Perpay works well, until it doesn’t. The payroll-deduction model and closed marketplace lock out gig workers, self-employed buyers, and anyone who wants to shop beyond Perpay’s catalog.

There are plenty of apps like Perpay that offer installment payment plans, no credit check shopping, and even credit-building features, without the W-2 requirement or the single-marketplace restriction.

Some match Perpay’s zero-interest, zero-fee model. Others open up access to hundreds of thousands of retailers. A few, like Affirm and Sezzle, actively report your payments to credit bureaus to help improve your score over time.

This guide covers the 10 best Perpay alternatives across every use case, whether you need flexible payment options, no credit check approval, or a genuine path to building credit while you shop.

Apps Like Perpay

Perpay lets you shop a built-in marketplace and pay through payroll deductions, no credit card needed. It works well for W-2 employees who want to build credit while making purchases. But its closed marketplace and direct-deposit requirement lock out a lot of people.

The BNPL market hit $42.22 billion in 2025 and is projected to reach $147.27 billion by 2031 (ResearchAndMarkets). That growth means more options, better terms, and more flexibility than Perpay alone offers.

Below are the top alternatives, each covering a different gap.

Klarna

Klarna is a buy now, pay later app that lets shoppers split purchases at checkout across multiple payment structures, targeting everyday retail buyers who want flexibility without a credit card.

It works at 800,000+ merchants including Amazon, Best Buy, Walmart, and Target, which is a much wider network than Perpay’s closed marketplace.

What Does Klarna Do?

Klarna lets users split purchases into 4 interest-free payments, defer payment for 30 days, or finance over 6 to 24 months using a soft credit check.

How Is Klarna Similar to Perpay?

- Both offer installment payment options with no interest on short-term plans

- Both use soft credit checks that don’t affect your score

- Both target shoppers who prefer alternatives to traditional credit

How Is Klarna Different from Perpay?

Klarna is not tied to your paycheck. Payments come from any card or bank account, not payroll deductions.

It also works across its entire merchant network, not a single internal marketplace. Monthly financing (6-24 months) can carry up to 35.99% APR depending on creditworthiness.

Who Is Klarna Best For?

Klarna suits shoppers who want wide retailer access and flexible repayment options without linking their employer or payroll.

Key Features of Klarna

- Pay in 4: 4 equal payments every 2 weeks, 0% interest

- Pay in 30 Days: Full payment deferred one month, interest-free

- Monthly financing: 6 to 24 months, 0%-35.99% APR

- Merchant network: 800,000+ retailers worldwide

Pricing

- Free plan: Yes (Pay in 4 and Pay in 30 Days are free)

- Paid plans: Monthly financing rates from 0% to 35.99% APR

- Free trial: No

Afterpay

Afterpay is a BNPL app that splits purchases into 4 interest-free installments over 6 weeks, designed for frequent online and in-store shoppers with no interest charges on standard plans.

It was acquired by Block, Inc. (formerly Square) and has expanded to 15,000+ merchants across fashion, beauty, home, and electronics.

What Does Afterpay Do?

Afterpay divides any eligible purchase into 4 equal payments, with the first due at checkout and the remaining 3 spread over 6 weeks at zero interest.

How Is Afterpay Similar to Perpay?

Both offer no-interest installment plans with soft credit checks only. Neither requires a traditional credit card to get started, and both target buyers who want to avoid revolving credit.

How Is Afterpay Different from Perpay?

Payments are bi-weekly, not payroll-deducted. Afterpay also allows monthly plans from 3 to 24 months for larger purchases. Late fees apply (capped at 25% of order value), while Perpay charges none.

Who Is Afterpay Best For?

Afterpay suits shoppers who want quick, zero-interest installment plans at mainstream retailers without connecting their payroll or employer.

Key Features of Afterpay

- Pay in 4: Zero interest, first payment at checkout

- Monthly plans: 3, 6, 12, or 24 months for larger purchases

- Spending limit: Up to $4,000 short-term, $20,000 long-term

- Grace period: 10-day window before late fees apply

Pricing

- Free plan: Yes (Pay in 4 is free)

- Late fees: Up to 25% of order value per missed payment

- Free trial: No

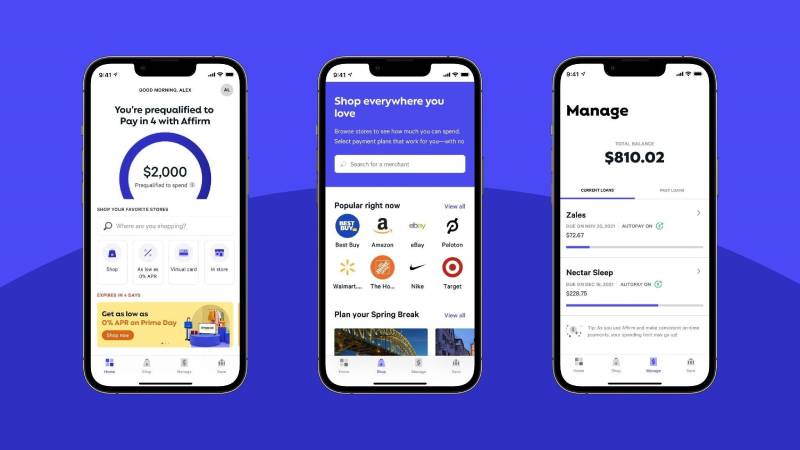

Affirm

Affirm is a consumer financing app that offers transparent, no-hidden-fee installment loans at point of sale, aimed at buyers making mid-to-large purchases who want clear repayment terms upfront.

