Lyft, Instacart | Multiple gig platforms |

| Advance funding | Same-day | Within 24 hours |

How Is Branch Different from Ualett?

Branch is primarily an employer-partnered earned wage access platform. Ualett works as a standalone cash advance service without employer participation. Branch advance limits depend on earnings tracked through its platform, while Ualett can offer up to $2,000. Branch charges no subscription fee. Standard transfers are free.

Who Is Branch Best For?

Branch suits multi-platform gig workers who want fee-free earned wage access and a digital wallet to consolidate income from multiple gig apps in one place.

Key Features of Branch

- Multi-Platform Integration: Connects with Uber, DoorDash, Lyft, Instacart

- Instant Pay: Access up to 50% of earned wages same-day

- Fee-Free Banking: No overdraft fees, free Allpoint ATM access

- Debit Card: Branch card with cash-back rewards

Pricing

- Free plan: Yes, no subscription required

- Paid plans: Small fee for instant transfers to external accounts

- Free trial: N/A

Giggle Finance

Giggle Finance is a merchant cash advance platform purpose-built for gig workers, 1099 contractors, and freelancers. It offers advances up to $5,000 with no credit score requirement. Available on iOS and Android.

What Does Giggle Finance Do?

Giggle advances funds based on future gig earnings, not credit history. Repayments are deducted automatically from earnings. Approval and funding can happen within minutes of a successful application.

How Is Giggle Finance Similar to Ualett?

Both are built specifically for gig economy workers and share very similar eligibility models. Neither requires a credit check. Both offer funding based on future receivables, and both repay through automatic deductions linked to gig earnings. They’re probably the closest direct competitors on this list.

How Is Giggle Finance Different from Ualett?

Advance limits differ significantly. Giggle goes up to $5,000. Ualett caps at $2,000. Giggle charges an origination fee of around 7.25%, while Ualett uses a flat factor fee structure. Giggle also requires at least 3 months of active gig work to qualify. Ualett’s customer reviews are stronger overall.

Who Is Giggle Finance Best For?

Giggle Finance suits established gig workers and independent contractors who need larger short-term advances (up to $5,000) and can comfortably repay within a tight schedule.

Key Features of Giggle Finance

- Advance Limit: Up to $5,000

- No Credit Check: Eligibility based on gig earnings history

- Fast Funding: Funds deposited within minutes of approval

- Auto Repayment: Deducted directly from earnings account

Pricing

- Free plan: No

- Paid plans: Origination fee approx. 7.25%; factor fee model

- Free trial: No

Klover

Klover is a zero-fee cash advance app that monetizes through user data sharing rather than subscription or interest charges. It’s available on iOS and Android and works for gig workers and hourly employees.

What Does Klover Do?

Klover provides cash advances up to $200 (extendable to $300+ via a points system) with no credit check, no interest, and no subscription fees. Users earn higher limits by completing surveys, scanning receipts, and watching ads.

How Is Klover Similar to Ualett?

Both offer cash advances with no credit check and no interest. Both accept gig workers and self-employed individuals. Neither charges a monthly subscription fee.

How Is Klover Different from Ualett?

Klover’s advance limit tops out around $300. Ualett offers up to $2,000. Klover funds via pay cycle patterns for traditional workers. Ualett is built exclusively around gig platform earnings data. Klover’s fee-free model trades user data to advertisers, while Ualett charges a transparent factor fee.

Who Is Klover Best For?

Klover suits budget-conscious workers who need small advances under $300 and don’t want to pay a subscription or service fee, and who are comfortable with data sharing.

