In the exhilarating sprint from private obscurity to the public trading spotlight, there lies a critical, often misunderstood, stage: the IPO lockup period. It’s the invisible hand that steadies the market, the unsung interval in every initial public offering teeming with anticipation and potential upheaval.

Here lies your compass to navigate this temporal labyrinth where early backers stand at the cusp of reaping rewards and new investors scan the horizon for opportunities.

By unraveling the intricacies of post-IPO selling windows and stock trading limitations, this guide affirms itself as the quintessential map for those seeking clarity in the tumultuous seas of the stock market’s debut dances.

The enigma of shareholder resale limitations shall be decoded, revealing the truth behind share price stabilization strategies and the significance of market performance post-IPO.

Immerse in these chronicles, and emerge with a profound understanding of the regulatory compliance period vibrantly painted across the canvas of public offerings.

This treatise promises not just insights, but an empowered stance in a realm where seconds tick like drumbeats, sounding the march of trading and investment.

What is an IPO lockup period?

The lockup period after an IPO is a predetermined span, typically lasting 90 to 180 days, where initial shareholders and insiders are barred from selling their shares. It’s employed to prevent the market from being flooded with excessive stock, which could negatively impact the share price post-IPO.

A lockup period is a contract that states there is a period after a company goes public when the major shareholders are not allowed to sell their shares. The lockup usually lasts between 90 and 180 days. When this period ends, the trading restrictions get removed.

Any investor or employee wants the lockups to be as short as possible so that they can cash out early. However, underwriting banks would ideally like the IPO lockup period to be longer to prevent insiders the drop the share price. The company itself is usually in the middle. They want to be sure the investors are happy with their returns but also don’t want to show that insiders lack faith in the stock.

The goal of an IPO lockup period is to stop the flooding of the market with too much of a company’s stock supply. Usually, just 20% of a company’s shares are offered for the investing public. If a significant shareholder is trying to unload all their holdings in the first week, they can send the stock down, and this does not help anyone.

There is significant evidence that suggests that at the end of the lockup period, stock prices experience a permanent drop of about 1% to 3%. What is also worth noting before a company goes public is that it often goes through an underwriting process where an underwriter is a bank.

Its goal is to structure and support the IPO to make it successful. One of the most common ways is to do this by agreeing to buy the entire inventory of stock of a company.

Quiet Periods

When talking about IPOs, companies need to have a quiet period that takes place before and after the IPO. For the executives of a company, this is an SEC-mandated period of 40 days in which they are prohibited from offering new information. However, this is not available to the public using the S-a filing.

The window of time that is first requested by the SEC is the pre-issue (the quiet period mentioned above) that extends from the date a company files the registration statement with the SEC. This lasts until the day the account becomes effective.

During this period, the SEC limits public discussion or marketing for the upcoming share offering by the company. The second-quarter period lasts 40 days and comes after the IPO. During this time, the staff and syndicate members are not allowed to comment on anything about any projected earnings or issue research reports.

The IPO lockup period also has a quiet period regarding the research reports that relate to the IPO. Even though there is no deadline set here, sell-side analysts that participated in the IPO go through do not publish anything for 20-30 days after the IPO date underwriting process.

The idea behind this is to stop any conflict of interest that might appear in connection with the stock.

Why should you know the IPO lockup period expiring date?

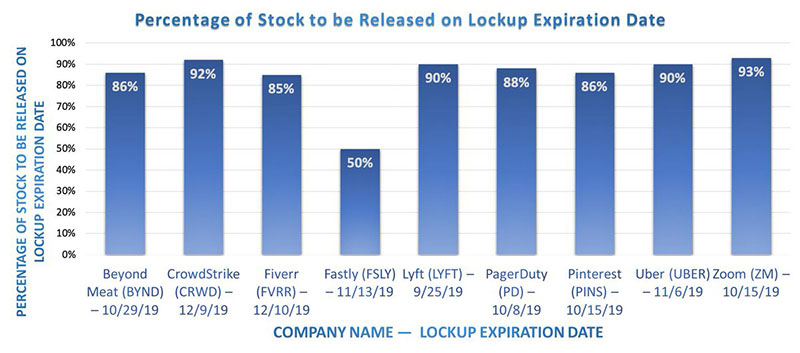

This is an important topic, and if this is the first time you have heard about this concept, here is an explanation. When you want to invest in a company that has made an initial public offering, you need to determine if the company has a lockup and when it expires. This is important because the price of the company’s stock can drop as a result of the locked-up shares that are going to be sold in the market when the lockup is finished.

It is important to consider the fact that every stock is different when using expiring lockups as the motivation to put on a trade. Some might go down a lot, or even collapse as a result of the IPO lockup period ending. Others might flourish and increase their prices. Most of the time, a stock is going to dip a few days in advance before the lockup expiration.

However, they quickly recover and rise even higher than before. The idea is that these dates influence the stock price and you need to pay attention to them.