Affirm is Amazon’s official BNPL partner and is accepted at 300,000+ merchants including Walmart, Target, Expedia, and eBay.

What Does Affirm Do?

Affirm lets users pay in 4 interest-free installments or choose monthly plans from 3 to 60 months, with APR ranging from 0% to 36% depending on credit profile and merchant terms.

How Is Affirm Similar to Perpay?

| Feature | Affirm | Perpay |

| Credit building | Yes, reports to Experian + TransUnion | Yes, via Perpay+ ($3/mo) |

| No credit card needed | Yes | Yes |

| Soft check on pre-qual | Yes | Yes |

How Is Affirm Different from Perpay?

Affirm works at external retailers, not a private marketplace. It also charges 0% late fees on all plans, which Perpay also avoids, but Affirm offers financing up to $17,500 at select merchants.

As of April 2025, Affirm reports all loans including Pay in 4 to Experian and TransUnion, which means on-time payments actively build your credit score.

Who Is Affirm Best For?

Affirm suits buyers who want no-fee, transparent financing for larger purchases and want those payments to report directly to credit bureaus.

Key Features of Affirm

- Pay in 4: Interest-free, no fees

- Monthly plans: 3 to 60 months, 0%-36% APR

- Credit reporting: Experian and TransUnion (as of April 2025)

- Max financing: Up to $17,500 at select merchants

Pricing

- Free plan: Yes (Pay in 4 is free)

- Paid plans: 0%-36% APR on monthly financing

- Late fees: None

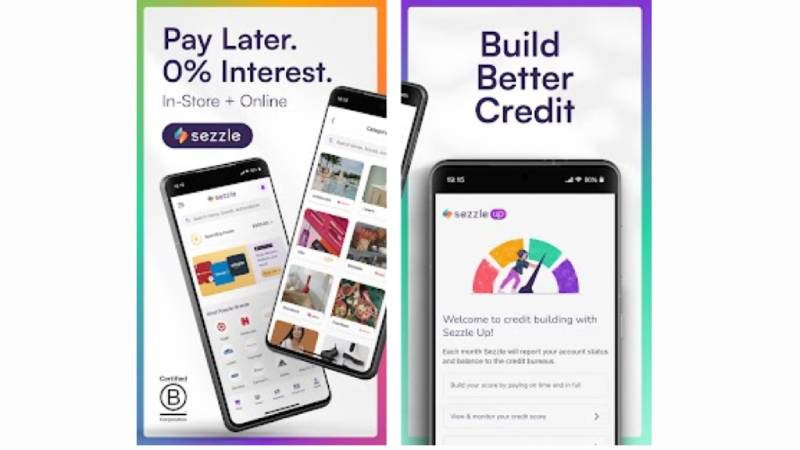

Sezzle

Sezzle is a buy now, pay later app focused on credit-building shoppers who want installment payments with the option to report payment history to all three major credit bureaus.

Sezzle has 41,800 active merchants including Target and GameStop, with a 2-day grace period before late fees kick in.

What Does Sezzle Do?

Sezzle splits purchases into 4 interest-free payments over 6 weeks. Sezzle Up, its optional credit-building tier, reports payments to all 3 bureaus. Long-term plans from 3 to 48 months carry 0%-34.99% APR.

How Is Sezzle Similar to Perpay?

Both prioritize credit building as a core feature, not just a side benefit. Both use soft credit checks. Both target buyers with limited or no credit history who want to shop without a traditional credit card.

How Is Sezzle Different from Perpay?

Sezzle reports to all 3 bureaus through Sezzle Up, while Perpay’s credit reporting is limited to its Perpay+ plan at $3/month. Sezzle also works at third-party retailers, not a closed marketplace.

One free payment reschedule per order is included, which Perpay’s payroll-deduction model doesn’t offer. If you want more options for flexible BNPL shopping, check out these apps similar to Sezzle for more comparisons.

Who Is Sezzle Best For?

Sezzle suits shoppers with limited credit history who want active credit-building features alongside standard BNPL shopping flexibility.