Key Features of Klover

- Advance Limit: Up to $200 base; up to $300+ with points

- Points System: Earn higher limits through surveys, receipts, and ads

- Budgeting Tools: Spending tracking and financial insights

- No Fees: Zero interest, zero subscription, zero late fees

Pricing

- Free plan: Yes, full access at no cost

- Paid plans: Optional expedited transfer fee

- Free trial: N/A

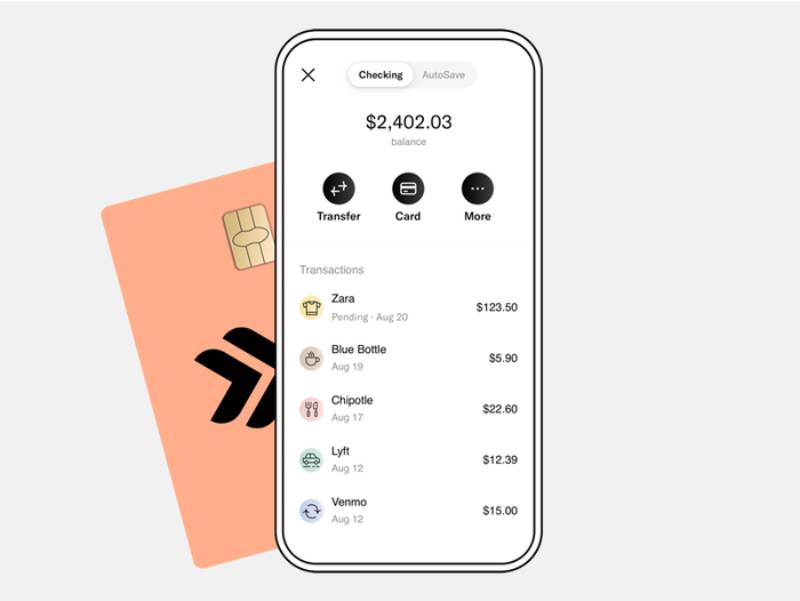

Empower (now Tilt)

Empower, now rebranded as Tilt since August 2025, is a personal finance app offering cash advances up to $400 with automatic overdraft reimbursement and AI-driven spending insights. Available on iOS and Android.

What Does Tilt Do?

Tilt provides cash advances from $10 to $400 with no credit check, automatic overdraft fee reimbursement, and budgeting tools, all behind an $8/month subscription.

How Is Tilt Similar to Ualett?

Both offer no-credit-check advances to gig workers and self-employed individuals. Both analyze bank account activity rather than credit scores. Same-day or instant funding is available on both platforms.

How Is Tilt Different from Ualett?

| Feature | Tilt (Empower) | Ualett |

| Advance limit | Up to $400 | Up to $2,000 |

| Monthly fee | $8/month | No subscription |

| Overdraft reimbursement | Yes | No |

| Target user | General workers | Gig/rideshare workers |

Who Is Tilt Best For?

Tilt suits workers who want a full financial wellness platform with overdraft protection, budgeting tools, and moderate cash advances, and don’t mind a flat monthly fee.