To discover if a company has an IPO lockup period, you can contact the company’s shareholder relations department. Another option is to get this information online using the SEC’s EDGAR database. Some commercial websites also track when companies have their IPO lockup period set to expire. The SEC does not endorse these websites and makes no representation of the information that is contained on them.

The usefulness of the IPO lockup period

The primary purpose of an IPO lockup period is to stop investors from flooding the market with a high number of shares, which would make the stock price drop. Company insiders have a high percentage of stock shares compared with the general public. Having a higher volume means that when they sell them, this activity can impact the share price very fast after the company goes public.

IPO lockup periods let the new shares to stabilize in the market without any pressure from the investors. This period allows time for the shares to flow naturally between supply and demand. At the start, liquidity can be low but will increase in time.

A company, together with its underwriters, can use the lockup period as a tool to bolster the share price in the IPO. Shares that are held by the bank or investors can be sold during the IPO, but shares owned by company insiders like founders, executives, and more are subject to a lockup period.

Another use of the lockup period is to retain key employees. When stock awards are not redeemable, they keep an employee from moving to the competitor, maintain continuity, or until they completed a critical mission. Lockup periods can be a way for companies to keep up appearances. When the closest to the company keep their shares, they can signal to investors that they have confidence in the power of the company.

FAQs about the IPO lockup period

How Does the Lockup Period Affect Share Prices?

Amid the lockup’s expiry, there can be volatile shifts in share pricing. This is largely due to the anticipation of stocks hitting the market, as investors speculate on potential sell-offs from insiders, which could dilute the stock value or reflect their confidence in the company’s prospects.

Can the IPO Lockup Period Be Waived or Altered?

Indeed, variations to the lockup terms, although rare, might occur. These tweaks typically stem from the underwriters or require consent from the company and its underwriter, especially if changing conditions suggest an adjustment could benefit the shareholder interests and market dynamics.

What Happens When the Lockup Period Ends?

As the lockup curtain lifts, early investors and company insiders are at liberty to sell their stock. This moment can attract a febrile audience as it may result in increased trading activity and, sometimes, heightened share price swings depending on the actions of those restricted shareholders.

Who Is Subject to the IPO Lockup Period?

Company directors, major shareholders, and certain employees typically find themselves beholden to the lockup agreement. This restraint ensures that the market doesn’t get jolted by insiders cashing out too soon after the public offering.

Why Is There a Need for an IPO Lockup Period?

This interval shields the newly minted public entity from volatile trading, typically safeguarding the market stabilization post-IPO. It grants the market time to absorb and appraise the company’s value void of the stress of potential insider selling, fostering a more organized secondary market transition.

What’s the Difference Between an IPO Quiet Period and a Lockup Period?

The quiet period references the time leading up to and shortly after the IPO when promotional chatter is muted. In contrast, the lockup period begins post-IPO, focusing strictly on the sales activities of insiders rather than on communication policies.

Does Every IPO Have a Lockup Period?

Almost universally, a lockup period is a fixed feature of IPOs, pitched as a measure of investor protection. It forms part of a customary agreement brokered by the participating financial advisors and the company pursuing an IPO.

Are There Exceptions to the IPO Lockup Period?

Exceptions, though not commonplace, materialize in instances where the underwriters release certain shareholders from their lockup commitments. These decisions are influenced by factors in the best interests of the company and shareholder equity, weighed with meticulous care and strategic foresight.

What Strategies Should Investors Consider Around the Lockup Expiry Date?

Astute investors keep a tight weather eye on the horizon as the lockup expiry nears. They seek patterns in insider trading intentions, pondering how their actions might ripple through share price stability, and adjust their sails accordingly, setting investment strategies that deftly navigate the shifting tides.

Conclusion

We’ve reached the threshold, the edge where the IPO lockup period lifts its veil. Throughout this article, critical insights have been shared—unwrapping the post-IPO tapestry, piecing together the shareholder restrictions, and deciphering the impacts on the capital market carousel.

- We’ve examined the quiet maneuvers during the lockup agreement terms.

- Explored the ticking clock of lockup expiration dates.

- And anticipated potential market fluctuations.

The wisdom here is not just in knowing the rules but in understanding the choreography of market sentiments that dance to the tune of supply and demand once that lockup period concludes. It’s a nuanced symphony where every instrument—the underwriter, the venture capitalist, the day-trader—plays a role.

As shareholders brace for the freedom to sell, remember this: the lockup period is an architect of stability, guiding a company as it finds its footing on the trading floor. May the insights harbored here be your compass in the complex orchestration of initial public offerings. Embrace the rhythms, for they hold the keys to discerning investment decisions.

If you enjoyed reading this article on the IPO lockup period, you should check out this one about Steve Jobs leadership style.

We also wrote about a few related subjects like risk assessment matrix, business process modelling, business model innovation, business model vs business plan, accelerator vs incubator, startup funding stages, how to value a startup and IPO process.