Key Features of Sezzle

- Pay in 4: Interest-free over 6 weeks

- Sezzle Up: Reports to all 3 credit bureaus

- Long-term financing: 3 to 48 months, up to 34.99% APR

- Payment reschedule: One free reschedule per order

Pricing

- Free plan: Yes

- Service fees: $0 to $5.99 per order (varies)

- Free trial: No

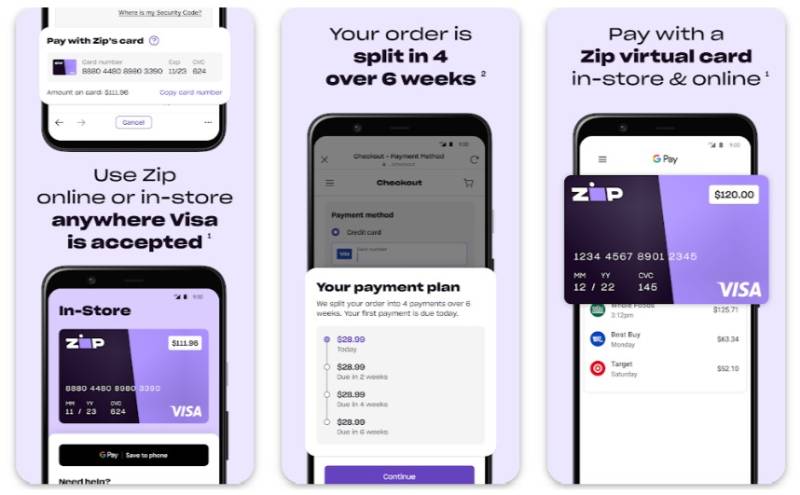

Zip (formerly Quadpay)

Zip is a buy now, pay later app that works anywhere Visa is accepted through a virtual card, targeting shoppers with poor credit who need flexible payment options without a credit check.

Zip does not perform any credit check before approval, which makes it one of the most accessible no credit check shopping solutions available.

What Does Zip Do?

Zip splits purchases into 4 installments over 6 weeks. It generates a virtual Visa card usable at any retailer, online or in-store, with no hard credit pull.

How Is Zip Similar to Perpay?

Both serve buyers with bad or no credit. Both offer installment-based payment plans with no traditional credit card required. Initial credit limits start low and increase over time with good repayment history.

How Is Zip Different from Perpay?

No payroll connection required. Zip works at any Visa-accepting merchant, while Perpay limits shopping to its own marketplace. Zip also allows free payment date adjustments if you need more time.

Who Is Zip Best For?

Zip suits shoppers with a bumpy credit history who want to shop at any retailer without going through employer verification or payroll deductions.

Key Features of Zip

- Virtual Visa card: Works anywhere Visa is accepted

- No credit check: Instant approval without hard pull

- Payment date flexibility: Free adjustment if requested in time

- Late fee: $7 per missed payment (refundable if account in good standing)

Pricing

- Free plan: Yes

- Late fees: $7 per missed payment

- Free trial: No

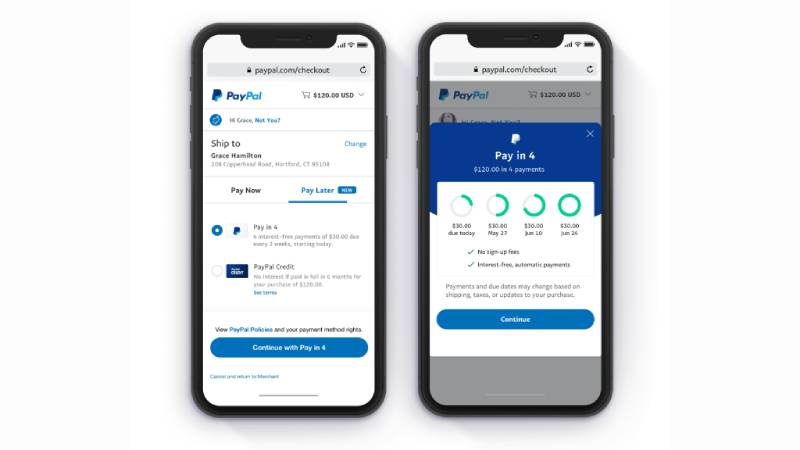

PayPal Pay Later

PayPal Pay Later is a BNPL option built into the PayPal ecosystem, targeting existing PayPal users who want installment plans at millions of merchants without a separate app or account.

It requires no separate signup. If you have a PayPal account, you already have access, which removes most of the friction tied to other buy now pay later apps.

What Does PayPal Pay Later Do?

PayPal Pay Later splits purchases into 4 interest-free payments (Pay in 4) or spreads costs over 6 to 24 months through Pay Monthly at 9.99%-35.99% APR.

How Is PayPal Pay Later Similar to Perpay?

Both offer no-interest short-term installment plans. Both require no credit card at checkout. Pay in 4 uses a soft credit check, similar to Perpay’s approval process.

How Is PayPal Pay Later Different from Perpay?

| Feature | PayPal Pay Later | Perpay |

| Retailer access | Millions (all PayPal merchants) | Perpay marketplace only |

| Payroll deduction | No | Yes (required) |

| Late fees | None on Pay in 4 | None |

| Credit reporting | No | Yes (Perpay+) |

Who Is PayPal Pay Later Best For?