Key Features of Tilt

- Cash Advance: $10-$400, no credit check

- Overdraft Reimbursement: Auto-reimburses overdraft fees from linked banks

- AutoSave: Automated savings based on spending patterns

- Thrive Credit Line: Up to $1,000 as a structured line of credit

Pricing

- Free plan: 14-day trial for new users

- Paid plans: $8/month; instant transfer fee $1-$8

- Free trial: Yes, 14 days

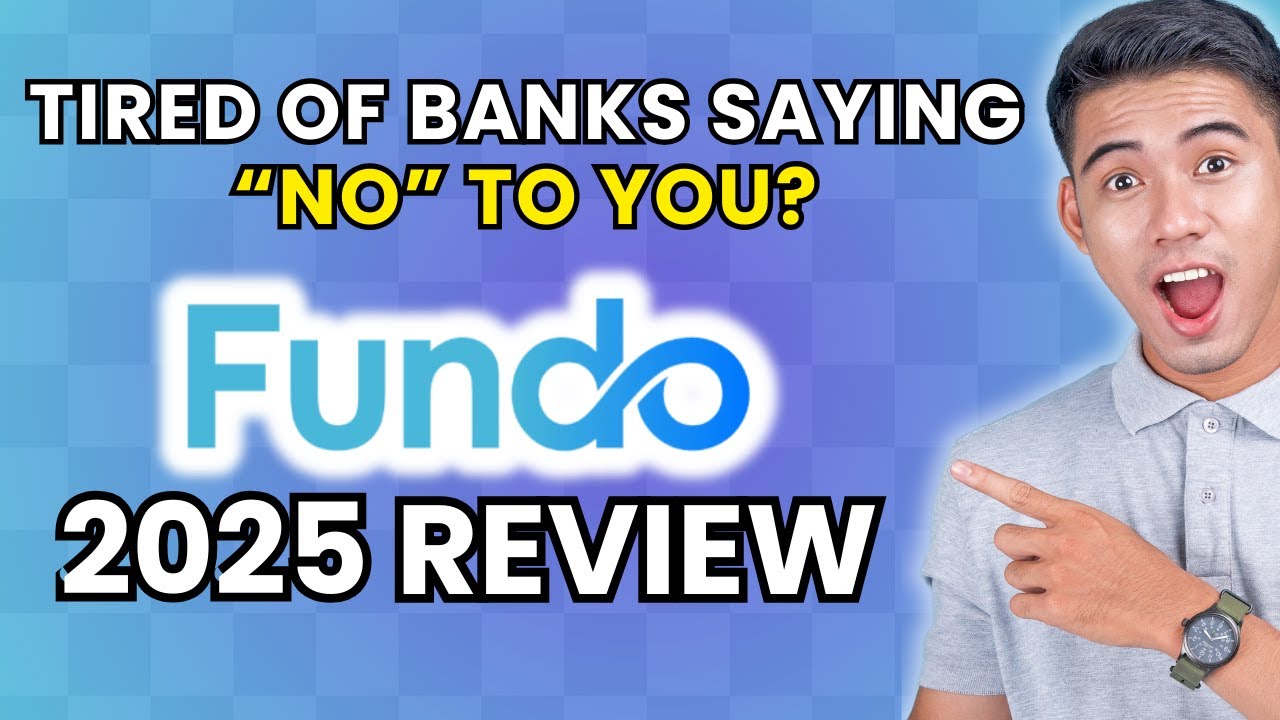

Fundo

Fundo is a merchant cash advance platform designed for gig workers, delivery drivers, freelancers, and micro-businesses. It offers advances up to $10,000 with same-day funding. Available via web and mobile app on iOS and Android.

What Does Fundo Do?

Fundo reviews gig earnings and bank account activity (not credit scores) to fund advances up to $10,000, with repayments deducted from future earnings and discounts available for early payoff.

How Is Fundo Similar to Ualett?

Both are built for gig economy workers and independent contractors. Neither requires a personal guarantee or credit check. Both use future earnings as the repayment source and target Uber, Lyft, and DoorDash drivers specifically.

How Is Fundo Different from Ualett?

Fundo’s advance ceiling is $10,000. That’s the highest on this list. Ualett caps at $2,000. Fundo is technically a revenue-based financing product, not a cash advance. Ualett is structured as a non-recourse cash advance tied to gig platform receivables. Fundo’s customer reviews are more mixed than Ualett’s.

Who Is Fundo Best For?

Fundo suits established gig workers and small business owners who need larger funding amounts (up to $10,000) and can reliably repay from upcoming earnings.

Key Features of Fundo

- Advance Limit: Up to $10,000

- Same-Day Funding: Funds deposited on approval day

- Early Repayment Discount: Pay off early to reduce total cost

- No Personal Guarantee: Gig earnings are the only collateral

Pricing

- Free plan: No

- Paid plans: Factor fee model; exact rates not publicly disclosed

- Free trial: No

Moves

Moves is a gig economy banking platform that partners directly with over a dozen gig companies to offer cash advances, a checking account, and equity participation in the platforms you work for. Available on iOS and Android.