PayPal Pay Later suits existing PayPal users who want simple, no-fee installment plans at any merchant without creating a new account or connecting their employer.

Key Features of PayPal Pay Later

- Pay in 4: Zero interest, no late fees

- Pay Monthly: 6-24 months, 9.99%-35.99% APR

- No separate app: Built into existing PayPal account

- In-store expansion: Virtual card available since October 2025

Pricing

- Free plan: Yes (Pay in 4 is free)

- Paid plans: Pay Monthly from 9.99% APR

- Free trial: No

Splitit

Splitit is a BNPL app that works differently from the rest. It uses your existing credit card to split purchases into interest-free installments, targeting buyers who already have credit cards and want installment flexibility without opening new accounts.

No registration, no credit check, no new account. That’s actually kind of rare in this space.

What Does Splitit Do?

Splitit holds the total purchase amount on your existing credit card as a hold and releases it incrementally as monthly payments are made. Plans run from 3 to 24 months with zero interest.

How Is Splitit Similar to Perpay?

Both let shoppers pay over time in fixed installments with no interest. Both avoid traditional credit applications. Both target buyers who want predictable monthly payment shopping without surprises.

How Is Splitit Different from Perpay?

Splitit requires an existing credit card with available balance. Perpay requires no credit card at all, just a paycheck and direct deposit. Splitit also doesn’t build credit since it uses an existing card, while Perpay+ actively reports to bureaus.

Who Is Splitit Best For?

Splitit suits buyers who already have a credit card with available credit and want to split a larger purchase into monthly payments without interest or a new application.

Key Features of Splitit

- Uses existing card: No new account or credit application

- Plans: 3, 6, 9, 12, or 24 months

- Interest: 0% on all plans

- Late fees: None

Pricing

- Free plan: Yes (no fees to consumers)

- Paid plans: N/A

- Free trial: No

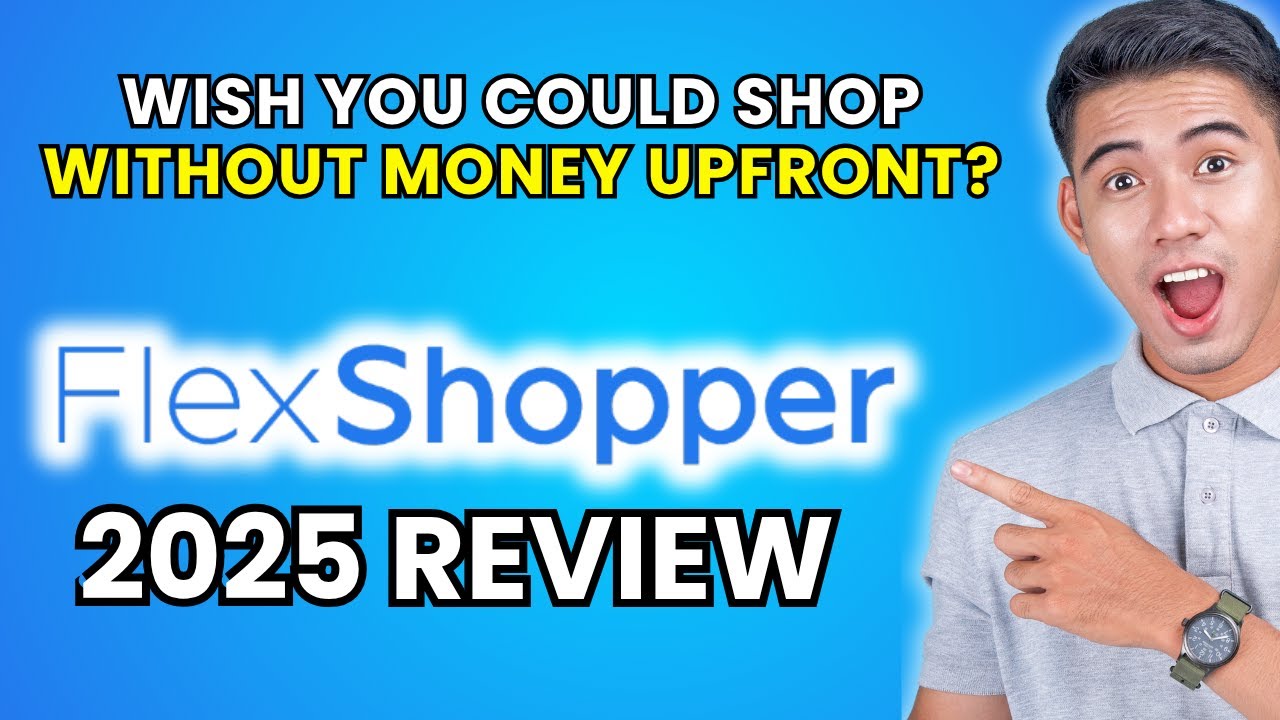

FlexShopper

FlexShopper is a lease-to-own marketplace for electronics, appliances, and furniture, targeting buyers with bad or no credit who need big-ticket items immediately and want flexible weekly payment options.

It operates on a lease model, not a credit model. You rent the item until it’s paid off, then own it. This matters if you’ve been turned down by every other no credit check shopping app.

What Does FlexShopper Do?

FlexShopper approves shoppers for up to $2,500 in lease-to-own spending on 85,000+ products. Payments are weekly over 52 weeks. No credit check required, and approval takes minutes.

How Is FlexShopper Similar to Perpay?

Both work as closed marketplaces with their own product catalogs. Both serve buyers who don’t qualify for traditional credit. Both deduct payments automatically on a scheduled basis.

How Is FlexShopper Different from Perpay?

FlexShopper is a lease-to-own model, not a buy now pay later model. Total cost paid over 52 weeks often significantly exceeds retail price. Perpay’s payroll-deduction model ties payments to your paycheck, while FlexShopper bills weekly regardless of pay cycle.

Who Is FlexShopper Best For?

FlexShopper suits buyers with bad credit who need electronics or appliances immediately and are willing to pay a premium over time for the convenience of instant ownership.

Key Features of FlexShopper

- Lease-to-own: 52-week payment term

- Spending limit: Up to $2,500

- No credit check: Income verification only

- Product catalog: 85,000+ branded products

Pricing

- Free plan: N/A (lease model)

- Weekly payments: Based on item value and lease terms

- Free trial: No

Fingerhut

Fingerhut is a retail credit platform that offers a revolving credit account for shopping its catalog of electronics, clothing, home goods, and more, targeting buyers who want to build credit through regular retail purchases.

Fingerhut has been around since 1948. That longevity reflects something real: it fills a consistent gap for credit-building shoppers who can’t get approved elsewhere.

What Does Fingerhut Do?

Fingerhut issues two credit accounts (Fingerhut Fetti and FreshStart) for purchasing from its catalog. Payments are monthly. The company reports to all 3 major credit bureaus with every on-time payment.

How Is Fingerhut Similar to Perpay?

Both operate as closed retail marketplaces where you shop and pay over time. Both actively report to credit bureaus, making them genuine credit-building shopping platforms. Both target buyers with poor or no credit history.

How Is Fingerhut Different from Perpay?

Fingerhut issues a revolving credit account, not a payroll-deduction plan. It charges interest on balances (unlike Perpay’s interest-free model). A $30 down payment is typically required. Perpay requires direct deposit access to your employer payroll.

Who Is Fingerhut Best For?

Fingerhut suits buyers with poor credit who want a revolving credit account that reports to all 3 bureaus and helps establish a consistent payment history over time.

Key Features of Fingerhut

- Credit reporting: All 3 bureaus with every payment

- Account types: Fetti (revolving) and FreshStart (starter)

- Product range: Electronics, home goods, clothing, toys

- Down payment: $30 required at account opening

Pricing

- Free plan: No (credit account with interest charges)

- APR: Variable, based on account type and creditworthiness

- Free trial: No

Zebit

Zebit is a no-credit-check online marketplace offering interest-free installment plans over 6 months, targeting employed buyers with poor credit who need access to everyday goods without high fees.

Zebit verifies income instead of credit score. Your spending limit (up to $2,500) is based on what you earn, not your FICO. It’s a genuinely different approach compared to most consumer financing apps.

What Does Zebit Do?

Zebit extends a line of credit up to $2,500 based on income verification. Users shop Zebit’s catalog of 175,000+ products and pay in 6-month installments at 0% interest with no fees.

How Is Zebit Similar to Perpay?

Both are income-verified, closed-marketplace platforms with no interest charges. Both serve buyers with bad credit who need a structured spending limit and installment payment shopping. Both use paycheck data to set limits.

How Is Zebit Different from Perpay?

| Feature | Zebit | Perpay |

| Payment Method | Bank account / Debit card | Direct payroll deduction |

| Credit Reporting | No | Yes (Perpay+) |

| Plan Length | Up to 6 months | Flexible (based on pay cycle) |

| Down Payment | ~20%–25% required | None (first payment on payday) |

Who Is Zebit Best For?

Zebit suits employed buyers with bad credit who want interest-free installment shopping without connecting their employer directly or making payroll deductions.

Key Features of Zebit

- No credit check: Income verification only

- Interest rate: 0% on all purchases

- Spending limit: Up to $2,500 based on income

- Product catalog: 175,000+ items

Pricing

- Free plan: Yes (no interest, no fees)

- Down payment: ~20% of purchase price at checkout

- Free trial: No

What Is Perpay and How Does Its Payment Model Work?