What Does Moves Do?

Moves connects to gig platform accounts, verifies earnings, and provides cash advances based on future receivables without credit checks, while also offering stock-sharing opportunities in partnered gig companies.

How Is Moves Similar to Ualett?

Both connect directly with gig platforms to verify earnings and offer advances against future receivables. Neither uses traditional credit scoring. Both target rideshare and delivery workers as their core audience.

How Is Moves Different from Ualett?

Moves bundles a full banking solution with checking account access and equity in gig platforms, which Ualett doesn’t offer. Ualett focuses purely on fast cash advance access without the broader banking infrastructure. Moves is better for workers wanting a complete financial home base. Ualett is better for those who just need quick access to a larger cash advance.

Who Is Moves Best For?

Moves suits multi-platform gig workers who want a full banking solution, equity in the platforms they work for, and advance access all in one app.

Key Features of Moves

- Platform Integrations: Partners with 12+ gig companies including Uber and DoorDash

- Cash Advance: Based on verified gig earnings, no credit check

- Equity Sharing: Earn stock in gig platforms you work for

- Checking Account: Full digital banking with debit card

Pricing

- Free plan: Yes, basic banking features

- Paid plans: Small fees for instant advance transfers

- Free trial: N/A

What Is Ualett and How Does It Work?

Ualett is not a lender. It’s a receivables purchasing platform operated by Cabicash Solutions Inc., built exclusively for gig workers, independent contractors, rideshare drivers, and delivery couriers.

Instead of issuing a loan, Ualett buys a portion of your future gig earnings at a discount. You receive cash upfront. Ualett collects repayment through weekly deductions from your linked bank account over 8 or 10 weeks.

As of 2025, Ualett has over 395,000 users across 49 U.S. states. That number reflects real demand, because most banks and traditional lenders reject gig workers outright due to irregular income.

How the factor fee works: Ualett charges a flat factor fee of 21% to 24% of the advance amount. On a $500 advance at 22%, you repay $610 total ($61/week over 10 weeks). No interest. No monthly subscription. No hidden fees.

The app connects to your earnings via Plaid, pulling income data from Uber, DoorDash, Lyft, Instacart, Amazon Flex, and other supported platforms. Approval is AI-driven. New users typically receive funds within 24 business hours.

Where Ualett falls short:

- No support for Chime, Cash App, Uber’s bank account, or most neobanks

- Factor fees (21-24%) are high compared to subscription-based apps

- Requires at least 3 months of active gig income to qualify

- Not available in Hawaii or Puerto Rico

For gig workers who need more than $500, Ualett fills a real gap. Most mainstream cash advance alternatives cap out far lower, around $200 to $500.

How Do Apps Like Ualett Compare Across Advance Limits, Fees, and Eligibility?

The cash advance app market was valued at $7.69 billion in 2024 and is projected to reach $25 billion by 2035, growing at an 11.3% CAGR, according to Wise Guy Reports. That growth is driven almost entirely by gig workers and people living paycheck to paycheck.

Not all apps in this space serve the same user. The table below shows how the top alternatives compare on the attributes that matter most to gig workers.

| App | Max Advance | Fee Model | Gig Worker Eligible | Credit Check |

| Ualett | $2,500 | Factor fee (21-24%) | Built for gig workers | No |

| EarnIn | $1,000/period | Optional tip + instant fee | W-2 only | No |

| Dave | $500 | $1-$8.99/month | Yes, flexible | No |

| Brigit | $250 | $8.99-$14.99/month | Yes, partial | No |

| Giggle Finance | $5,000 | Origination fee ~7.25% | Built for gig workers | No |

| Fundo | $10,000 | Factor fee (undisclosed) | Built for gig workers | No |

| Klover | $300 | Free (data sharing model) | Yes, flexible | No |

The clearest split is between apps built for gig workers and apps that simply accept gig workers. EarnIn requires a fixed work location or employer email, which disqualifies most 1099 contractors immediately.