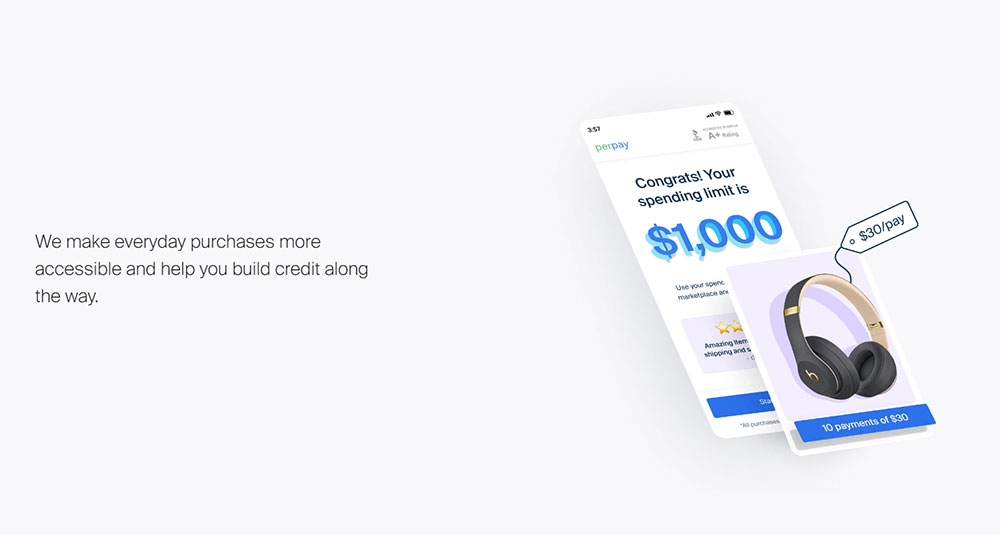

Perpay is a closed-marketplace BNPL platform built specifically for W-2 employees. You shop inside Perpay’s own catalog, and payments are deducted directly from your paycheck via direct deposit.

No credit card. No interest. No late fees. Your spending limit (up to $1,000) is determined by your paycheck, not your credit score.

| Feature | Perpay Standard | Perpay+ |

| Interest | 0% | 0% |

| Late Fees | None | None |

| Credit Reporting | No | Yes, all 3 bureaus |

| Monthly Cost | Free | $3/month |

BNPL purchase volume in the U.S. hit an estimated $70 billion in 2025, growing roughly 20% per year since 2021, according to Richmond Fed research.

What types of purchases does Perpay support?

Perpay’s marketplace covers electronics, home goods, appliances, clothing, and furniture. You can’t use it at external retailers.

That closed ecosystem is Perpay’s biggest limit. If you want a specific item not stocked in their catalog, you’ll need one of its alternatives.

Who qualifies for a Perpay account?

Full-time W-2 employment is required. Gig workers, freelancers, and self-employed individuals don’t qualify.

You also need direct deposit set up with your employer. Perpay deducts payments automatically from each paycheck, which removes the risk of missed payments but limits who can use it.

How Do Apps Like Perpay Compare Across Key Features?

Not all BNPL platforms work the same way. The differences in retailer access, payment method, and credit-building features are significant enough to change which app fits your situation.

PayPal is the most used BNPL provider at 56% of users, followed by Klarna, Affirm, and Afterpay each at 38%, according to a 2025 LendingTree survey.

| App | Retailer Access | Credit Check | Credit Building | Payment Method |

| Perpay | Closed marketplace | Soft pull | Yes (Perpay+) | Payroll deduction |

| Klarna | 1,000,000+ merchants | Soft pull | Partial (Term loans only) | Card, bank account |

| Affirm | 300,000+ merchants | Soft / Hard pull | Yes (all loans) | Card, bank account |

| Sezzle | 41,800+ merchants | Soft pull | Yes (Sezzle Up) | Bank account, debit card |

| Zip | Any Visa merchant | Soft pull | No | Virtual Visa card |

| FlexShopper | Closed marketplace | Soft pull / None | Yes (Reports to bureaus) | Weekly bank draft |

An estimated 91.5 million Americans will use BNPL in 2025, up from 86.5 million in 2024, according to Capital One Shopping research.

Which apps work without W-2 employment?

Klarna, Afterpay, Affirm, Sezzle, Zip, PayPal Pay Later, Splitit, FlexShopper, Fingerhut, and Zebit all work without employer verification.

Key difference: Perpay requires your employer’s payroll system. Every other major alternative on this list uses a debit card, credit card, or bank account instead.

Open-network vs. closed-marketplace apps

Klarna and Affirm lead on retailer flexibility. Klarna covers 800,000+ merchants. Affirm powers checkout at Amazon, Walmart, and Target.

FlexShopper and Fingerhut, like Perpay, operate as closed catalogs. The trade-off is that closed systems often have higher approval rates for buyers with poor credit.

Which Apps Like Perpay Help Build Credit?

Most BNPL apps don’t report payments to credit bureaus. That’s changing fast, but right now only a few platforms actively help you build a credit score through installment payment shopping.

TransUnion research from 2024 found 89% of BNPL users are satisfied with these products, and 75% expect their on-time payments will positively impact their credit. Most are right to expect that, at least with the right platform.

Which BNPL apps report to credit bureaus?

Affirm is the most aggressive on credit reporting. As of April 2025, it reports all loans, including Pay in 4, to Experian and TransUnion. That’s a meaningful shift from its previous policy.

- Affirm: Reports all loans to Experian + TransUnion (April 2025)

- Sezzle Up: Reports to all 3 bureaus via opt-in tier

- Fingerhut: Reports to all 3 bureaus on every monthly payment

- Perpay+: Reports to all 3 bureaus for $3/month

- Klarna: Reports Term Loan data to TransUnion only (since September 2024)

FICO’s simulations show most users see a score change of around +/-10 points when BNPL data is factored in, according to Bank of Hawaii research.

Does using BNPL apps affect your credit score?

For most apps, no, not yet. Pay in 4 plans from Afterpay, Klarna (short-term), Zip, and PayPal Pay in 4 still don’t report to bureaus.

That changes in Fall 2025. FICO launched new scoring models (FICO Score 10 BNPL and FICO Score 10 T BNPL) that incorporate BNPL loan data for the first time. Missed payments on any reporting platform will now count against your score the same way a missed credit card payment does.

For credit-building shoppers, the safest bets remain Affirm and Sezzle Up, both of which have full bureau reporting already in place.

What Apps Like Perpay Work Without a Credit Check?

Perpay uses a soft credit check, which doesn’t affect your score. A few alternatives go further and skip credit checks entirely, approving based on income or debit card access alone.

Nearly 60% of BNPL users have admitted to using these services to finance a purchase they couldn’t otherwise afford, according to Motley Fool Money’s 2025 BNPL Trends Report. No-check options serve exactly this group.

No credit check shopping apps compared

Zip: Zero credit check. Generates a virtual Visa card usable anywhere Visa is accepted. Immediate approval, $7 late fee (refundable in good standing).

Zebit: Income verification only. Up to $2,500 at 0% interest across 175,000+ products. Requires a roughly 20% down payment at checkout. No credit score required.

FlexShopper: No hard pull. Lease-to-own model with up to $2,500 on 85,000+ products. Weekly payments over 52 weeks. Total cost often exceeds retail price significantly.

Soft check vs. no check: what’s the real difference?

| Check Type | Apps | Score Impact | Typical Approval |

| No check | Zip, Zebit, FlexShopper | None | Income / debit card only |

| Soft check | Klarna, Afterpay, Sezzle, Perpay | None | Light credit profile review |

| Hard check | Affirm (monthly plans), Fingerhut | Minor temporary dip | Full credit file review |

The no-check route usually comes with trade-offs: lower spending limits, closed catalogs, or lease-to-own terms instead of outright purchase. Worth knowing before you commit.

What Apps Like Perpay Give Access to More Retailers?

Perpay’s closed marketplace is its defining limitation. If you want to shop at Amazon, Target, or any specific retailer, you need an open-network alternative.

BNPL results in an 85% higher average order value than other payment methods, according to Capital One Shopping research. That’s why retailers push hard to integrate these platforms at checkout.

Open-network BNPL apps with the widest reach

Klarna works at 800,000+ merchants globally including Amazon, Best Buy, Walmart, and Target. Its virtual card also lets you shop at any Visa-accepting store not officially integrated.

- Affirm: 300,000+ merchants, Amazon’s official BNPL partner

- Afterpay: 15,000+ merchants across fashion, beauty, home goods

- PayPal Pay Later: millions of merchants, no separate app needed

- Zip: anywhere Visa is accepted, online and in-store

Splitit is a different case. It uses your existing credit card at any retailer that accepts cards, which means it works almost universally without adding a new account.

Can you use BNPL apps in physical stores?

Yes, most major platforms now support in-store use. PayPal Pay Monthly expanded to physical stores in October 2025 via a 24-hour single-use virtual card. Klarna’s physical card works anywhere Visa is accepted in-store.

Zip and Afterpay both work in-store through virtual card generation in-app. Sezzle issues a virtual card for both online and physical retail use at 41,800+ merchants including Target and GameStop.

How Do Perpay Alternatives Handle Fees and Interest?

Perpay charges zero interest and zero late fees. That’s genuinely hard to beat. But several alternatives match it, and a few actually come close on total cost.

Numerator’s 2025 survey found that managing cash flow (36%) is the top reason consumers use BNPL, with making large purchases affordable (28%) close behind. Fee structure matters a lot to this audience.

Zero-fee options

Three platforms charge no fees of any kind on their standard plans:

- Affirm: No late fees on any plan, 0% APR on Pay in 4

- PayPal Pay in 4: No interest, no late fees

- Splitit: Zero fees to consumers, uses existing credit card

Affirm is the only major BNPL provider that reports all U.S. loans to credit bureaus while also charging zero late fees, according to Affirm’s November 2025 investor disclosure.