Apps like Dave and Brigit use bank deposit patterns rather than gig platform earnings data. That works for gig workers with consistent deposits, but fails for those with highly irregular weekly income, which is most of them.

Which Apps Like Ualett Work Best for Rideshare and Delivery Drivers?

Ride-sharing accounts for 58% of global gig economy revenue in North America, according to Pebl research. That concentration matters: rideshare and delivery drivers face unique financial timing problems that general cash advance apps weren’t built to solve.

Car repairs don’t wait. Gas bills don’t pause. When a DoorDash driver’s transmission fails on a Tuesday, they can’t wait 3 business days for a standard transfer from a subscription app.

Best for large advances: Giggle Finance and Fundo

Both use the same future-receivables model as Ualett. No credit check. Repayment deducted from gig earnings automatically.

Giggle Finance caps at $5,000 and requires 3+ months of active gig income. Funds arrive within minutes of approval. The tradeoff: an origination fee of around 7.25%, and customer reviews lean negative compared to Ualett’s 97% five-star Trustpilot rating.

Fundo goes up to $10,000. Same-day funding. No personal guarantee required. But fee structures aren’t publicly disclosed, which makes comparison tricky before you apply.

Best for platform integration: Branch

Branch connects directly with Uber, DoorDash, Lyft, and Instacart. Workers receive earnings into a Branch digital wallet and can access a same-day wage advance of up to 50% of earned wages. No monthly fee. Standard transfers are free.

The downside: advance amounts depend entirely on what you’ve earned through Branch-connected platforms. If you work across platforms Branch doesn’t support, your eligible amount drops.

Best for small gaps: Dave and Cleo

| Scenario | Best Pick | Why |

| Need $800+ fast | Ualett or Fundo | Higher ceiling, gig-specific |

| Need $100 before payout | Dave or Cleo | Fast, low cost for small amounts |

| Multi-platform income tracking | Branch | Consolidates gig earnings in one wallet |

| Need $5,000+ for equipment | Fundo | Highest advance ceiling on the list |

Dave caps at $500 and charges instant transfer fees of $1.99 to $25 depending on the size and destination. Cleo caps at $250 with a $5.99/month subscription. Both accept gig workers with bank account income verification, no employer check needed.

What Makes a Cash Advance App Right for Gig Workers With Irregular Income?

There are 76.4 million freelancers in the U.S. in 2025, representing about 36% of the total workforce, according to DemandSage. Yet most fintech lending products were designed for W-2 employees with predictable bi-weekly deposits. That mismatch is why a specific set of criteria matters when gig workers are choosing between apps like Ualett.

Income verification method

This is the most important filter. Two models exist:

- Platform-linked earnings data: Ualett, Branch, Giggle Finance, and Fundo connect directly to gig platforms. They see actual completed gigs, real earnings, and verified receivables. This is the only model that works reliably for workers with no consistent direct deposit schedule.

- Bank deposit pattern analysis: Dave, Brigit, Cleo, and Tilt analyze 60-90 days of bank account deposits. Works for gig workers who deposit consistently, but penalizes those with lumpy or seasonal income cycles.

EarnIn is the strictest. It requires a fixed work location or employer-provided email, which disqualifies all 1099 workers and gig contractors by default.

Repayment structure

Weekly deductions from bank account (Ualett model): predictable, but requires a traditional bank. No neobank support.

Lump-sum on next payday (Dave, EarnIn, Cleo model): works well if you have a reliable payday. For gig workers with variable weekly earnings, this can create cash flow stress at repayment time.

Neobank compatibility

This is an underrated barrier. Many gig workers use Chime, Cash App, or platform-specific accounts (Uber Pro Card, DasherDirect) as their primary banking. Ualett doesn’t support these. Neither does EarnIn.

Dave, Cleo, and Tilt connect through Plaid and work with most bank types including many neobanks. Cash advance apps that work with Chime are a separate category worth checking if that’s your primary account.

Gig workers without traditional bank accounts should also look at cash advance apps that don’t use Plaid for income verification alternatives.

Are Apps Like Ualett Safe and Legitimate for Gig Workers?

Ualett holds a 4.9/5 rating on Trustpilot with over 4,900 verified reviews as of 2025, with 97% rated five stars. That’s an unusually strong signal for a fintech product in a space that attracts a lot of complaints.

Legitimate apps in this category share a recognizable pattern. Here’s what to look for:

- Clear fee disclosure before you sign anything

- Bank-grade encryption and Plaid (or equivalent) for account linking

- No requirement for your Social Security number

- Non-recourse structure (you owe nothing if your gig income drops unexpectedly)

Non-recourse matters more than most people realize. Ualett’s product is technically a receivables purchase, not a loan. If your earnings dry up and you can’t repay, Ualett absorbs that loss. You don’t owe a debt. That’s a meaningfully different risk profile than a payday loan.

The CFPB notes that typical two-week payday loans carry an APR of nearly 400%. Cash advance apps, while not perfect, operate at dramatically lower effective costs, especially apps like EarnIn and Dave that charge no interest at all.

Watch for these red flags in this category:

- Opaque fee structures (Fundo doesn’t disclose rates upfront)

- Guarantee of approval with no income verification

- Apps with no BBB or Trustpilot history

Ualett’s F rating from the BBB (due to two unanswered complaints) looks alarming in isolation, but context matters. The same company scores near-perfectly on every consumer review platform. BBB ratings are based partly on response behavior, not just customer outcomes. Review both sources before deciding.

For workers who want broader fintech app options beyond cash advances, including banking and credit-building tools, several platforms now bundle all three in one product.

What Are the Costs of Using Apps Like Ualett Over Time?

The CFPB analyzed the earned wage access market and found that more than 7 million workers accessed approximately $22 billion in advances in 2022. The average worker accessed $3,000 in funds per year. Repeat usage was high and increasing.

That repeat usage is where the real cost accumulates. One advance is manageable. A habit is expensive.

Subscription vs. factor fee: which costs more?

Subscription model (Dave, Brigit, Tilt):

- Dave: $1-$8.99/month + instant transfer fee $1.99-$25

- Brigit: $8.99-$14.99/month for advance access

- Tilt: $8/month + instant fee $1-$8

Factor/tip model (Ualett, EarnIn, Giggle):

- Ualett: 21-24% flat fee on advance amount, no subscription

- EarnIn: No mandatory fee, optional tip up to $13, instant fee $3.99-$5.99

- Giggle: ~7.25% origination fee on advance amount

For someone borrowing $100 four times a month, a $8.99 Brigit subscription costs less than Ualett’s factor fee on a $400 advance. But Ualett is cheaper per dollar borrowed on a single large advance, especially if you avoid instant transfer fees on subscription apps.

The effective APR reality

A $150 EarnIn advance repaid in two weeks with a $5.99 instant fee works out to a roughly 104% annualized APR, per NerdWallet’s analysis. That sounds alarming until you compare it to payday loans at 400% APR.

Ualett’s 22% factor fee on $500 repaid over 10 weeks works out to an effective cost closer to 50-60% annualized. High by credit card standards. Reasonable by gig worker alternatives.

When a personal loan beats a cash advance

For any need above $500 with a repayment window longer than 8-10 weeks, a personal loan almost always wins on total cost. Apps like Possible Finance offer short-term installment loans that bridge the gap between cash advance apps and traditional personal loans.

Apps like Solo Funds also offer peer-to-peer lending at rates that are often lower than any cash advance product, though funding speed is less predictable.