Late fee comparison across top alternatives

Afterpay caps late fees at 25% of order value, which is the steepest structure in the group. Klarna and Zip both charge $7 per missed payment, though Zip will refund it if your account is otherwise in good standing.

Sezzle’s grace period is 2 days before fees apply. Afterpay and Klarna give 10 days. For buyers who sometimes run late on paydays, those 8 extra days can make a real difference.

Interest rates on longer-term plans

Monthly financing plans add real cost if you carry a balance. Here’s the APR range across the main platforms:

- Klarna: 0% to 35.99% APR (6 to 24 months)

- Affirm: 0% to 36% APR (3 to 60 months)

- Sezzle: 0% to 34.99% APR (3 to 48 months)

- PayPal Pay Monthly: 9.99% to 35.99% APR

FlexShopper’s lease-to-own model doesn’t advertise an APR, but total payments over 52 weeks often end up significantly higher than the item’s retail price. A laptop priced at $335 can cost $725+ by payoff, per public FlexShopper lease estimates. That’s worth knowing before choosing the lease route over a standard BNPL plan.

For the best alternatives to Affirm specifically, the fee and credit-reporting combination makes it a strong benchmark for cost comparison across consumer financing apps.

FAQ on Apps Like Perpay

What is the best alternative to Perpay?

Affirm is the strongest overall alternative. It works at 300,000+ merchants, charges zero late fees, and reports all loans to Experian and TransUnion. For credit building combined with wide retailer access, nothing else comes as close.

What apps like Perpay work without a credit check?

Zip, Zebit, and FlexShopper require no credit check at all. Zip approves through a virtual Visa card. Zebit uses income verification only. FlexShopper runs a lease-to-own model with instant approval based on income and bank account access.

Can you use apps like Perpay if you’re self-employed?

Yes. Perpay itself requires W-2 employment, but every major alternative, including Klarna, Afterpay, Sezzle, Zip, and Affirm, works for gig workers and self-employed buyers. No employer connection or payroll deduction is needed.

Do apps like Perpay build credit?

Some do. Affirm reports all loans to Experian and TransUnion. Sezzle Up reports to all three bureaus. Fingerhut reports to all three bureaus monthly. Perpay+ does the same for $3 per month. Most Pay in 4 plans still don’t report.

Are there apps like Perpay with no interest?

Yes. Klarna, Afterpay, Affirm, Sezzle, and PayPal Pay in 4 all offer zero-interest installment plans. Zebit also charges 0% interest across its full catalog. Interest only applies on longer monthly financing plans, typically ranging from 0% to 36% APR.

What apps like Perpay let you shop anywhere?

Klarna works at 800,000+ merchants. Affirm covers 300,000+. Zip generates a virtual Visa card usable anywhere Visa is accepted. PayPal Pay Later works across millions of merchants without needing a separate app or browser extension.

What is the difference between Perpay and Afterpay?

Perpay deducts payments from your paycheck and limits shopping to its own marketplace. Afterpay splits purchases at external retailers into 4 bi-weekly payments with no interest. Afterpay works for anyone with a debit card, not just W-2 employees.

Which apps like Perpay are best for bad credit?

Zip requires no credit check and works anywhere Visa is accepted. Zebit uses income verification only. FlexShopper offers lease-to-own approval based on income. Fingerhut issues a revolving credit account for bad credit buyers and reports to all three bureaus.

Are apps like Perpay safe to use?

Yes, the major platforms are regulated fintech companies. Affirm, Klarna, Afterpay, and Sezzle are established providers used by tens of millions of consumers. The real risk is overspending. Nearly 60% of BNPL users have financed purchases they couldn’t otherwise afford, per Motley Fool Money 2025.

What apps like Perpay have the lowest fees?

Affirm, PayPal Pay in 4, and Splitit charge zero late fees and zero interest on standard plans. Perpay also charges nothing. Afterpay has the steepest late fees, capped at 25% of order value. Klarna and Zip charge $7 per missed payment.

Conclusion

This conclusion is for an article presenting apps like Perpay as real, tested alternatives to payroll-deduction shopping, each covering a different gap in the buy now pay later space.

If credit building is the goal, Affirm and Sezzle Up report directly to the bureaus. If retailer access matters more, Klarna and Zip open up the widest networks.

Buyers with bad credit have solid options too. Zebit’s income-verified installment plan and FlexShopper’s lease-to-own model both skip the credit check entirely.

No single consumer financing app wins across every category. The right choice depends on where you shop, how you get paid, and whether you’re actively trying to improve your score.

Pick the platform that matches your situation, not the one with the most name recognition.

- Android App Bundle vs APK - August 1, 2026

- PHP Cheat Sheet - July 31, 2026

- How Computer Vision, built on existing systems, increases inventory accuracy by 20%+ and protects profit margins - July 31, 2026