The bottom line: cash advance apps, including Ualett and its alternatives, are tools for short-term income smoothing. Using them every pay cycle creates a repayment loop that makes the underlying cash flow problem harder to solve, not easier.

FAQ on Apps Like Ualett

What are the best apps like Ualett for gig workers?

The strongest alternatives are EarnIn, Dave, Brigit, Branch, Cleo, Klover, Giggle Finance, Fundo, Tilt, and Moves. Each serves a different need. Branch and Giggle Finance are the closest to Ualett because both are built specifically for independent contractors and gig platform workers.

Which cash advance apps work without a credit check?

Most apps on this list skip the credit check entirely. Ualett, Giggle Finance, Fundo, EarnIn, Dave, Brigit, and Klover all verify eligibility through bank account activity or gig platform earnings data rather than your FICO score.

What is the highest cash advance available for gig workers?

Fundo offers the highest ceiling at $10,000, followed by Giggle Finance at $5,000 and Ualett at $2,500. Most mainstream apps like Dave and Brigit cap at $500 and $250 respectively. Higher limits come with higher fees.

Can Uber and DoorDash drivers use apps like Ualett?

Yes. Ualett, Branch, Giggle Finance, and Fundo are all built around rideshare and delivery driver income. Branch directly integrates with Uber, DoorDash, Lyft, and Instacart. Earned wage access for drivers is the core use case for most of these platforms.

Do any of these apps work with Chime?

Ualett does not support Chime or most neobanks. Dave, Cleo, Brigit, and Klover connect through Plaid and work with Chime. If Chime is your primary account, those are better starting points than Ualett alternatives that require traditional banking.

What is the difference between a factor fee and a subscription fee?

A factor fee is a flat percentage charged on each advance (Ualett charges 21-24%). A subscription fee is a fixed monthly charge regardless of how often you borrow. Dave costs $1-$8.99/month. Neither model charges interest in the traditional sense.

Are apps like Ualett considered payday loans?

No. Ualett is a non-recourse receivables purchase, not a payday loan. Apps like Dave and EarnIn are earned wage access products. The CFPB distinguishes these from payday loans, which typically carry APRs near 400%. Cash advance apps cost significantly less in most scenarios.

How fast do these apps send money?

Ualett funds new users within 24 business hours and returning users nearly instantly via FedNow. EarnIn’s Lightning Speed delivers in minutes for $3.99-$5.99. Dave takes 1-3 days on the free tier. Same-day funding is standard across Giggle Finance and Fundo after approval.

What happens if I cannot repay my cash advance on time?

Ualett allows you to reschedule your payment date at no extra cost. Brigit lets you extend your due date up to three times. Dave does not charge late fees. Non-recourse apps like Ualett absorb the loss if gig income genuinely stops. Most apps won’t send you to collections.

Which app is best for freelancers with irregular income?

Cleo and Dave work well because they focus on bank deposit patterns rather than employer verification. Ualett and Giggle Finance are better for platform-based gig workers with verifiable earnings on Uber, DoorDash, or Instacart. Klover requires no income proof at all for small advances under $200.

Conclusion

This conclusion is for an article presenting apps like Ualett, and the core takeaway is simple: no single app wins for every gig worker.

If you need a large same-day cash advance against future receivables, Giggle Finance and Fundo are the closest matches. For everyday income smoothing under $500, Dave and Cleo handle that without a factor fee.

Branch is the strongest pick for multi-platform workers managing earnings across Uber, DoorDash, and Instacart in one place. Klover works if you want zero-fee earned wage access and don’t mind data sharing.

The right app depends on your advance size, your bank, and how often you actually need it. Use these tools for short-term cash flow gaps. Not as a permanent fix.

- Best 5 AI Penetration Testing Tools for Web and Mobile Applications - August 2, 2026

- Android App Bundle vs APK - August 1, 2026

- PHP Cheat Sheet - July 31, 2026